PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061976

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061976

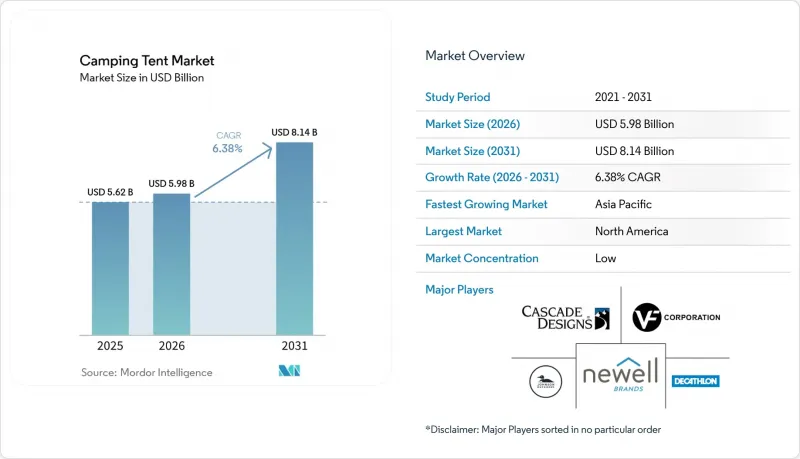

Camping Tent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the camping tent market size was valued at USD 5.62 billion in 2025 and estimated to grow from USD 5.98 billion in 2026 to reach USD 8.14 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dome Tents, Tunnel Tents, Geodesic Tents, Others), Capacity (Below 4 Person, 4 Person and Above), Material (Nylon, Polyester, Composite Fabric Blends, Others), Distribution Channel (Online Retail Stores, Offline Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Camping Tent Market Trends and Insights

Rising popularity of adventure tourism and outdoor leisure activities

Outdoor participation in the United States expanded in 2024, with 181.1 million participants aged six and older, and camping among the top gateway activities, which sustained demand for entry tents and crossover all-season models in 2026, according to the Outdoor Foundation Association. Growth within youth and diverse communities widened the pool of prospective owners, supporting a larger addressable pool for beginner-friendly formats and education-led retailing that clarifies setup, fit, and care. Brands that reduce setup friction or offer clear sizing claims convert casual interest into ownership as users migrate from rentals or shared gear to first purchases that balance weight, space, and weather protection. At the same time, a visible wave of product introductions in 2025 and 2026 reset performance expectations by discarding PFAS treatments and moving toward solution-dyed and recycled textiles that hold up across seasons while easing compliance in North America. This broadening of the user base favors scalable designs, so the camping tent market is seeing continued interest in easy-pitch dome formats for mainstream buyers and expedition-grade geodesic formats for experienced users who want to keep using their gear in harsh conditions without sacrificing long-term durability.

Rising demand for lightweight and easy-to-install tent designs

Ultralight backpacking tents continued to gain momentum during 2025-2026 as manufacturers prioritized sub-1 kg shelters without compromising durability or weather protection. Innovations such NEMO's Dragonfly OSMO, updated for 2025-2026, leverages proprietary 100% recycled composite yarns delivering 4x longer water repellency, 3x less stretch when wet, and 20% greater strength versus similar fabrics, meeting flame-retardancy standards without added chemicals highlight the use of recycled high-performance fabrics, enhanced waterproofing, reduced fabric stretch, and chemical-free flame-retardant compliance, while also improving condensation control and overall strength. At the same time, inflatable airframe tents from brands including Heimplanet, Vango, and Zempire have simplified setup processes, with some models pitching in under five minutes, increasing their appeal among first-time and family campers seeking convenience. Regulatory changes, including Canada's adoption of the CAN/CGSB-182.1-2020 standard in November 2024, are further supporting innovation by reducing reliance on flame-retardant chemicals and lowering material costs for compliant manufacturers.

Counterfeit and low-quality products impacting brand reputation

Counterfeit camping tents sold through e-commerce platforms are increasingly affecting brand reputation and product safety. Tentsile reported an increase in complaints about fake products made with low-quality fabrics, substandard carabiners, and misleading sizing claims, while ToyouTent issued an authenticity alert in February 2026 after fraudulent websites copied internal production visuals to mislead buyers. Product quality concerns are also growing: in November 2024, China's Liaoning Provincial Market Supervision Administration tested 15 batches of outdoor tents and found none compliant, with failures in tear strength, UV protection, waterproofing, and flame-retardant standards. Similarly, the UK Office for Product Safety and Standards detained a two-person tent in 2021 after its polyester fabric failed flammability requirements under the General Product Safety Regulations 2005. These issues are increasing pressure on legitimate manufacturers that invest in ISO 5912 testing and certifications such as Bluesign and OEKO-TEX. Naturehike responded by adopting a "trademark first" strategy after surpassing RMB 1.5 billion in sales, registering intellectual property ahead of market entry in Southeast Asia, and segmenting supply chains to reduce component leakage. Regulatory measures are also tightening, with the EU's 2024 General Product Safety Regulation (GPSR) requiring manufacturers to maintain technical documentation and product traceability, raising compliance standards across the industry.

Other drivers and restraints analyzed in the detailed report include:

- Increasing disposable income supporting recreational travel spending

- Increasing influence of social media and outdoor lifestyle influencers

- Stringent regulations on fire-retardant chemicals increasing compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dome tents captured 36.43% of the camping tent market share in 2025, supported by balanced interior space, familiar setup, and a wide range of price points for casual buyers and weekend users. Growth in geodesic tents is forecast at 8.21% CAGR through 2031, reflecting greater interest in expedition-grade stability that has moved into lighter formats and more accessible price tiers for advanced consumers. New models emphasize structural strength without heavy materials, encouraging users to upgrade as they seek better wind performance and snow-load handling for shoulder seasons and higher elevations. Recycled and solution-dyed fabrics now appear in technical lines alongside established designs, and that pairing signals to buyers that environmental and safety standards can coexist with field durability. Brands that present clear hydrostatic head ratings and pole specifications help new owners match tents to climate and terrain, which supports satisfaction and lowers returns.

The projected rise of geodesic designs is reshaping how the camping tent market communicates value to experienced users who spend more nights outdoors and want confidence when forecasts turn. Retailers and brand sites that compare dome and geodesic architectures educate users on when to trade weight for strength and when marginal ounces are worth additional stability in exposed sites. Multi-vestibule and larger-volume floor plans continue to appear in the upper end of this category as buyers ask for both storm-worthiness and habitability that feels comfortable during longer trips. Terra Nova's geodesic entries illustrate how established technical brands are reconciling weight, recycled content, and waterproof ratings in a single build that appeals to advanced hikers and mountaineers. Across the category, easy-to-follow pitch steps, color cues, and simplified guy-out systems are now standard expectations, aligning technical adoption with usability that limits setup errors for new owners.

Below 4-Person tents held the largest share at 65.58% in 2025, mirroring the needs of solo backpackers, couples, and small groups who value weight savings and compact packed size. Families and multi-generational groups are influencing the top end of the capacity range, with demand for 4-person and larger tents that offer greater live-in comfort over several consecutive nights. The expected 7.36% CAGR for larger capacities reflects how repeat participation leads buyers toward room dividers, taller peak heights, and vestibules that ease daily living at crowded campgrounds, and those features now arrive in packages that remain manageable to transport. Retailers that stage full-size family models allow shoppers to try standing height, cots, and storage arrangements, helping align purchases with planned use and reducing first-trip surprises. This matching of format to need supports lasting satisfaction and fuels repeat purchases when the same household later adds a dedicated backpacking shelter for adult-only trips.

Family buyers also respond to clear messaging around fabric safety, waterproof claims, and ventilation, and they expect to see those assurances across online product pages and in-store displays. Transparent specs narrow the field and make brand comparisons easier as parents seek predictable comfort for longer weekends or holiday weeks on the road. The camping tent market reflects this by presenting capacity, floor plans, and weather ratings in consistent templates so that larger models are easier to grasp when buyers weigh setup time and campsite space. Easy-pitch features and guidance around ground cloths and guyline placement serve as lightweight education that reduces setup stress at arrival and improves the first-night experience. As a result, the larger-capacity segment benefits from clear sizing guidance and repeatable setup, and that clarity underpins its faster growth profile through the forecast.

Geography Analysis

North America accounted for 34.46% of the camping tent market in 2025, supported by a large and diverse participant base that continued to expand in 2024 and stabilized above pre-pandemic levels in 2026. Product adoption reflects both frequent local trips and seasonal destination travel, which pushes retailers to stock a range of capacities and weather ratings that match regional climates and varied terrain. Updated flammability standards and clearer labeling practices are streamlining product introductions in the United States and Canada, and this consistency helps omnichannel retailers maintain unified staff training and consistent education for shoppers. Large-format retailers with vertical integration use displays and education to drive confident first purchases, serving the influx of new participants who prioritize simplicity and value. Technical brands continue to thrive by offering PFAS-free fabric performance and reliable weatherproofing, which resonate with buyers who camp year-round in Northern states and Western high country.

Asia-Pacific is projected to be the fastest-growing region at 7.73% CAGR through 2031, supported by rising participation in urban and peri-urban markets and quality-focused product introductions that balance price, weight, and durability. As retailers and brands expand digital guides and setup content in local languages, barriers to entry fall for first-time owners who want straightforward pitch steps and clear fabric claims. The camping tent market sees strong crossover interest in sub-4 person ultralight shelters for hikers along with 4 to 6 person family configurations for drive-to campgrounds, and both ends of the range benefit from advances in composite fabrics and solution-dyed construction. Manufacturers with consistent labeling and regional compliance documentation can expand faster because their models meet expectations and reduce surprises at delivery. Education and clarity around waterproof ratings, pole materials, and ventilation choices give buyers enough confidence to adopt tents suited to the region's monsoon and summer heat patterns.

Europe maintains steady growth with a mature base of frequent users who value longevity, easy care, and credible environmental improvements in materials. Technical brands in the region continue to publish detailed handbooks and yearbooks that educate buyers on fabric selection, construction, and field care, and this tradition supports informed upgrades to newer tent generations. The EU's evolving product safety and chemical frameworks continue to shape material choices for camping tents, and brands that meet strict requirements while avoiding legacy chemicals can strengthen their quality signal to retail partners and consumers. In this context, composite blends and solution-dyed options help deliver the UV stability, tear strength, and waterproofing that European buyers demand without complex finishing steps. The camping tent market remains diversified across geographies within Europe, with coastal and alpine use cases both sustaining interest in formats that can handle wind, rain, and cooler shoulder seasons.

- Newell Brands (Coleman)

- VF Corporation (The North Face)

- Decathlon S.A. (Quechua & Forclaz)

- Cascade Designs (MSR)

- Big Agnes Inc.

- Hilleberg AB

- NEMO Equipment, Inc.

- Johnson Outdoors Inc. (Eureka)

- Exxel Outdoors LLC (Kelty)

- Sea to Summit

- Black Diamond Equipment Ltd.

- Snow Peak Inc.

- Sierra Designs (Exxel Outdoors)

- Vango (AMG Group)

- Oase Outdoors (Robens, Outwell)

- VAUDE

- Hyperlite Mountain Gear Inc.

- Naturehike Outdoor Products

- NEMO Equipment Inc

- Mountain Hardwear (Columbia Sportswear)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Popularity of Adventure Tourism and Outdoor Leisure Activities

- 4.2.2 Rising Demand for Lightweight and Easy-to-Install Tent Designs

- 4.2.3 Increasing Disposable Income Supporting Recreational Travel Spending

- 4.2.4 Increasing Influence of Social Media and Outdoor Lifestyle Influencers

- 4.2.5 Technological Advancements in Weatherproof and All-Season Tent Fabrics

- 4.2.6 Expansion of E-commerce Platforms Boosting Outdoor Gear Accessibility

- 4.3 Market Restraints

- 4.3.1 Seasonal Nature of Camping Limiting Year-Round Product Demand

- 4.3.2 Counterfeit and Low-Quality Products Impacting Brand Reputation

- 4.3.3 Volatility in Raw Material Prices Affecting Tent Manufacturing Costs

- 4.3.4 Stringent Regulations on Fire-Retardant Chemicals Increasing Compliance Costs

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Dome Tents

- 5.1.2 Tunnel Tents

- 5.1.3 Geodesic Tents

- 5.1.4 Others

- 5.2 By Capacity

- 5.2.1 Below 4 Person

- 5.2.2 4-Person and Above

- 5.3 By Material

- 5.3.1 Nylon

- 5.3.2 Polyester

- 5.3.3 Composite Fabric blends

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Online Retail stores

- 5.4.2 Offline Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Indonesia

- 5.5.3.7 Thailand

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Newell Brands (Coleman)

- 6.4.2 VF Corporation (The North Face)

- 6.4.3 Decathlon S.A. (Quechua & Forclaz)

- 6.4.4 Cascade Designs (MSR)

- 6.4.5 Big Agnes Inc.

- 6.4.6 Hilleberg AB

- 6.4.7 NEMO Equipment, Inc.

- 6.4.8 Johnson Outdoors Inc. (Eureka)

- 6.4.9 Exxel Outdoors LLC (Kelty)

- 6.4.10 Sea to Summit

- 6.4.11 Black Diamond Equipment Ltd.

- 6.4.12 Snow Peak Inc.

- 6.4.13 Sierra Designs (Exxel Outdoors)

- 6.4.14 Vango (AMG Group)

- 6.4.15 Oase Outdoors (Robens, Outwell)

- 6.4.16 VAUDE

- 6.4.17 Hyperlite Mountain Gear Inc.

- 6.4.18 Naturehike Outdoor Products

- 6.4.19 NEMO Equipment Inc

- 6.4.20 Mountain Hardwear (Columbia Sportswear)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS