PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061980

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061980

Icing Sugar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

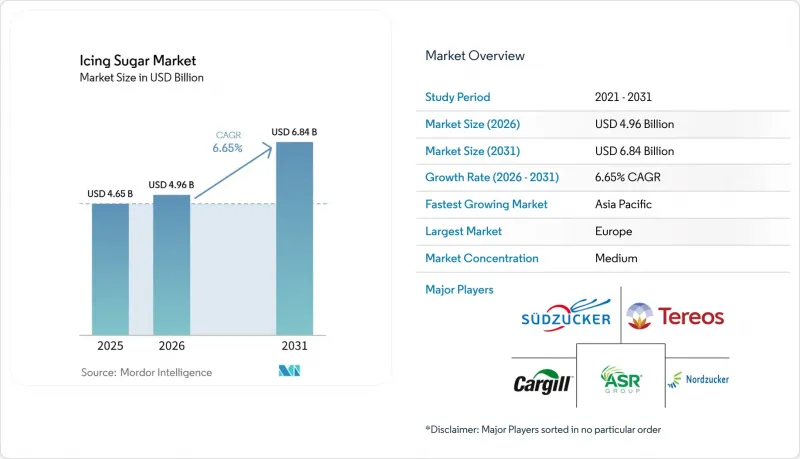

According to Mordor Intelligence, the global icing sugar market is witnessing steady growth, increasing from USD 4.65 billion in 2025 to USD 4.96 billion in 2026, and is projected to reach USD 6.84 billion by 2031, with a CAGR of 6.65% during the forecast period of 2026-2031.

This report is Segmented by Category (Conventional and Organic), Product Type (6X Granulation, 10X Granulation, and 12X/Ultra-fine), Application (Bakery, Confectionery, Beverages, and More), Distribution Channel (B2B/Industrial, Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Both Value (USD) and Volume (Tons).

Global Icing Sugar Market Trends and Insights

Rising consumption of bakery and confectionery products

The increasing consumption of bakery and confectionery products is a significant driver of the global icing sugar market, as it boosts the demand for essential ingredients in large-scale food production. The ongoing growth of industrial bakery and confectionery manufacturing has resulted in greater procurement of standardized inputs like icing sugar, ensuring consistent processing and formulation efficiency. As manufacturers expand production to cater to changing consumer preferences for indulgent and premium sweet products, the demand for reliable, high-quality sugar ingredients has grown. Furthermore, the rise of organized food production systems and automated processing lines has strengthened the demand for icing sugar due to its uniform particle size and ease of integration into production workflows. This consistent growth in bakery and confectionery production across both developed and emerging markets remains a key factor driving the icing sugar market.

Growth of cafe culture and foodservice outlets

The growth of cafe culture and foodservice outlets, driven by the rapid expansion of organized dining and beverage service formats, is increasing the demand for standardized ingredient inputs in professional kitchens. The rise of cafes, quick-service restaurants, and mobile foodservice operators has created a need for consistent, high-quality ingredients to support efficient, high-volume preparation processes. This trend is particularly prominent in Europe, where the foodservice sector is well-developed and continues to grow. According to Eurostat, in 2024, France led Europe in the number of enterprises in restaurants and mobile food service activities, with 178,780 establishments, followed by Italy with 158,820 and Germany with 142,450 . This extensive and expanding network of foodservice outlets is driving large-scale procurement of essential ingredients, such as icing sugar, as operators focus on efficiency, consistency, and standardized preparation across their locations.

Growing health concerns related to sugar consumption

Health concerns related to sugar consumption are a significant restraint on the global icing sugar market. Growing awareness of diet-related health issues, such as obesity and type 2 diabetes, is influencing ingredient choices within the food industry. Consumers and manufacturers are increasingly limiting the use of high-sugar ingredients, driving reformulation strategies aimed at reducing sugar content or replacing traditional sugars with alternative sweeteners. Furthermore, public health campaigns, nutritional labeling requirements, and industry-wide sugar reduction initiatives are pressuring manufacturers to adjust formulations, directly affecting the demand for icing sugar. Consequently, the emphasis on health-conscious consumption patterns continues to limit the growth potential of the icing sugar market.

Other drivers and restraints analyzed in the detailed report include:

- Development of organic, low-calorie, and flavored icing sugars

- Growth in celebration culture

- Regulatory pressure on sugar reduction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The conventional icing sugar segment accounted for 73.46% of the global market share in 2025, primarily due to its strong supply-side advantages, standardized production processes, and widespread industry acceptance. This segment benefits from a well-established manufacturing infrastructure, where refined sugar is processed into fine powdered form using efficient, large-scale milling and anti-caking technologies. These processes ensure consistent quality and uniform particle size. Its dominance is further supported by robust global supply chains, which facilitate easy availability, reliable distribution, and uninterrupted procurement for both bulk and retail buyers. Additionally, conventional icing sugar complies with existing regulatory frameworks and does not require specialized certifications, unlike organic or specialty variants. This simplifies production, labeling, and market entry for manufacturers.

The organic icing sugar segment is emerging as a fast-growing category, with a projected CAGR of 8.11% through 2031. This growth is driven by increasing consumer demand for clean-label, sustainably sourced, and minimally processed ingredients. The segment's expansion is supported by the growing global organic ecosystem, where production capacity and raw material availability are steadily improving. For example, according to Organics International, the number of organic producers worldwide reached 4.8 million in 2024, reflecting significant growth in certified agricultural practices . This increase in organic farming enhances the supply of organically cultivated sugarcane, the primary input for organic icing sugar, thereby strengthening the segment's production base.

The 10X granulation segment, accounting for 48.49% of the global icing sugar market share in 2025, is a key driver of the market due to its balance of fineness, functionality, and processing efficiency. This segment benefits from a standardized particle size distribution, ensuring consistent performance in industrial-scale operations without requiring additional refinement or adjustments. The 10X grade is widely favored by manufacturers for its superior flowability and controlled dusting characteristics, which facilitate smoother handling in automated production systems. Its uniformity also minimizes variability during mixing and blending processes, enhancing batch consistency and reducing production losses.

The 12X and ultra-fine granulation segments are experiencing steady growth, with a projected CAGR of 6.87% through 2031. This growth is driven by their superior refinement, precision processing, and alignment with advanced manufacturing requirements. These finer grades are produced using advanced milling and sieving technologies, resulting in extremely small and uniform particle sizes that improve consistency in formulation processes. The demand for these grades is supported by the increasing need for high-performance ingredients that enable better dispersion, faster dissolution, and smoother integration within complex production systems.

Geography Analysis

Europe is projected to hold 38.09% of the global icing sugar market share in 2025, maintaining its position as the leading regional contributor. This dominance is supported by a well-established sugar refining infrastructure, advanced processing technologies, and the strong presence of organized manufacturers. However, the region faces structural challenges that are moderating its growth. Persistently low sugar prices are compressing producer margins, while elevated sugar beet cultivation costs are creating input-side pressures for refiners. Additionally, evolving regulatory frameworks within the European Union, particularly concerning sugar production quotas, sustainability standards, and labeling requirements, are introducing uncertainty for market participants. These factors collectively constrain growth despite the region's mature supply chain and high level of industry standardization.

Asia-Pacific is the fastest-growing region in the global icing sugar market, with a projected CAGR of 8.04% through 2031. This growth is driven by rapid structural transformation across food systems and supply chains. Factors such as increasing urbanization, rising income levels, and the accelerated development of modern retail and organized foodservice networks are enhancing distribution efficiency and product accessibility. The region's strong reliance on sugar imports further supports the availability of refined sugar inputs necessary for icing sugar production. Countries like China and Indonesia rank among the world's largest sugar importers. For example, according to the United States Department of Agriculture (USDA), China was projected to import 5.3 million metric tons of centrifugal sugar in the marketing year 2025/26, underscoring the scale of raw material inflows that facilitate downstream processing and market expansion in the region .

North America, South America, and the Middle East and Africa collectively account for the remaining share of the global icing sugar market, exhibiting diverse and region-specific growth trends. In North America, a highly industrialized and efficient supply chain supports stable demand, although regulatory scrutiny regarding sugar consumption continues to influence market dynamics. South America benefits from robust sugar production capabilities, particularly in key exporting nations, which ensures raw material availability and supports regional processing activities. In the Middle East and Africa, a growing reliance on imports and the ongoing development of food processing infrastructure are gradually strengthening the region's position in the market.

- Sudzucker AG

- Tereos S.A.

- Cargill, Incorporated

- American Sugar Refining, Inc. (Domino Foods)

- Tate & Lyle PLC

- Nordzucker AG

- Associated British Foods plc (British Sugar)

- Wilmar International Ltd.

- Rogers Sugar Inc.

- Cosan S.A.

- Imperial Sugar Company

- American Crystal Sugar Company

- Louis Dreyfus Company

- Mitr Phol Group

- Couplet Sugars SA

- Manildra Group

- Sunshine Sugar (Manildra Harwood)

- Wholesome Sweeteners Inc.

- Ragus Sugars Ltd.

- SBEC Sugar Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumption of bakery and confectionery products

- 4.2.2 Growth of cafe culture and foodservice outlets

- 4.2.3 Development of organic, low-calorie, and flavored icing sugars

- 4.2.4 Growth in celebration culture

- 4.2.5 Growing influence of social media food trends

- 4.2.6 Increasing demand for ready-to-eat desserts

- 4.3 Market Restraints

- 4.3.1 Growing health concerns related to sugar consumption

- 4.3.2 Regulatory pressure on sugar reduction

- 4.3.3 Short shelf life and moisture sensitivity

- 4.3.4 Fluctuations in raw material quality

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Supply-Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Category

- 5.1.1 Conventional

- 5.1.2 Organic

- 5.2 By Product Type

- 5.2.1 6X Granulation

- 5.2.2 10X Granulation

- 5.2.3 12X / Ultra-fine

- 5.3 By Application

- 5.3.1 Bakery

- 5.3.2 Confectionery

- 5.3.3 Beverages

- 5.3.4 Dairy and Frozen Desserts

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 B2B / Industrial/HoReCa

- 5.4.2 Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sudzucker AG

- 6.4.2 Tereos S.A.

- 6.4.3 Cargill, Incorporated

- 6.4.4 American Sugar Refining, Inc. (Domino Foods)

- 6.4.5 Tate & Lyle PLC

- 6.4.6 Nordzucker AG

- 6.4.7 Associated British Foods plc (British Sugar)

- 6.4.8 Wilmar International Ltd.

- 6.4.9 Rogers Sugar Inc.

- 6.4.10 Cosan S.A.

- 6.4.11 Imperial Sugar Company

- 6.4.12 American Crystal Sugar Company

- 6.4.13 Louis Dreyfus Company

- 6.4.14 Mitr Phol Group

- 6.4.15 Couplet Sugars SA

- 6.4.16 Manildra Group

- 6.4.17 Sunshine Sugar (Manildra Harwood)

- 6.4.18 Wholesome Sweeteners Inc.

- 6.4.19 Ragus Sugars Ltd.

- 6.4.20 SBEC Sugar Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK