PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061999

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061999

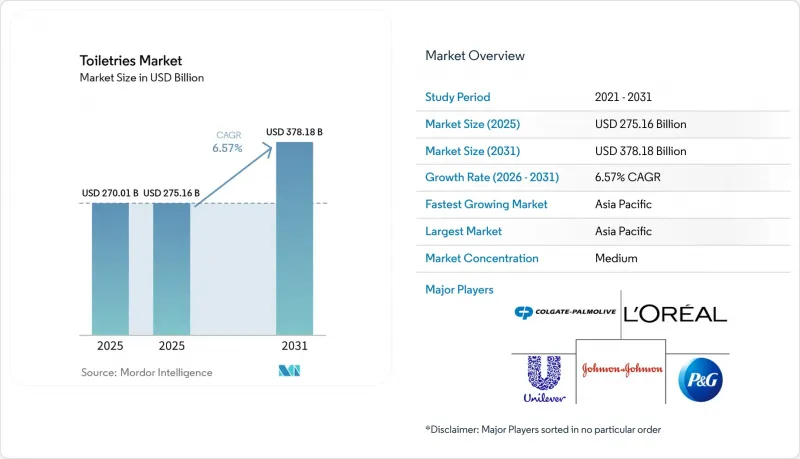

Toiletries - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global toiletries market size is expected to grow from USD 270.01 billion in 2025 and USD 275.16 billion in 2026 to USD 378.18 billion by 2031, registering a CAGR of 6.57% between 2026 and 2031.

This report is Segmented by Product Type (Soaps and Body Wash, Shampoos and Conditioners, Toothpaste and Toothbrushes, and More), by Category (Mass and Premium), by End User (Kids and Adults), by Distribution Channel (Supermarkets/Hypermarkets, Health and Beauty Stores, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Toiletries Market Trends and Insights

Increasing awareness about personal hygiene

Post-pandemic hygiene awareness has significantly influenced consumer behavior, supported by government health initiatives emphasizing personal cleanliness. The WHO's focus on hand hygiene and the CDC's updated guidelines on protective practices have driven consistent demand for antibacterial soaps, sanitizing wipes, and specialized cleansing products. This heightened awareness also extends to oral care, with the Chinese government's promotion of specialized oral care products contributing to growth in the children's oral care market. The trend is particularly pronounced in emerging markets, where increasing education levels and urbanization are establishing new hygiene standards. Additionally, digital health platforms and telemedicine consultations have enhanced awareness of the link between personal hygiene and overall health outcomes. Public health campaigns supported by governments in countries such as India and Brazil have institutionalized hygiene practices, fostering long-term behavioral changes and sustaining market demand beyond immediate health emergencies.

Preference for natural and organic products

Consumer preference for natural and organic toiletries is driving innovation and premium product development in the global market. Increasing awareness of skin health, sustainability, and ingredient transparency has led consumers to favor products made with plant-based ingredients, botanical extracts, essential oils, and chemical-free formulations. This trend has prompted manufacturers to reformulate products and invest in cleaner, safer, and environmentally responsible alternatives. Regulatory changes are further supporting this shift. For example, the European Union's Regulation 2023/1545 requires the labeling of 56 fragrance allergens when concentrations exceed specified thresholds, enhancing transparency in personal care and toiletry products. Similarly, the United Kingdom's Regulation 2024/1334 imposes restrictions on fragrance allergens and certain UV filters, requiring full ingredient disclosure . These regulations have also encouraged brands to adopt certifications such as COSMOS and NATRUE to demonstrate compliance and build consumer trust. Consequently, the demand for certified natural and organic toiletries is growing, particularly among health-conscious and environmentally aware consumers seeking clean-label toiletries products.

Product imitations and counterfeiting

Counterfeit toiletries products negatively impact brand equity, compromise consumer safety, and divert revenue from legitimate manufacturers, while enforcement efforts struggle to keep up with the rapid growth of digital distribution channels. In 2024, South Korea's customs authority initiated a permanent crackdown on counterfeit cosmetics, targeting fake K-beauty products sold via social media and cross-border e-commerce platforms. However, the volume of seizures highlights the persistence of counterfeit supply chains. Counterfeiting has become a significant issue in the toiletries sector, with the European Union Intellectual Property Office (EUIPO) reporting annual losses of EUR 3 billion for the cosmetics industry. This figure accounts for 4.8% of legitimate sales and has led to 32,000 job losses across the EU, according to the 2024 EUIPO Counterfeiting Report . Counterfeiting continues to hinder growth in the premium segment, as consumers in price-sensitive markets opt for counterfeit products that replicate packaging but offer inferior formulations, delaying the trust-building necessary for category expansion.

Other drivers and restraints analyzed in the detailed report include:

- Innovations and launches in products

- Recovery in the travel, tourism, and hospitality sectors

- Environmental regulations increasing packaging costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Personal hygiene products accounted for 35.16% of the projected 2025 revenue, highlighting their significance as a key contributor to the global toiletries market size. These products, which include essential items such as soaps, deodorants, and sanitary products, form the foundation of the market due to their consistent demand and necessity in daily routines. Shampoos and conditioners, while currently smaller in market share, are expected to grow at a CAGR of 6.88%, driven by the increasing popularity of sulfate-free and probiotic formulations, particularly in emerging cities across Asia. This growth is further supported by rising consumer awareness of product ingredients and their impact on health and the environment.

Advancements in micellar technology and salon-grade formulations are contributing to higher per-unit prices, even in traditionally cost-sensitive markets, thereby increasing the market share of premium haircare brands. These innovations cater to a growing segment of consumers seeking professional-grade results at home, which has become a significant trend in the personal care industry. At the same time, commoditized categories such as toothpaste are shifting towards subscription-based electric toothbrushes to maintain profit margins. This shift reflects an effort to enhance customer retention and provide added value through convenience and advanced oral care solutions.

The mass tier is projected to account for 69.29% of 2025 sales, driven by the widespread availability of products in supermarkets and convenience stores. This dominance is attributed to the affordability and accessibility of mass-tier products, which cater to a broad consumer base. In contrast, premium SKUs are expected to grow at a CAGR of 7.45%, supported by the increasing adoption of refillable pods and clinically validated serums. These innovations not only justify higher price points but also appeal to environmentally conscious and health-focused consumers, contributing to the expansion of the personal care products market at the premium end.

Multinational companies are developing premium sub-lines to maintain their shelf presence and compete in the evolving market landscape. These efforts are aimed at addressing the growing demand for high-quality, specialized products. Meanwhile, direct-to-consumer (D2C) challengers are leveraging influencer marketing channels to attract early adopters, particularly within affluent urban clusters. This strategy enables D2C brands to gain a foothold in the market, often at the expense of incumbents' market share in these high-value segments.

Geography Analysis

Asia-Pacific accounts for 37.40% of the current revenue and is projected to strengthen its position with a region-leading CAGR of 6.81%. This growth is driven by multiple factors, including India's USD 40 billion online beauty market, which is expanding rapidly due to increasing internet penetration and rising consumer preference for e-commerce platforms. TikTok-driven product discovery is playing a significant role in influencing purchasing decisions, particularly among younger demographics. Additionally, mandatory Halal certification requirements in Indonesia and Malaysia are shaping product formulations and marketing strategies, catering to the growing demand for Halal-compliant toiletries. Urban Chinese consumers are shifting their preferences from foreign brands to science-driven local labels, reflecting a growing trust in domestic innovation and quality. Meanwhile, Japanese companies are leveraging K-beauty sensory elements, such as unique textures and fragrances, to modernize and relaunch their heritage brands, aiming to appeal to both domestic and international markets.

North America and Europe are experiencing steady growth, influenced by premiumization trends and regulatory compliance challenges. California's PFAS ban and the EU's CMR prohibition have significantly increased reformulation costs for manufacturers, as they work to eliminate harmful substances from their products. However, these stringent regulations are creating opportunities for early adopters of natural and clean beauty products, which already meet compliance standards. This shift is driving the toiletries market toward higher average selling prices (ASPs) as consumers increasingly prioritize safety and sustainability. Furthermore, the recovery of travel retail across European and Middle Eastern hubs has revitalized demand for prestige miniatures and gift sets, particularly among international travelers seeking convenient and luxurious options.

Latin America and the Middle East & Africa present significant growth opportunities, driven by expanding urban middle classes and the implementation of formalized regulatory frameworks. In Brazil, the use of Amazonian botanicals is gaining traction as a key differentiator, helping local brands compete with imports by offering unique, sustainable, and culturally resonant products. Meanwhile, Nigeria's QR authentication system is addressing the widespread issue of counterfeit products, enhancing consumer trust and gradually steering purchasing behavior back to legitimate channels. These developments are fostering a more structured and reliable toiletries market in these regions, paving the way for sustained growth.

- The Procter & Gamble

- Unilever plc

- Colgate-Palmolive Company

- Kenvue Inc

- L'Oreal S.A.

- Johnson & Johnson

- Reckitt Benckiser Group plc

- Henkel AG & Co. KGaA

- Kao Corporation

- Beiersdorf AG

- Church & Dwight Co., Inc.

- Edgewell Personal Care

- Combe Inc.(Virtue)

- Shiseido Company, Ltd.

- Amorepacific Corporation

- Natura & Co

- Godrej Consumer Products

- Dabur India Ltd.

- The Honest Company

- Himalaya Wellness

- Marico Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing awareness about personal hygiene

- 4.2.2 Preference for natural and organic products

- 4.2.3 Innovations and launches in products

- 4.2.4 Rising demand for personalized and customized products

- 4.2.5 Recovery in the travel, tourism, and hospitality sectors

- 4.2.6 Growth in men's grooming and baby care product adoption

- 4.3 Market Restraints

- 4.3.1 Product imitations and counterfeiting

- 4.3.2 Environmental regulations increasing packaging costs

- 4.3.3 High cost of premium and natural products

- 4.3.4 Pressure to replace performance-critical ingredients

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Soaps and body wash

- 5.1.2 Shampoos and conditioners

- 5.1.3 Toothpaste and toothbrushes

- 5.1.4 Deodorants and antiperspirants

- 5.1.5 Shaving supplies

- 5.1.6 Personal hygine products

- 5.2 By Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 By End User

- 5.3.1 Kids

- 5.3.2 Adults

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Health and Beauty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 The Procter & Gamble

- 6.4.2 Unilever plc

- 6.4.3 Colgate-Palmolive Company

- 6.4.4 Kenvue Inc

- 6.4.5 L'Oreal S.A.

- 6.4.6 Johnson & Johnson

- 6.4.7 Reckitt Benckiser Group plc

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Kao Corporation

- 6.4.10 Beiersdorf AG

- 6.4.11 Church & Dwight Co., Inc.

- 6.4.12 Edgewell Personal Care

- 6.4.13 Combe Inc.(Virtue)

- 6.4.14 Shiseido Company, Ltd.

- 6.4.15 Amorepacific Corporation

- 6.4.16 Natura & Co

- 6.4.17 Godrej Consumer Products

- 6.4.18 Dabur India Ltd.

- 6.4.19 The Honest Company

- 6.4.20 Himalaya Wellness

- 6.4.21 Marico Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK