PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062006

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062006

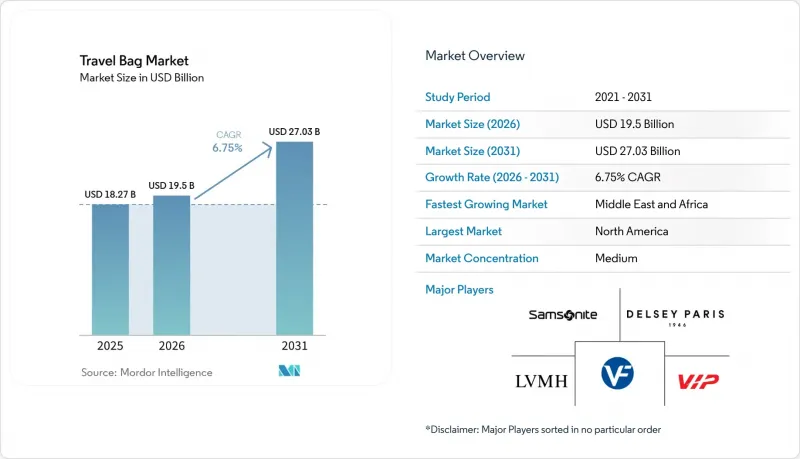

Travel Bag - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the travel bag market size is projected to expand from USD 18.27 billion in 2025 and USD 19.50 billion in 2026 to USD 27.03 billion by 2031, registering a CAGR of 6.75% between 2026 and 2031.

This report is Segmented by Material Type (Hard, Soft), End User (Adults, Kids), Category (Mass, Premium), Distribution Channel (Offline Retail Stores, Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Travel Bag Market Trends and Insights

Adventure and Experiential Travel Trends

As travelers increasingly prioritize gear that can endure rugged environments, luggage design is shifting towards durability and modularity, moving away from traditional hard-shell aesthetics. From 2020 to 2025, the global adventure travel sector experienced a robust annual growth rate of 15%, outpacing the leisure travel segment. Notably, millennials and Gen Z made up a significant 62% of these bookings. In response to this demographic trend, brands are introducing hybrid products. For instance, Osprey's Transporter series melds the flexibility of soft-shells with the protective zones of hard-shells, even incorporating backpack harness systems into wheeled luggage for versatile journeys. Reflecting this shift, Samsonite revealed that a notable 40% of its 2024 sales stemmed from products made with recycled materials, catering to adventure travelers who prioritize sustainability alongside performance. Furthermore, there's a rising demand for smaller bags that comply with carry-on restrictions. This trend aligns with adventure travelers' preference for budget airlines, allowing them to invest more in experiences rather than incurring checked-baggage fees.

Low-Cost Carrier Expansion Stimulating Lightweight Carry-On Sales

In 2025, low-cost carriers tightened cabin-bag policies, with 42% of passengers paying an average gate fee of EUR 47 (USD 51) for oversized carry-ons, up from 38% in 2024, according to the European Consumer Organisation. Ryanair restricted free cabin bags to 40 cm X 20 cm X 25 cm unless priority boarding was purchased, while Spirit and Frontier in the U.S. reduced personal-item sizes to 45 cm X 35 cm X 20 cm. These changes pushed manufacturers to create compact designs maximizing internal space. Travelers are shifting from 55 cm spinners to lighter 50 cm and 48 cm models, offering 30-35 liters of capacity with features like compression panels and expandable compartments. In April 2026, Delsey Paris launched its "Elegance" collection with Air France, featuring IATA-compliant cabin suitcases priced from EUR 249 (USD 270) and lined with 100% recycled polyester. This targets the 68% of European travelers who check luggage dimensions online before buying. The rise of low-cost carriers is also boosting demand for hard-shell carry-ons, as polycarbonate models better withstand overhead-bin compression, reducing warranty claims and improving brand reputation.

Dominance of Unorganized Low-End Players

Unorganized manufacturers dominate price-sensitive markets like India, Indonesia, and Nigeria, controlling 40-50% of unit volumes by offering products 30-50% cheaper than branded players through informal distribution and low quality-control costs. In fiscal 2024, VIP Industries held over 50% of India's branded luggage market, but its revenue in calendar 2024 fell 18% year-on-year to USD 210 million due to competition from unorganized players selling soft-shell bags at Rs 800-1,200 (USD 10-14), compared to VIP's Rs 2,500-4,000 (USD 30-48) models. These unorganized players rarely invest in R&D or sustainable materials, creating a two-tier market where urban consumers pay premiums for warranties and design, while rural buyers opt for cheaper, short-lived products. VIP's 32% stake sale to a Multiples Equity-led consortium for Rs 1,437.78 crore (USD 173 million) in August 2025 signals confidence in market formalization, driven by stricter e-commerce quality standards and improved tax compliance.

Other drivers and restraints analyzed in the detailed report include:

- Rapid E-Commerce Cross-Border Shipping of Baggage and Packaging Solutions

- Rising Global Tourism and Travel Frequency

- Counterfeit branded bags diluting premium price realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, soft-sided luggage dominated 67.90% of global market revenue due to its affordability, expandability, and lightweight design. Priced at USD 40-80, nylon and polyester duffels are far cheaper than hard-shell options costing USD 120-250, making them popular in cost-sensitive regions like India, Southeast Asia, and Latin America. These bags offer 15-20% extra capacity using external straps, making them ideal for long trips with varying packing needs. Additionally, low-cost carriers' baggage restrictions favor soft-sided carry-ons, as collapsible duffels fit under seats and help travelers avoid gate-check fees, which 42% of European passengers paid in 2025, averaging EUR 47. However, the EU's REACH directive, which limits phthalates in PVC linings, has pushed manufacturers toward costlier thermoplastic polyurethane alternatives, increasing production costs by 12-18% and reducing profit margins.

Hard-shell luggage is expected to grow at a 7.02% CAGR through 2031, outpacing the overall market. Polycarbonate innovations have reduced weight by 20-30% since 2015 while maintaining durability, making them ideal for checked baggage in cold cargo holds. Covestro's Makrolon polycarbonate enables thinner shell walls, cutting material costs by 15-20% and meeting airline weight limits for bags under 23 kg. Samsonite's Curv material, a self-reinforcing polypropylene, provides superior impact absorption. In 2025, Samsonite expanded its Nashik, India plant to produce 700,000 units monthly, with 60% focused on polycarbonate carry-ons. Recycled-content mandates are also driving hard-shell demand. Covestro's Shanghai facility produces 25,000 tonnes of post-consumer polycarbonate annually, allowing brands to market eco-friendly products with 20-35% price premiums in Western Europe and North America, where 68% of consumers consider environmental impact before purchasing premium luggage. Online shoppers prefer hard-shell luggage for better shipping protection, reducing damage-related returns by 12-18%, while in-store buyers favor soft-sided bags for their flexibility and compressibility.

In 2025, adults made up 91.87% of end-user demand for luggage, primarily using it as a practical tool for both business and leisure travel. Frequent flyers, who take four or more international trips each year, typically replace their luggage every 3 to 5 years, while occasional travelers do so every 5 to 7 years. Although they constitute only 18% of global passengers, frequent flyers account for a significant 38% of premium luggage purchases. They tend to favor modular ecosystems-like carry-ons, checked bags, and garment sleeves-from a single brand, ensuring both stackability and a cohesive look. Business travelers, justifying price points between USD 200 and USD 400, seek organizational features in their luggage. These include laptop compartments with shock-absorbing foam, garment folders to reduce wrinkles, and USB charging ports integrated into telescoping handles.

Driven by partnerships with Disney, Marvel, and Pixar, the kids' luggage segment is set to grow at a 7.5% CAGR through 2031. These collaborations elevate luggage from mere travel items to coveted products, with retail prices ranging from USD 79 to USD 109. For instance, the Disney Store's Minnie Mouse rolling suitcase is priced at USD 79, while hard-shell models from Samsonite, licensed under Disney's Frozen and Toy Story, retail between USD 89 and USD 129. Such licensing allows these brands to command a 30% to 40% premium over generic kids' luggage, which typically retails between USD 49 and USD 69. The segment enjoys a protective edge against unorganized manufacturers due to regulatory barriers. The U.S. Consumer Product Safety Commission's 16 CFR Part 1500 imposes strict mandates on children's products, including lead-content limits, phthalate restrictions, and small-parts testing. These compliance measures add an estimated USD 5 to USD 10 per unit in costs. Targeting eco-conscious parents, Ful offers PVC-free kids' luggage priced between USD 59 and USD 79. This niche, emphasizing phthalate-free materials, saw an 18% year-on-year growth in 2025, driven by heightened awareness of chemical safety in children's products.

Geography Analysis

In 2025, North America accounted for 41.98% of global revenue, supported by the U.S.'s advanced travel infrastructure and high luggage ownership. However, growth is slowing as consumers prioritize durable products and extend replacement cycles. U.S. sales were flat from January to June 2025 after a 6% decline in 2023-2024, reflecting market saturation in urban areas. Canada and Mexico added volume through cross-border tourism and e-commerce, though tariff uncertainties under USMCA renegotiations created pricing challenges for manufacturers relying on Chinese components. Direct-to-consumer brands like Monos (Toronto), Away (New York), and July (San Francisco) capitalized on access to venture capital and affluent consumers, offering premium carry-ons priced at USD 250 to USD 400. North America leads in smart luggage adoption, with 28% of travelers showing interest in GPS-enabled cases, though restrictions on non-removable lithium batteries limit broader adoption.

The Middle East and Africa are expected to grow the fastest, with an 8.23% CAGR through 2031. Saudi Arabia's travel and tourism GDP reached USD 178 billion in 2025, up 7.4% year-on-year, with international arrivals 39% higher than 2019 levels. Vision 2030 projects like NEOM and Red Sea resorts boosted business travel by 55%, while religious tourism to Mecca and Medina sustained demand for durable luggage. The UAE recorded an 8.2% rise in visitor spending, driven by Dubai's role as a global transit hub and Abu Dhabi's cultural investments. Africa saw 81 million arrivals in 2025, an 8% increase, with North Africa leading at 11% growth. Egypt experienced a 20% rise to 19 million visitors, supported by proximity to Europe and favorable currency rates. However, unorganized manufacturers dominate 60-70% of the luggage market in Nigeria, Kenya, and South Africa, limiting international brands' pricing power.

Asia-Pacific, Europe, and South America showed varied trends. China's domestic travel rebounded to 6.2 billion trips in 2025, but luggage sales grew only 3% as consumers focused on experiences over goods. India became Samsonite's largest manufacturing hub, with its Nashik plant exporting 10% of output to Southeast Asia and the Middle East. VIP Industries, holding over 50% market share, faces competition from private-equity-backed consolidations. In Europe, stricter baggage rules by Ryanair and easyJet led 42% of passengers to pay gate fees averaging EUR 47, driving demand for compliant carry-ons. South America's growth remained modest due to currency volatility and tariffs. Brazil's 35% duty on non-Mercosur luggage raised prices by 50-70%, encouraging local assembly by VIP Industries and Safari, though quality gaps persist compared to imports.

- Samsonite International S.A.

- VIP Industries Ltd.

- VF Corporation

- LVMH (Moet Hennessy Louis Vuitton)

- Away Travel

- Travelpro

- Delsey Paris

- Briggs & Riley

- Calpak (California Pak International, Inc)

- Monos

- Beis Luggage

- Victorinox AG

- Antler

- Carlton

- Flight Knight

- Solgaard

- Osprey Packs, Inc

- Bellroy

- July Luggage

- Safari

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adventure and experiential travel trends

- 4.2.2 Low-cost carrier expansion stimulating light-weight carry-on sales

- 4.2.3 Rapid e-commerce cross-border shipping of baggage and packaging solutions

- 4.2.4 Rising global tourism and travel frequency

- 4.2.5 Technological innovations and smart features

- 4.2.6 Carbon-neutral luggage lines capturing sustainability-led consumer switch

- 4.3 Market Restraints

- 4.3.1 Dominance of unorganized low-end players

- 4.3.2 Counterfeit branded bags diluting premium price realization

- 4.3.3 Volatile petrochemical prices inflating ABS/PC resin costs

- 4.3.4 Regulatory pressures on materials and safety

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Hard

- 5.1.2 Soft

- 5.2 By End User

- 5.2.1 Adults

- 5.2.2 Kids

- 5.3 By Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Products, Recent Developments)

- 6.4.1 Samsonite International S.A.

- 6.4.2 VIP Industries Ltd.

- 6.4.3 VF Corporation

- 6.4.4 LVMH (Moet Hennessy Louis Vuitton)

- 6.4.5 Away Travel

- 6.4.6 Travelpro

- 6.4.7 Delsey Paris

- 6.4.8 Briggs & Riley

- 6.4.9 Calpak (California Pak International, Inc)

- 6.4.10 Monos

- 6.4.11 Beis Luggage

- 6.4.12 Victorinox AG

- 6.4.13 Antler

- 6.4.14 Carlton

- 6.4.15 Flight Knight

- 6.4.16 Solgaard

- 6.4.17 Osprey Packs, Inc

- 6.4.18 Bellroy

- 6.4.19 July Luggage

- 6.4.20 Safari

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK