PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062021

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062021

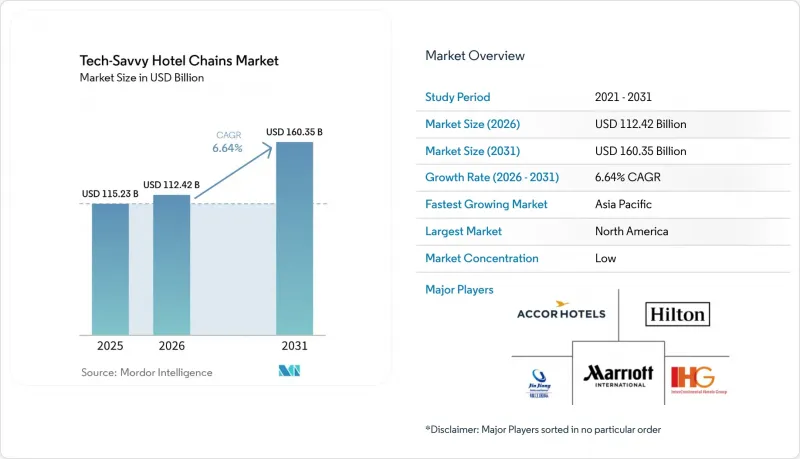

Tech-Savvy Hotel Chains - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031)

According to Mordor Intelligence, the tech-Savvy chain hotel market was valued at USD 115.23 billion in 2025 and is estimated to grow from USD 122.42 billion in 2026 to reach USD 169.51 billion by 2031, at a CAGR of 6.64% during the forecast period (2026-2031).

This report is Segmented by Category (luxury & Upper-Upscale, Upscale, Mid-Scale, and Economy & Budget), End-User (business Travelers, and Leisure Travelers), Hotel-Chain Type (greater Than 500 Properties, 101-500 Properties, and Other), and Geography (North America, Europe, Asia Pacific, South America, and Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Tech-Savvy Hotel Chains Market Trends and Insights

Mobile-First Guest Journeys Enabling Seamless Digital Check-In, Check-Out, and Key Access

Mobile-first guest experiences have become a standard expectation as hotels adopt digital keys, app-based messaging, and self-service options to streamline arrival and departure. Wallet-based digital keys reduce wait times, simplify room access, and enhance security and operational auditability. Mews introduced native Apple and Google Wallet room keys without third-party middleware, with Hey Lou Hotels showcasing seamless walk-in experiences that eliminate queues and plastic cards. Resorts World Las Vegas demonstrated how digital keys integrate into systems, enabling automatic room updates and functioning on iPhone power reserve for resilience. Mobile app ecosystems drive ancillary revenue through in-room dining, spa bookings, and personalized offers, while platforms like INTELITY centralize mobile check-in, keys, and communications, reducing front desk workload and improving service. Privacy-by-design remains essential with clear notices, opt-in consent, and encrypted data flows, ensuring compliance and trust.

Adoption of Cloud-Based PMS and Fully Integrated Hospitality Technology Ecosystems

Cloud-based Property Management Systems (PMS) are gaining traction as hotels transition from on-premise servers to managed, API-first platforms that standardize data and streamline integrations across reservations, POS, CRM, and revenue systems. Rapid transformation is feasible with vendor-managed services, as seen in Motel One's migration of over 100 properties across 13 countries to Oracle OPERA Cloud in four months, averaging 14 go-lives per week. Integrated platforms enhance analytics, forecasting, staff scheduling, and service recovery while reducing downtime risks and ownership costs by eliminating server maintenance and patching. Unified data layers simplify feature deployment, support AI workflows, and ensure compliance through stronger governance, disaster recovery SLAs, and vendor certifications across regions.

Elevated Cybersecurity Risks and Increasing Data Privacy Compliance Requirements

Cyber risk is a significant concern for hotel chains, which manage payments, identity verification, loyalty data, and digital touchpoints, increasing vulnerability to attacks. A breach at Pyramid Global Hospitality exposed sensitive personal and financial information, highlighting the need for monitoring, privileged access control, and rapid response. Compliance adds complexity, with GDPR requiring breach notifications, vendor agreements, and data processing records. Hotels now adopt privacy-by-design, encryption, and prioritize vendors with security certifications, disaster recovery plans, and data residency policies. Employee training and culture-building are critical as human error drives incidents, while multifactor authentication, endpoint protection, and network segmentation help minimize breach impacts.

Other drivers and restraints analyzed in the detailed report include:

- AI- and Analytics-Driven Personalization Across Guest Engagement and Service Delivery

- Automation-Led Cost Optimization via Robotics and IoT-Enabled Energy Management

- High Capital Investment and Retrofit Costs for Upgrading Legacy Hotel Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luxury and upper-upscale properties are expected to hold a 30.55% share of the tech-savvy chain hotel market size in 2025, driven by early adoption of AI concierges, mobile-first guest journeys, and predictive service models that enhance premium experiences. Central platforms distribute innovation costs across hotels, enabling faster deployment of features like wallet-based digital keys and unified commerce data for targeted offers. Investments in building automation and ESG reporting help meet sustainability expectations for both customers and corporate travel. Integrated POS and PMS systems are increasingly used to link dining, spa, and activity transactions with loyalty programs, supporting curated guest experiences. These platforms also improve service recovery and personalization by equipping staff with complete guest context during escalations from AI agents to human team members, maintaining the quality of premium service.

The mid-scale segment, growing at a projected CAGR of 7.21% through 2031, benefits from cloud-native technology stacks that reduce conversion cycles and standardize digital capabilities across properties. Operators prioritize mobile check-in, keyless entry, and unified messaging to streamline arrivals and boost cross-sell conversions. Scalable cloud PMS solutions with pre-integrated interfaces enhance forecasting and housekeeping efficiency. Automation in energy management and maintenance alerts reduces costs and allows staff to focus on guest interactions that drive reviews and repeat bookings.

Geography Analysis

North America held 34.25% of the Tech-Savvy Hotel Chains market share due to early adoption of cloud Property Management Systems (PMS), mobile-first customer journeys, and loyalty-focused personalization programs. U.S. operators are enhancing arrival experiences and reducing front desk congestion through digital keys and unified messaging systems, aligning with app-based service preferences. Cloud migrations ensure consistent analytics and uptime across properties, enabling real-time performance management and service recovery. Security efforts focus on identity management and incident readiness across applications and partner systems, addressing the sector's broad attack surface. Recent breaches underscore the need for vetted vendors and strong data governance. Canada and Mexico contribute through independent hotel modernization and mobile-first strategies, meeting traveler expectations for digital convenience and responsive services.

Europe shows varied adoption rates, with Northern markets advancing in cloud PMS and operational analytics, while Southern markets face challenges balancing upgrades with local ownership constraints. Germany's Kimpton Hotel Frankfurt integrates advanced building automation, including HVAC, lighting, and accessibility features like vibrating pillows for deaf guests, aligning with sustainability and safety standards. Spain leverages digital twins for energy and comfort optimization in hotels, supported by recovery funding and real-world validation, showcasing scalable improvements in cost efficiency and service quality. Europe's regulatory framework emphasizes privacy-by-design in applications and data platforms, enhancing resilience and trust in loyalty programs and mobile-first services. Vendor ecosystems expand to accommodate regional payment preferences and language support, catering to cross-border travel flows and diverse property footprints.

Asia Pacific is the fastest-growing market for Tech-Savvy Hotel Chains, with a projected CAGR of 8.39% through 2031. Giga-projects, digital-native consumer behavior, and rapid new-build activity drive leapfrog adoption of advanced technologies. New projects integrate robotics, elevator systems, and building automation into agentic digital twins, optimizing resource management and reducing congestion. India's enterprise upgrades demonstrate how cloud-enabled scalability reduces infrastructure costs and accelerates rollout for expanding hotel portfolios. Southeast Asia adopts mobile-first engagement strategies from inception, aligning with smartphone-centric travel behaviors and bypassing legacy systems. Australia, South Korea, and Japan integrate with global vendor ecosystems to support cross-channel distribution and unified guest data, facilitating seamless travel across key regional corridors.

- Marriott International

- Hilton Worldwide

- Accor Hotels

- InterContinental Hotels Group (IHG)

- Jin Jiang International

- Hyatt Hotels Corp.

- Wyndham Hotels & Resorts

- Choice Hotels Intl.

- Radisson Hotel Group

- Minor Hotels

- Whitbread plc (Premier Inn)

- Shangri-La Group

- Four Seasons Hotels & Resorts

- Mandarin Oriental Hotel Group

- Melia Hotels International

- Louvre Hotels Group

- citizenM Hotels

- OYO Hotels & Homes

- Sonder Holdings

- Red Lion Hotels Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mobile-first guest journeys enabling seamless digital check-in, check-out, and key access

- 4.2.2 Adoption of cloud-based PMS and fully integrated hospitality technology ecosystems

- 4.2.3 AI- and analytics-driven personalization across guest engagement and service delivery

- 4.2.4 Automation-led cost optimization via robotics and IoT-enabled energy management

- 4.2.5 Use of digital twins to enhance real-time operational efficiency and asset performance

- 4.2.6 Deployment of ESG-linked AI tools supporting sustainability tracking and green financing access

- 4.3 Market Restraints

- 4.3.1 Elevated cybersecurity risks and increasing data privacy compliance requirements

- 4.3.2 High capital investment and retrofit costs for upgrading legacy hotel infrastructure

- 4.3.3 Vendor lock-in risks and lack of interoperability across fragmented technology systems

- 4.3.4 Shortage of skilled workforce to manage and operate advanced digital solutions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Insights on Technology Applications in Guest Experience, Operations, Energy Automation, and Security

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Hotel Category

- 5.1.1 Luxury & Upper-Upscale

- 5.1.2 Upscale

- 5.1.3 Mid-scale

- 5.1.4 Economy & Budget

- 5.2 By End-User

- 5.2.1 Business Travelers

- 5.2.2 Leisure Travelers

- 5.3 By Hotel-chain Tier

- 5.3.1 Greater Than 500 properties

- 5.3.2 101 - 500 properties

- 5.3.3 Less Than 100 properties

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Marriott International

- 6.4.2 Hilton Worldwide

- 6.4.3 Accor Hotels

- 6.4.4 InterContinental Hotels Group (IHG)

- 6.4.5 Jin Jiang International

- 6.4.6 Hyatt Hotels Corp.

- 6.4.7 Wyndham Hotels & Resorts

- 6.4.8 Choice Hotels Intl.

- 6.4.9 Radisson Hotel Group

- 6.4.10 Minor Hotels

- 6.4.11 Whitbread plc (Premier Inn)

- 6.4.12 Shangri-La Group

- 6.4.13 Four Seasons Hotels & Resorts

- 6.4.14 Mandarin Oriental Hotel Group

- 6.4.15 Melia Hotels International

- 6.4.16 Louvre Hotels Group

- 6.4.17 citizenM Hotels

- 6.4.18 OYO Hotels & Homes

- 6.4.19 Sonder Holdings

- 6.4.20 Red Lion Hotels Corp.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment