PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062047

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062047

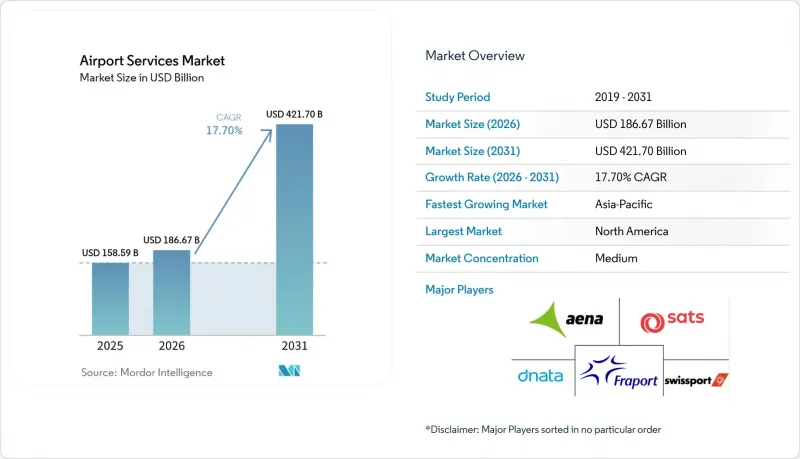

Airport Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the airport services market size is expected to grow from USD 158.59 billion in 2025 to USD 186.67 billion in 2026 and is forecast to reach USD 421.70 billion by 2031 at 17.70% CAGR over 2026-2031.

This report is Segmented by Service Type (Aircraft Ground Handling Services, Aircraft Maintenance Services, Passenger Services, and More), Revenue Stream (Aeronautical Services and Non-Aeronautical Services), Airport Size (Large Airports, and More), Infrastructure Type (Greenfield Airport, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Airport Services Market Trends and Insights

Surging Air Passenger Traffic in Emerging Asia-Pacific and Middle East Hubs

The airport services market is being lifted by traffic growth, now more clearly centered in Asia-Pacific and the Middle East. Asia-Pacific RPK grew 7.8% in 2025, while Middle Eastern carriers posted 6.8% growth, both well ahead of North America at 0.4%. IATA expects Asia-Pacific demand to rise by another 7.3% in 2026, keeping the region as the fastest-growing large aviation market. This volume increase directly lifts demand for passenger handling, turnaround support, baggage operations, and premium airport services at major hubs. It also raises pressure on constrained airports, where service revenues per passenger can rise faster because airlines and concession operators value speed and reliability more highly. In the airport services market, this creates stronger pricing power for operators serving busy gateway airports than for those focused only on underused secondary facilities.

E-commerce-Led Growth in Cross-border Air Cargo

The airport services market is also gaining momentum from cargo flows that are becoming more time-sensitive and e-commerce-driven. Global air cargo demand reached a record level in 2025, rising 3.4% year over year, with Asia-Europe demand up 10.3%. E-commerce is expected to account for 30% of total air cargo volumes by 2027, up from 20% in 2024, which is changing the operating mix at large freight gateways. In the airport services market, that shift favors automated sorting, express handling, and cargo terminals that can process fast parcel flows with lower dwell time. It also changes investment priorities, as airports now need greater digital coordination among airlines, handlers, and customs-facing processes. Cargo handling is therefore becoming a stronger growth engine than it was in the pre-e-commerce period.

Volatile Aviation Fuel Prices Squeezing Airline Handling Budgets

Fuel volatility is the most immediate financial restraint on the airport services market in 2026. Jet fuel prices nearly doubled between February and March 2026, with the global jet fuel index rising 95.2% to USD 195.2 per barrel after disruption around the Strait of Hormuz. Airports Council International Europe warned that a systemic jet fuel shortage could affect the EU if normal flows did not resume. At the same time, the International Energy Agency estimated Europe had only six weeks of supply at that stage. When airlines face this kind of cost shock, they often trim marginal routes, reduce frequencies, and demand tighter handling costs from contractors. In the airport services market, revenue per aircraft movement is compressed while labor and equipment costs remain elevated. Ground handlers are especially exposed because they usually cannot recover inflation quickly without renegotiating contracts that may take many months to reopen.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Smart and Digital Airport Technologies

- Sustainability-Linked Financing Propelling Ground Support Electrification

- Acute Skilled Labor Shortage in Ground Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aircraft ground handling services accounted for 28.95% of the airport services market in 2025, making it the largest service segment and the operational base for most airport activity. The segment remains central because every commercial flight depends on ramp handling, aircraft movement support, boarding support, and turnaround coordination. The airport services market still reflects this essential role, as airline hub strategies and preferred service partnerships continue to concentrate large handling volumes with established operators. Aircraft maintenance services also remain important because fleet aging and delivery delays are keeping aircraft in service for longer periods.

Baggage/cargo handling services are the fastest-growing segment, and their airport services market size is projected to expand at an 18.88% CAGR through 2031. That growth is tied closely to e-commerce flows, semiconductor shipments, and the rising need for fast sorting and transfer capacity. Retail services and food and beverage services, while smaller, are growing in importance because they support the broader shift toward commercial airport revenue. Car parking and landside mobility services are also becoming more integrated with rail, EV charging, and new airport access planning. Across the airport services industry, service differentiation is increasingly shaped by who can combine operational reliability with digital support for cargo and passengers.

Aeronautical services represented 58.27% of the market in 2025 and remained the core contractual layer of airport economics. Landing fees, terminal charges, and related regulated charges still provide the largest revenue base for many airports. The airport services market continues to rely on this stream because it is embedded in airline-airport operating relationships and in regulated pricing structures. Even so, airline pushback to higher airport charges is limiting how far airports can depend on fee-led growth alone.

Non-aeronautical services are the fastest-growing revenue stream in the airport services market, with a 19.98% CAGR through 2031, reflecting a long-running shift toward retail, food and beverage, parking, lounges, and app-based commercial services. Airports are increasingly treating passenger dwell time as an asset that can be monetized more effectively through better layouts and digital engagement. That makes non-aeronautical activity a more resilient growth lever even when airline pricing remains contested. In the airport services industry, digital ancillary products are becoming more important because they scale more easily than traditional concession formats.

Geography Analysis

North America held 39.78% of the airport services market share in 2025 and remained the largest regional base. ACI-NA identified USD 173.9 billion in airport infrastructure needs for 2025 to 2029. The region is therefore investing heavily even though passenger growth is now much slower than in emerging regions. That is pushing the airport services market in North America toward modernization, technology deployment, and higher-value commercial services rather than simple volume expansion.

Asia-Pacific is the fastest-growing regional segment, and the airport services market size in the region is projected to expand at a 20.01% CAGR through 2031. The region accounted for 34.4% of global RPK in 2025, and its air cargo demand grew by 8.4%, well above the global average. ACI Asia-Pacific and the Middle East have identified USD 240 billion in planned airport infrastructure investment through 2035, which supports a long runway for service contracts across terminals, cargo, and airside systems. The airport services market in Asia-Pacific is also supported by higher load factors and tighter turnaround needs at major hubs, which raises the value of reliable ground handling and passenger flow management. This combination of traffic growth, airport construction, and operational intensity keeps the region at the center of future contract expansion.

Europe remained the second-largest regional market and entered 2026 with the highest absolute airline net profitability at USD 14 billion, supporting demand for a broad range of airport services. The airport services market in Europe is still shaped by higher regulatory complexity than most other regions, especially around emissions compliance and airport charging debates. The Middle East continues to stand out for hub-led expansion, with airline profit margins projected at 9.3% in 2026, which supports premium passenger and ground service demand. Africa also posted strong traffic momentum, with flight demand growth at 9.4% in 2025, which improves the medium-term outlook for service demand at developing gateways. South America is benefiting from traffic recovery and network expansion, but the airport services market there remains smaller and more uneven than in North America, Europe, and Asia-Pacific.

- Swissport International AG

- dnata (The Emirates Group)

- John Menzies Limited

- SATS Ltd.

- Fraport Ground Services GmbH

- Aena S.M.E., S.A.

- Groupe ADP (Aeroports de Paris SA)

- LHR Airports Limited

- Changi Airport Group (Singapore) Pte. Ltd.

- Capital Airports Holdings Co., Ltd.

- Avolta AG

- Flughafen Zurich AG

- Kobenhavns Lufthavne A/S

- Avinor AS

- Flughafen Munchen GmbH

- Celebi HavacIlIk Holding A.S

- Acciona, S.A.

- Air General, Inc.

- Hong Kong Air Cargo Terminals Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging air passenger traffic in emerging Asia-Pacific and Middle East hubs

- 4.2.2 Expansion and modernization of airport infrastructure globally

- 4.2.3 E-commerce-led growth in cross-border air cargo

- 4.2.4 Rising demand for ancillary non-aeronautical revenue streams

- 4.2.5 Integration of smart and digital airport technologies

- 4.2.6 Sustainability-linked financing propelling ground support electrification

- 4.3 Market Restraints

- 4.3.1 Volatile aviation fuel prices squeezing airline handling budgets

- 4.3.2 Acute skilled labor shortage in ground operations

- 4.3.3 High capital expenditure for advanced equipment and IT systems

- 4.3.4 Increasing ESG scrutiny inflating service costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Aircraft Ground Handling Services

- 5.1.2 Aircraft Maintenance Services

- 5.1.3 Passenger Services

- 5.1.4 Baggage/Cargo Handling Services

- 5.1.5 Car Parking and Landside Mobility Services

- 5.1.6 Food and Beverage Service

- 5.1.7 Retail Services

- 5.1.8 Others

- 5.2 By Revenue Stream

- 5.2.1 Aeronautical Services

- 5.2.2 Non-Aeronautical Services

- 5.3 By Airport Size

- 5.3.1 Large Airports

- 5.3.2 Medium Airports

- 5.3.3 Small Airports

- 5.4 By Infrastructure Type

- 5.4.1 Greenfield Airports

- 5.4.2 Brownfield Airports

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Qatar

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Swissport International AG

- 6.4.2 dnata (The Emirates Group)

- 6.4.3 John Menzies Limited

- 6.4.4 SATS Ltd.

- 6.4.5 Fraport Ground Services GmbH

- 6.4.6 Aena S.M.E., S.A.

- 6.4.7 Groupe ADP (Aeroports de Paris SA)

- 6.4.8 LHR Airports Limited

- 6.4.9 Changi Airport Group (Singapore) Pte. Ltd.

- 6.4.10 Capital Airports Holdings Co., Ltd.

- 6.4.11 Avolta AG

- 6.4.12 Flughafen Zurich AG

- 6.4.13 Kobenhavns Lufthavne A/S

- 6.4.14 Avinor AS

- 6.4.15 Flughafen Munchen GmbH

- 6.4.16 Celebi HavacIlIk Holding A.S

- 6.4.17 Acciona, S.A.

- 6.4.18 Air General, Inc.

- 6.4.19 Hong Kong Air Cargo Terminals Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment