PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062070

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062070

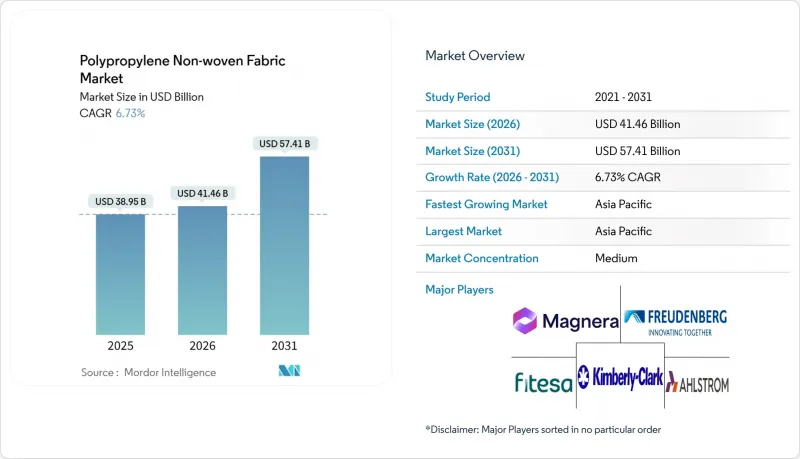

Polypropylene Non-woven Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the polypropylene non-woven fabric market size is expected to grow from USD 38.95 billion in 2025 to USD 41.46 billion in 2026 and is forecast to reach USD 57.41 billion by 2031 at 6.73% CAGR over 2026-2031.

This report is Segmented by Production Technology (Spunbond, Meltblown, SMS (Spun-Melt-Spun), and More), Application (Hygiene, Medical, Packaging, Automotive, Filtration, and Other Applications), Raw Material Type (Homopolymer and Copolymer), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polypropylene Non-woven Fabric Market Trends and Insights

Growing Demand in Hygiene and Medical Disposables

Hygiene and medical disposables continue to underpin volume growth as diaper, feminine care, and incontinence products proliferate in emerging economies while hospital systems institutionalize single-use infection-control protocols. Polypropylene spunbond topsheets provide hydrophobic surfaces with air permeability around 1,868 mm/s, reducing fluid strike-through time versus cellulosic alternatives. Kimberly-Clark's multi-site US manufacturing program, announced in 2025, underlines brand-owner confidence and increases domestic roll-goods procurement. Medical demand is outpacing hygiene on a percentage basis as SMS and SMMS composites achieve higher AAMI protection levels and as Tyvek sterilization wrap capacity additions support the surge in single-use medical devices. Industry reviews highlight a gap between gown barrier standards and real-world pathogen persistence, accelerating interest in validated antimicrobial polypropylene substrates. Collectively, these developments raise baseline consumption in the polypropylene non-woven fabric market.

Expanding Usage in Packaging Industry

Brand owners are shifting toward monomaterial structures to comply with Europe's 2030 recyclability targets, steering flexible packaging specifications toward high-purity, single-site polypropylene nonwovens. Borealis' 2026 scale-up of Borstar Nextension grades aims to supply this compliance-driven demand, offering improved sealing and mechanical recyclability for food contact and healthcare pouches. In logistics, breathable spunbond bags replace polyethylene films because they cut condensation damage during transport while maintaining printability for branding. Reuse and void-space caps embedded in the packaging regulation could depress some single-use volumes, yet they simultaneously create openings for durable nonwoven bag systems that satisfy reuse metrics. Near-term supply of food-grade recycled polypropylene remains tight, sustaining a premium that further differentiates virgin meltblown and spunbond rolls within the polypropylene non-woven fabric market.

Environmental and Regulatory Pressure on Single-Use Plastics

The EU Packaging and Packaging Waste Regulation, effective August 2026, obliges every pack format to meet at least grade C recyclability by 2030 and grade A or B by 2038, with recycled-content quotas escalating yearly. Extended producer responsibility fees penalize hard-to-recycle composites, directly affecting low-grammage commodity spunbond shopping bags and single-use tableware. A separate EU draft issued in September 2025 requires pellet-handling sites above 1,500 tons/year to certify risk-mitigation plans and exposes violators to fines up to 3% of Union turnover. North-American states are adopting analogous bag bans and recycled-content laws, tightening the policy vice. While industrial, automotive, and geotextile nonwovens remain largely untouched, converters serving consumer packaging segments must accelerate design-for-recycling initiatives to retain market access within the polypropylene non-woven fabric market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight, Cost-Effective Material Economics

- Increasing Utilization in Agriculture

- Polypropylene Price Volatility Linked to Crude Oil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spunbond retained 55% of the polypropylene non-woven fabric market share in 2025 owing to high-speed output and low unit costs that suit diapers, bags, and geotextiles. The polypropylene non-woven fabric market size for spunbond grades exceeded USD 21 billion in the base year, yet its forecast CAGR lags niche technologies as saturation sets in. Melt-blown, projected to grow 6.87% annually, benefits from regulatory upgrades to N95 respirators, HVAC, and battery-electrode separators that demand fibers below 3 µm diameter. Composite SMS and SMMS structures marry spunbond strength with melt-blown filtration, capturing hospital gown and industrial filtration spend. Investments in Reicofil 5 and equivalent lines across North America, Turkey, and China illustrate the capital pivot. Hybrid lines that alternate hot-air and calender bonding extend the basis-weight range to 10-200 g/m2, enabling automotive and roofing penetration.

Policy momentum compounds technical drivers. The US Department of Energy HVAC roadmap targets 50% energy reductions in commercial buildings by 2035, incentivizing high-efficiency melt-blown media; meanwhile, China's 2026 indoor-air-quality standard caps PM2.5 at 35 µg/m3, spurring cabin-air and residential filter demand. Supply tightness during 2020-2021 underscored the necessity of domestic melt-blown capacity, justifying government incentives in India, Indonesia, and Brazil. Equipment suppliers report order pipelines stretching into 2028, supporting a healthy backlog for the polypropylene non-woven fabric market.

Geography Analysis

Asia-Pacific controlled 42.67% of global demand in 2025 and is on track for a 6.91% CAGR through 2031 as China and India commission over 35 mt of integrated polypropylene capacity. Reliance's 5.20 million tonnes per annum Jamnagar plant, slated for 2030, alone can feed more than 10 billion m2 of spunbond fabric yearly, signaling an import-replacement strategy that elevates regional self-sufficiency. China's Fujian Eversun pipeline and Indonesia's Tuban complex likewise tighten the intra-Asia resin loop, reducing freight costs and carbon footprints. Converters take advantage, adding Reicofil and Oerlikon lines near end-markets to cut lead times and tailor basis-weight portfolios for local specifications.

North America's polypropylene non-woven fabric market benefits from OEM reshoring moves. Kimberly-Clark's USD 2 billion multi-state program and Avgol's Reicofil 5 installation in North Carolina enhance supply resilience and reduce overreliance on Asian imports. Ahlstrom's filter-media upgrade in Illinois, set for Q4 2026, will meet surging HVAC and EV filtration demand, underlining a structural pivot to domestic raw-material security. Resin price premiums remain a headwind, but domestic logistics savings and tariff avoidance partially offset higher feedstock costs.

Europe adds demand mainly through regulatory push for recyclable solutions. Borealis' 2026 Burghausen investment lines up with PPWR deadlines, offering grades that unlock monomaterial pouches and sterilizable medical wrap markets. Germany's polypropylene imports of 903 kt in 2024 illustrate dependence on intra-EU and Middle Eastern feedstock; CBAM adjustments could further redirect flows toward lower-carbon suppliers. South America and the Middle East & Africa remain emerging pockets, with Brazil's protected-cultivation subsidies and Turkey's twin 1 million tonnes per annum polypropylene projects expanding regional applicability of crop-protection and construction fabrics.

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corp.

- Avgol Nonwovens

- Dalian Ruiguang Nonwoven Group

- Don & Low Ltd.

- DuPont

- Fibertex Nonwovens A/S

- Fitesa S.A.

- Freudenberg Group

- Glatfelter Corp.

- Johns Manville

- Kimberly-Clark Worldwide, Inc.

- Kingsafe Group

- Lydall Performance Materials

- Magnera

- Mitsui Chemicals Inc.

- PFNonwovens Holding

- Sandler AG

- Schouw & Co. (Fibertex Personal Care)

- Shandong Kangjie Nonwovens

- Sunshine Nonwoven Fabric Co.

- Suominen Corp.

- Toray Advanced Materials Korea Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand in hygiene and medical disposables

- 4.2.2 Expanding usage in packaging industry

- 4.2.3 Lightweight, cost-effective material economics

- 4.2.4 Increasing utilization in agriculture

- 4.2.5 Antimicrobial PP nonwovens enabling reusable PPE

- 4.3 Market Restraints

- 4.3.1 Environmental and regulatory pressure on single-use plastics

- 4.3.2 Polypropylene price volatility linked to crude oil

- 4.3.3 EU carbon border adjustment raising import cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Technology

- 5.1.1 Spunbond

- 5.1.2 Meltblown

- 5.1.3 SMS (Spun-Melt-Spun)

- 5.1.4 SMMS (Spun-Melt-Melt-Spun)

- 5.1.5 Other Production Technologies

- 5.2 By Application

- 5.2.1 Hygiene

- 5.2.2 Medical

- 5.2.3 Packaging

- 5.2.4 Automotive

- 5.2.5 Filtration

- 5.2.6 Agriculture

- 5.2.7 Other Applications

- 5.3 By Raw Material Type

- 5.3.1 Homopolymer

- 5.3.2 Copolymer

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Ahlstrom

- 6.3.2 Amcor plc

- 6.3.3 Asahi Kasei Advance Corp.

- 6.3.4 Avgol Nonwovens

- 6.3.5 Dalian Ruiguang Nonwoven Group

- 6.3.6 Don & Low Ltd.

- 6.3.7 DuPont

- 6.3.8 Fibertex Nonwovens A/S

- 6.3.9 Fitesa S.A.

- 6.3.10 Freudenberg Group

- 6.3.11 Glatfelter Corp.

- 6.3.12 Johns Manville

- 6.3.13 Kimberly-Clark Worldwide, Inc.

- 6.3.14 Kingsafe Group

- 6.3.15 Lydall Performance Materials

- 6.3.16 Magnera

- 6.3.17 Mitsui Chemicals Inc.

- 6.3.18 PFNonwovens Holding

- 6.3.19 Sandler AG

- 6.3.20 Schouw & Co. (Fibertex Personal Care)

- 6.3.21 Shandong Kangjie Nonwovens

- 6.3.22 Sunshine Nonwoven Fabric Co.

- 6.3.23 Suominen Corp.

- 6.3.24 Toray Advanced Materials Korea Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment