PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062091

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062091

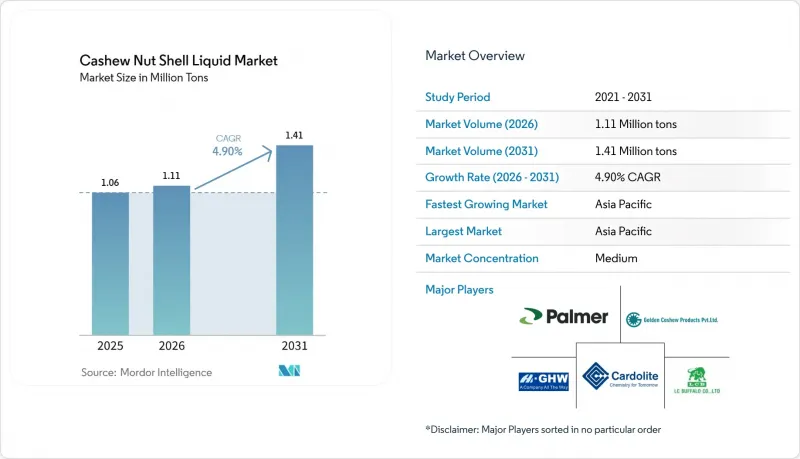

Cashew Nut Shell Liquid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cashew nut shell liquid market size was valued at 1.06 million tons in 2025 and is estimated to grow from 1.11 million tons in 2026 to reach 1.41 million tons by 2031, at a CAGR of 4.90% during the forecast period (2026-2031).

This report is Segmented by Product Type (Cardol and Others), Grade (Technical Grade and Others), Extraction Method (Mechanical Press and Others), Application (Friction Materials and Other Applications), End-User Industry(Oil and Gas and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Cashew Nut Shell Liquid Market Trends and Insights

Growing OEM Demand for High-Performance Friction Linings

Automotive and commercial vehicle manufacturers are replacing conventional phenol-formaldehyde with cardanol-based phenolic resins in brake pads to comply with stricter particulate emission and copper content regulations. This shift is driven by European Union (EU) Regulation 2019/631 and China's National VI standards. Additionally, electric vehicle platforms require friction materials capable of handling infrequent but high-energy braking events. In response to rising demand, Palmer International expanded its Texas production capacity in 2025, following reports of significant growth in orders for bio-based linings from North American truck original equipment manufacturers (OEMs). Peer-reviewed studies indicate that cashew nutshell liquid (CNSL)-phenolic composites offer improved wear resistance and reduced noise, vibration, and harshness, supporting their increased usage. Indian suppliers based in Chennai and Pune are utilizing domestic feedstock and International Organization for Standardization (ISO) 9001 certification to fulfill global contracts, further strengthening the Asia-Pacific region's position in this market.

Regulatory Push for Bio-Based, Low-VOC Industrial Coatings

The International Maritime Organization's Volatile Organic Compound (VOC) caps and national ecolabels support phenalkamine-cured epoxies due to their ability to cure efficiently at low temperatures and their high renewable-carbon content. Cardolite's LITE 514HP, introduced in May 2025, exceeds ASTM B117 salt-spray thresholds of 3,000 hours, making it suitable for applications such as offshore wind towers and marine hulls. Regulatory programs like the European Union Registration, Evaluation, Authorization, and Restriction of Chemicals (EU REACH) and the United States Environmental Protection Agency (U.S. EPA) Safer Choice discourage the use of nonylphenol ethoxylates, increasing demand for cardanol-based diluents despite their higher cost. European buyers consistently pay a 15-20% premium for distilled Cashew Nut Shell Liquid (CNSL) accompanied by traceability documentation, establishing a structural price floor for high-purity supply.

Volatile Cashew Crop Yields and Raw-Shell Pricing

Unpredictable monsoons and pest outbreaks have resulted in feedstock shortages, increasing shell prices, and reducing processor margins. In the first quarter (Q1) of 2026, India experienced a notable decline in raw-nut imports due to logistical challenges in West Africa. This situation led to smaller extractors halting operations and raised refined-grade prices to USD 975-1,025 per ton. West African countries continue to utilize most shells for energy, foregoing potential extraction revenue and contributing to global supply fluctuations. Integrated players with plantation connections secure long-term contracts, while spot buyers face margin pressures during periods of crop shortages.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Wind-Energy Blade Manufacturing Composites

- Shift to Phenalkamine Curing Agents in Marine Epoxy Systems

- Availability of Low-Cost Synthetic Alkyl-Phenols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical Cashew Nut Shell Liquid (CNSL) is expected to account for 46.5% of the volume in 2025, reflecting its cost efficiency in friction materials and generic industrial coatings. Cardanol is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.12%, driven by demand from epoxy and phenalkamine formulators requiring specifications such as Gardner color less than or equal to 1, potassium content below 10 parts per million (ppm), and a consistent amine value.

Distillation processes concentrate cardanol to 78% purity, enabling formulators to meet Original Equipment Manufacturer (OEM) requirements for electric vehicle brake systems and marine coatings that cure at sub-zero temperatures. Margin pressures caused by raw-shell price volatility are encouraging Indian and Vietnamese processors to expand wiped-film and ion-exchange purification lines to capture higher value from specialty derivatives. Additionally, phenalkamine resins remain a profitable sub-segment, with prices reaching up to USD 3,500 per ton for offshore coating applications.

Distilled and refined grades are projected to grow at a Compound Annual Growth Rate (CAGR) of 5.23% through 2031, driven by downstream demand for consistent chemical profiles and low trace metal content in high-end composites. In 2025, technical grade accounted for 42.1% of the Cashew Nut Shell Liquid market size; however, its market share is expected to decline as global Original Equipment Manufacturers (OEMs) standardize supplier quality audits.

European importers pay up to 20% more for Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH)-compliant refined materials, creating a price differential that supports technology upgrades in Asia-Pacific production facilities. Acid-grade output continues to cater to niche wood-adhesive applications, although many plywood manufacturers are transitioning to low-formaldehyde cardanol options, which offer improved performance compared to traditional phenol-formaldehyde binders.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 39.1% of the Cashew Nut Shell Liquid (CNSL) market and is projected to grow at a compound annual growth rate (CAGR) of 5.25% from 2026 to 2031. India processes approximately 45% of the global CNSL supply, benefiting from its proximity to cashew farms. Vietnam focuses on exporting refined CNSL grades, which are priced higher in European and North American markets. Meanwhile, China's resin producers are advancing research on cardanol-epoxy systems to localize supply chains and reduce import dependency. This is supported by multiple peer-reviewed studies in 2025 on graphene-reinforced cardanol matrices.

North America sources the majority of its CNSL feedstock from Asia but maintains strong demand for high-performance applications, such as friction binders and phenalkamine coatings. Palmer International's capacity expansion in 2025 reflects robust downstream orders, particularly from electric vehicle platforms that require bio-based materials. Additionally, Canada's wind energy sector is incorporating cardanol epoxies in blade repair resins, further expanding the market's addressable volume.

Europe remains the largest importer of refined and distilled CNSL grades, often paying traceability premiums to meet the requirements of Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) and Ecolabel certifications. Nordic countries are prioritizing recyclable epoxy systems for offshore wind projects, driving research and development efforts. These initiatives are supported by circular-economy grants that align with CNSL chemistry advancements.

South America, despite its abundance of raw cashew nuts, extracts limited volumes of CNSL. Brazilian researchers are pioneering new applications for CNSL, but industrialization in the region is hindered by capital shortages. The Middle East and Africa exhibit modest CNSL offtake. However, West Africa's surplus of raw cashew nuts presents an opportunity for localized extraction, which could enable the region to capture more value within the supply chain.

- Adarsh Industrial Chemicals

- Blueline Foods (India) Pvt Ltd

- C. Ramakrishna Padayatchi

- Cardolite Corporation

- Cashew Chem India

- Cat Loi Cashew Oil Production & Export JSC

- Elementis Plc

- GHW (VIETNAM) CO., LTD

- Golden Cashew Products Pvt. Ltd.

- K2P Chemicals

- Kumaraswamy Industries

- LC BUFFALO CO., LTD

- Muskaan Group

- Olam International

- Palmer International, Inc.

- Senesel

- Shivam Cashew Industry

- Shree Ganesh Agro

- SI Group

- Sri Devi Group

- Vavimex Co., Ltd

- Zhejiang Wansheng Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing OEM demand for high-performance friction linings

- 4.2.2 Regulatory push for bio-based, low-VOC industrial coatings

- 4.2.3 Expansion of wind-energy blade manufacturing composites

- 4.2.4 Shift to phenalkamine curing agents in marine epoxy systems

- 4.2.5 Rapid adoption of CNSL-based bio-pesticides in agro-chemicals*

- 4.3 Market Restraints

- 4.3.1 Volatile cashew crop yields and raw-shell pricing

- 4.3.2 Availability of low-cost synthetic alkyl-phenols

- 4.3.3 Scale-up challenges for super-critical CO2 extraction

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Technical CNSL (TCNSL)

- 5.1.2 Cardanol

- 5.1.3 Cardol

- 5.1.4 Phenalkamine Resins

- 5.1.5 Anacardic Acid and Other Derivatives

- 5.2 By Grade

- 5.2.1 Technical Grade

- 5.2.2 Acid Grade

- 5.2.3 Distilled / Refined Grade

- 5.3 By Extraction Method

- 5.3.1 Mechanical Press

- 5.3.2 Solvent Extraction

- 5.3.3 Distillation and Vacuum Distillation

- 5.3.4 Super-critical CO2 Extraction

- 5.3.5 Thermal Cracking

- 5.4 By Application

- 5.4.1 Friction Materials

- 5.4.2 Paints and Coatings

- 5.4.3 Adhesives and Laminates

- 5.4.4 Surfactants and Plasticizers

- 5.4.5 Polymer and Composites

- 5.4.6 Chemical Intermediates

- 5.4.7 Other Niche Uses (Bio-lubricants, Carbon Materials)

- 5.5 By End-User Industry

- 5.5.1 Automotive and Transportation

- 5.5.2 Building and Construction

- 5.5.3 Industrial Chemicals

- 5.5.4 Personal Care and Cosmetics

- 5.5.5 Oil and Gas

- 5.5.6 Agriculture

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 Japan

- 5.6.1.3 India

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Adarsh Industrial Chemicals

- 6.4.2 Blueline Foods (India) Pvt Ltd

- 6.4.3 C. Ramakrishna Padayatchi

- 6.4.4 Cardolite Corporation

- 6.4.5 Cashew Chem India

- 6.4.6 Cat Loi Cashew Oil Production & Export JSC

- 6.4.7 Elementis Plc

- 6.4.8 GHW (VIETNAM) CO., LTD

- 6.4.9 Golden Cashew Products Pvt. Ltd.

- 6.4.10 K2P Chemicals

- 6.4.11 Kumaraswamy Industries

- 6.4.12 LC BUFFALO CO., LTD

- 6.4.13 Muskaan Group

- 6.4.14 Olam International

- 6.4.15 Palmer International, Inc.

- 6.4.16 Senesel

- 6.4.17 Shivam Cashew Industry

- 6.4.18 Shree Ganesh Agro

- 6.4.19 SI Group

- 6.4.20 Sri Devi Group

- 6.4.21 Vavimex Co., Ltd

- 6.4.22 Zhejiang Wansheng Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Demand for Sustainable, Bio-based Solutions