PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062106

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062106

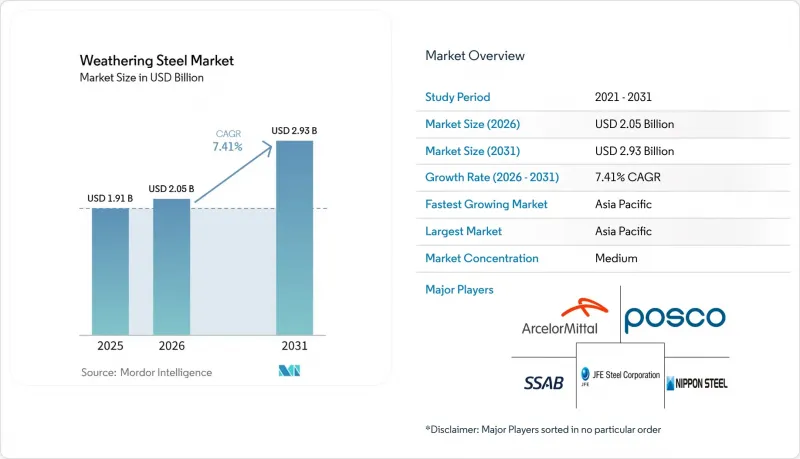

Weathering Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the weathering steel market size was valued at USD 1.91 billion in 2025 and is estimated to grow from USD 2.05 billion in 2026 to reach USD 2.93 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031).

This report is Segmented by Type (A588, A242, A606, ASTM A709 Gr50W, Others), Form (Plates, Sheets and Coils, and More), End-User Industry (Building and Construction, Bridges and Civil Infrastructure, Transportation, Industrial Plant and Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Weathering Steel Market Trends and Insights

Decarbonization Push Favoring Low-Maintenance Steels

Steelmakers are now embedding lifecycle-carbon accounting into their product offerings. This shift is particularly advantageous for weathering grades, as the removal of paint systems not only eliminates volatile organic compounds but also reduces emissions from recurring maintenance. ArcelorMittal's XCarb heavy plates, crafted in electric arc furnaces (EAFs) using over 75% scrap and powered entirely by renewable electricity, have achieved a 36% reduction in carbon intensity for Vestas' Nordlicht 1 offshore wind project when compared to traditional blast-furnace steel. Starting January 2026, the EU's Carbon Border Adjustment Mechanism will impose tariffs on imports with high carbon footprints. This move is nudging buyers towards certified low-carbon weathering grades. In a strategic move, Tata Steel is channeling USD 3.2 billion into its Kalinganagar expansion, introducing dedicated lines for high-strength weathering plates. This positions Tata to cater to both the domestic infrastructure boom and the export markets that align with CBAM standards. Currently, Europe and North America lead in demand, but as global carbon pricing tightens, a peak is anticipated in the medium term.

Aesthetic Weather-Tone Appeal in Urban Architecture

In 2025, design portal Dezeen spotlighted 10 signature projects, showcasing architects' growing admiration for the evolving rust-brown patina, valued for its unique texture and depth. Municipalities in Singapore and Toronto have updated their guidelines, detailing drainage solutions to prevent staining on nearby facades. This move has expedited approvals for the use of exposed weathering steel. Meanwhile, JFE Steel introduced its FLExB weld bead on the Miyuki Bridge in March 2026. This innovation promises smoother surfaces, significantly reducing runoff marks and addressing a primary concern in pedestrian areas. As flagship buildings emerge, setting material precedents, this architectural trend is expected to influence dense urban centers in the short term.

Patina Breakdown in Marine/High-Chloride Climates

In 2025, a study by Buildings journal highlighted premature section loss on bridges along the Gulf Coast. This finding led the DOTs of Louisiana, Oregon, and Washington to impose a ban on weathering steel within a 10-mile radius of saltwater. Similarly, while offshore wind foundations are turning to hot-dip galvanizing or epoxy coatings, the five U.S. Atlantic projects, collectively valued at over USD 28 billion and under construction in 2025, have steered clear of conventional weathering grades. Nippon Steel's CORSPACE hybrid plate, which was trialed on a bridge in Vanuatu in 2024, boasts extended repainting intervals. However, it finds itself in direct competition with traditional weathering plates for inland projects. Due to salt-spray limitations, growth in market share near coastal areas is expected to be restrained in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Lifecycle-Cost Edge Over Galvanized and Coated Steels

- Growing Use in Containerized Data-Center Skids

- Emerging Green-Steel Grades with Superior ESG

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, A588 captured 41.11% of the market share, highlighting its long-standing leadership in highway girders and transmission towers. Meanwhile, ASTM A709 Gr50W is on the rise, with a 7.88% CAGR, due to its preferred toughness and weldability among bridge engineers in seismic zones. Additionally, Ansteel's Q500qE plate, recognized for its 50% weight reduction, was pivotal in the 800 m Yichang Dongyan Yangtze span project, awarded in January 2026. As agencies increasingly prioritize performance-based specifications that emphasize seismic resilience, the market for A709-based bridge applications is expected to grow steadily.

While demand for the legacy A242 is declining due to inventory rationalization, new proprietary high-strength products like SSAB's Strenx Weathering 700 and 960, introduced in March 2025, are creating niches in mining and offshore equipment. Furthermore, the recently published ASTM A588-24 standard in October 2024, which tightens chemistry and impact-test protocols, is facilitating cross-market certifications. As a result, the weathering steel market is anticipated to see an increase in the share of premium plates, driven by these higher-grade substitutions.

Geography Analysis

Asia-Pacific, commanding 46.13% of 2025's revenue, is projected to grow at a rate of 8.02% through 2031. The region's dynamism is supported by China's ambitious bridge program, India's 8 metric tons per annum Kalinganagar expansion, and Japan's FLExB weld innovation. Additionally, ASEAN's highway corridors and South Korea's offshore wind yards contribute to the incremental tonnage.

Since June 2025, North America has reaped the benefits of 50% Section 232 tariffs, providing a shield for domestic mills. Gerdau, in response, boosted its 2025 shapes shipments by 8.5% to reach 2.59 metric tons and is on track to introduce an additional 150 kilotons of EAF capacity in Texas by late 2026. Meanwhile, U.S. grid operators invested a total of USD 115 billion into transmission in 2025, spurring a heightened demand for weathering piles and poles.

Europe is pivoting towards a low-carbon plate. For example, ArcelorMittal's XCarb deliveries to Vestas achieved a 36% reduction in tower emissions. Concurrently, ThyssenKrupp's USD 870 million revamp in Duisburg and Salzgitter's takeover of 6 metric tons HKM in June 2026 are reshaping the continent's capacity landscape. Furthermore, the enforcement of CBAM from 2026 is set to bolster domestic premiums for certified EAF weathering grades.

In South America, Gerdau has slashed its 2026 capex by 20% due to a surge in imports, as authorities struggled to curb subsidized inflows. Nevertheless, Brazil, Argentina, and Chile continue to prioritize weathering plates for their viaducts and solar farms. Meanwhile, the Middle East & Africa's demand is concentrated around Gulf bridges, desalination plants, and South African mining, with regional fabricators like Cleveland Bridge Steel stepping up to meet these needs.

- ArcelorMittal

- Bluescope Steel Limited

- China Ansteel Group Corporation Limited

- Dillinger Hutte

- Gerdau S/A

- HBIS Group

- JFE Steel Corporation

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Oklahoma Steel & Wire, Inc.

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal PJSC

- Shandong Baosteel Industry Co., Ltd

- SSAB AB

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Decarbonisation push favouring low-maintenance steels

- 4.2.2 Aesthetic weather-tone appeal in urban architecture

- 4.2.3 Lifecycle-cost edge over galvanised and coated steels

- 4.2.4 Growing use in containerised data-centre skids

- 4.2.5 Adoption in high-altitude solar tracker columns

- 4.3 Market Restraints

- 4.3.1 Patina breakdown in marine/high-chloride climates

- 4.3.2 Emerging "green-steel" grades with superior ESG

- 4.3.3 Designer push-back over perceived colour drift

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 A588

- 5.1.2 A242

- 5.1.3 A606

- 5.1.4 ASTM A709 Gr50W

- 5.1.5 Others

- 5.2 By Form

- 5.2.1 Plates

- 5.2.2 Sheets and Coils

- 5.2.3 Bars and Sections

- 5.2.4 Pipes and Tubes

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Bridges and Civil Infrastructure

- 5.3.3 Transportation (Railcar, Shipbuilding)

- 5.3.4 Industrial Plant and Machinery

- 5.3.5 Art, Sculpture and Public Furniture

- 5.3.6 Renewable Energy Structures

- 5.3.7 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 Bluescope Steel Limited

- 6.4.3 China Ansteel Group Corporation Limited

- 6.4.4 Dillinger Hutte

- 6.4.5 Gerdau S/A

- 6.4.6 HBIS Group

- 6.4.7 JFE Steel Corporation

- 6.4.8 LIBERTY Steel Group

- 6.4.9 NIPPON STEEL CORPORATION

- 6.4.10 Oklahoma Steel & Wire, Inc.

- 6.4.11 POSCO

- 6.4.12 Salzgitter Flachstahl GmbH

- 6.4.13 Severstal PJSC

- 6.4.14 Shandong Baosteel Industry Co., Ltd

- 6.4.15 SSAB AB

- 6.4.16 Tata Steel

- 6.4.17 Thyssenkrupp AG

- 6.4.18 United States Steel Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment