PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062123

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062123

Hair Removal Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

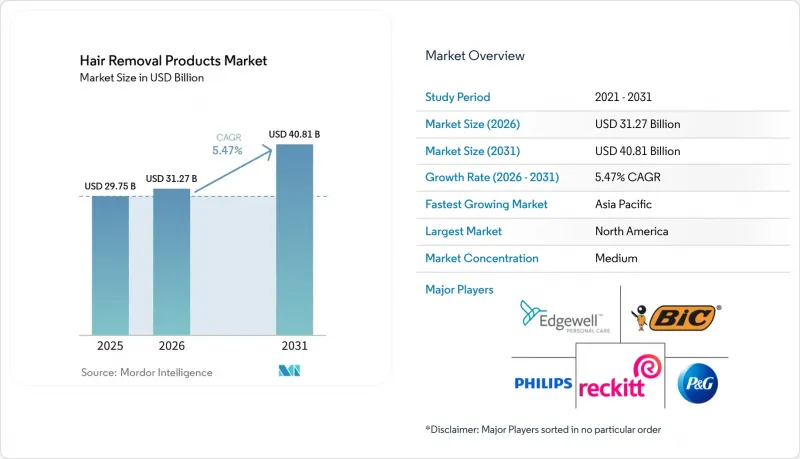

According to Mordor Intelligence, the hair removal products market size is expected to increase from USD 29.75 billion in 2025 to USD 31.27 billion in 2026 and reach USD 40.81 billion by 2031, growing at a CAGR of 5.47% over 2026-2031.

This report is Segmented by Product Type (Razors and Blades, Shaving Creams and Foams, Waxes, and More), End User (Household/Personal, Professional), Gender (Male, Female), Distribution Channel (Supermarkets/Hypermarkets, Health and Beauty Stores, Online Retail Stores, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Hair Removal Products Market Trends and Insights

Growing emphasis on personal grooming and hygiene

Consumer spending on personal grooming and hygiene continues to increase as maintenance routines become integral to daily life. Data from Poland's Central Statistical Office shows monthly spending on personal hygiene increased from PLN 47.86 in 2022 to PLN 53.6 in 2023, indicating growing consumer investment in self-care . Companies like Veet (Reckitt Benckiser), Nair (Church & Dwight), Philips, Sally Hansen, and The Man Company offer diverse hair removal solutions, including depilatory creams, waxes, IPL devices, and male grooming products. These companies continue developing products that are convenient, skin-safe, and technologically efficient for at-home use. Digital marketing, influencer partnerships, and e-commerce accessibility have normalized hair removal practices like shaving, waxing, and cream-based depilation as standard hygiene routines. Market players are expanding their consumer base through product innovations, awareness campaigns, and specialized offerings for demographics, including men and individuals with sensitive skin. This increased focus on personal grooming contributes to the growth of the global hair removal products market.

Demand for convenient at-home solutions

The demand for at-home hair removal solutions has increased due to privacy concerns, cost-efficiency, and technological improvements that provide results comparable to professional treatments. The FDA's implementation of Class II special controls for low-level laser systems validates the safety and effectiveness of these home-use devices, increasing consumer trust . At-home treatments offer time savings, flexible scheduling options, eliminate appointment requirements, and reduce potential exposure to communicable diseases. Current IPL devices achieve up to 90% hair reduction within a month and include app-based guidance for personalized treatment, making professional-level results possible at home. This technology particularly appeals to younger consumers who prefer self-administered treatments and integrated digital solutions. Companies like Philips, TRIA Beauty, and MiSMON dominate the market with devices featuring skin sensors and adjustable settings for various hair and skin types. The expansion of online retail channels increases product accessibility, addressing consumer needs for privacy, convenience, and effective hair removal solutions. These factors contribute to market growth, reflecting increased demand for self-care solutions and hygienic personal grooming options.

Concerns over skin irritation, allergies, and side effects from chemical or mechanical methods

Safety concerns regarding skin irritation, allergies, and side effects impact hair removal product sales and market performance, particularly as consumer awareness increases and regulatory oversight intensifies. The Australian Radiation Protection and Nuclear Safety Agency has documented severe adverse effects from laser and IPL devices, including burns and eye injuries, emphasizing the importance of professional expertise and safety protocols . Chemical depilatories face regulatory challenges due to ingredient safety reviews, particularly concerning potential allergens and carcinogens, necessitating product reformulations or restrictions. While the International Commission on Non-Ionizing Radiation Protection advocates for standardized global safety regulations, varying country-specific standards create compliance challenges for manufacturers and consumers. The UK's 2024 recall of non-compliant IPL products demonstrates how safety issues can damage consumer confidence and trigger regulatory actions. Market expansion faces limitations among sensitive demographics, including individuals with darker skin tones, pregnant women, and those with dermatological conditions. Companies are developing safer, clinically tested formulations and devices, while implementing consumer education programs to reduce risks. The hair removal market's continued growth depends on maintaining a balance between innovation and safety standards to ensure consumer protection.

Other drivers and restraints analyzed in the detailed report include:

- Rising influence of social media and beauty influencers

- Increasing marketing and education by brands

- Chemical-safety scrutiny on depilatories

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Razors and blades hold the dominant market share at 39.56% in 2025, while electronic devices show the highest growth rate at 5.90% CAGR through 2031, as consumers increasingly adopt advanced grooming technology. The wet shaving segment continues to evolve through product development, exemplified by Procter & Gamble's Gillette Venus introducing enhanced formulations with skin care benefits in March 2025. Besides, shaving creams and foams remain complementary to razor sales but face competition from waterless options and multi-purpose products. Also, wax products sustain consistent demand across hot, cold, and strip variants, especially in professional salons where immediate results outweigh discomfort considerations.

Hair removal devices maintain premium price points through technological advancements, including AI integration and app connectivity that enhance effectiveness and user experience. While depilatory creams remain widely used due to convenience, regulatory oversight regarding chemical safety, specifically concerning allergens and carcinogens, limits their market growth. The development of AI-enabled devices has established electronic products as the main growth segment in the hair removal market, attracting consumers who seek professional-level results at home. Companies such as Philips, RaysDanc, and Braun demonstrate this trend by developing devices with customizable settings, skin sensors, and pain reduction features. These technological capabilities increase user confidence, support higher pricing, and drive market adoption, establishing electronic devices as key drivers of market expansion.

The household/personal user segment accounts for 71.94% of hair removal product sales in 2025, as consumers increasingly choose accessible options like depilatory creams, wax strips, and home-use electronic devices. The professional segment, comprising salons and clinics, is expected to grow at a CAGR of 7.38% through 2031. This expansion stems from investments in advanced equipment that combines hair removal with additional treatments like skin rejuvenation, optimizing equipment usage, and per-client revenue. Consumer preference for professional services remains strong, particularly for treatments requiring specialized expertise in sensitive areas, with customers willing to pay higher prices for reliable results.

The professional segment's growth stems from institutional investments in advanced technologies, which often lead to innovations that later enter the consumer market. Companies like Philips have positioned IPL technology for home use by emphasizing its development by dermatologists, creating similarities between professional and personal-use devices. However, the professional segment maintains high barriers to entry through training requirements and regulatory compliance, which protect established providers and maintain safety standards. Professional providers distinguish themselves through specialized treatments and personalized consultations, preserving their premium service positioning despite home-use device advancements. This positioning helps maintain the professional segment's significant role in the global hair removal market.

Geography Analysis

North America holds 32.48% market share in the hair removal products market in 2025, supported by high market penetration and consumer preference for premium grooming products. The region's strength stems from established grooming practices, structured regulatory environments, and consumer adoption of advanced electronic hair removal devices from manufacturers like Philips and Reckitt Benckiser. The extensive retail network, including supermarket chains and specialty stores, ensures broad product accessibility. The market benefits from integration between the United States, Canada, and Mexico through trade relationships and shared consumer preferences, solidifying North America's market leadership.

Asia-Pacific demonstrates the highest growth rate at 6.13% CAGR through 2031. This growth stems from increasing urbanization, higher female workforce participation, and the growing influence of Western beauty trends. Japan, the fourth-largest cosmetics market globally, and South Korea maintain product quality through regulatory bodies PMDA and KFDA. China's Cosmetics Supervision and Administration Regulation has improved product approval processes, as evidenced by Beiersdorf's Thiamidol approval in 2024. The region's large young population with increasing beauty awareness drives demand for modern hair removal solutions.

Europe maintains consistent market growth through unified regulations across countries, building consumer confidence in product safety. Germany, the United Kingdom, France, and Spain show strong demand for premium and environmentally conscious products. Besides, South America, and Middle East and Africa offer growth potential through increasing grooming awareness and social media influence, despite current market limitations. Companies like Sally Hansen and Emjoi are expanding their presence in these regions as market accessibility improves, indicating future growth opportunities in the global hair removal market.

- Koninklijke Philips N.V.

- Spectrum Brands Holdings, Inc.

- Edgewell Personal Care Company

- Panasonic Corporation

- The Procter & Gamble Company

- Coty Inc (Sally Hansen)

- Reckitt Benckiser Group PLC

- Conair Corporation

- Wahl Clipper Corporation

- Church & Dwight Co., Inc.(Nair)

- Beiersdorf AG

- Societe Bic S.A.

- Sue Ismiel & Daughters Enterprises (Nad's)

- Dollar Shave Club

- Mammoth Brands

- The Organic Ones

- Redroom Technology Pvt. Ltd (Sanfe)

- Completely Bare

- Mountainor Well Being Pvt Ltd.

- Oyo Skincare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing emphasis on personal grooming and hygiene

- 4.2.2 Demand for convenient at-home solutions

- 4.2.3 Rising influence of social media and beauty influencers

- 4.2.4 Increasing marketing and education by brands

- 4.2.5 Technological advances in laser and IPL devices

- 4.2.6 Expansion of product variety to suit different skin types and preferences

- 4.3 Market Restraints

- 4.3.1 Concerns over skin irritation, allergies, and side effects from chemical or mechanical methods

- 4.3.2 Chemical-safety scrutiny on depilatories

- 4.3.3 Lack of awareness or education regarding proper use for effective results

- 4.3.4 Growing social acceptance of body hair

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Razors and Blades

- 5.1.2 Shaving Creams and Foams

- 5.1.3 Waxes (Hot, Cold, Strips)

- 5.1.4 Depilatory Creams and Lotions

- 5.1.5 Electronic Devices

- 5.2 By End User

- 5.2.1 Household/Personal

- 5.2.2 Professional

- 5.3 By Gender

- 5.3.1 Male

- 5.3.2 Female

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Health and Beauty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Koninklijke Philips N.V.

- 6.4.2 Spectrum Brands Holdings, Inc.

- 6.4.3 Edgewell Personal Care Company

- 6.4.4 Panasonic Corporation

- 6.4.5 The Procter & Gamble Company

- 6.4.6 Coty Inc (Sally Hansen)

- 6.4.7 Reckitt Benckiser Group PLC

- 6.4.8 Conair Corporation

- 6.4.9 Wahl Clipper Corporation

- 6.4.10 Church & Dwight Co., Inc.(Nair)

- 6.4.11 Beiersdorf AG

- 6.4.12 Societe Bic S.A.

- 6.4.13 Sue Ismiel & Daughters Enterprises (Nad's)

- 6.4.14 Dollar Shave Club

- 6.4.15 Mammoth Brands

- 6.4.16 The Organic Ones

- 6.4.17 Redroom Technology Pvt. Ltd (Sanfe)

- 6.4.18 Completely Bare

- 6.4.19 Mountainor Well Being Pvt Ltd.

- 6.4.20 Oyo Skincare

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK