PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062137

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062137

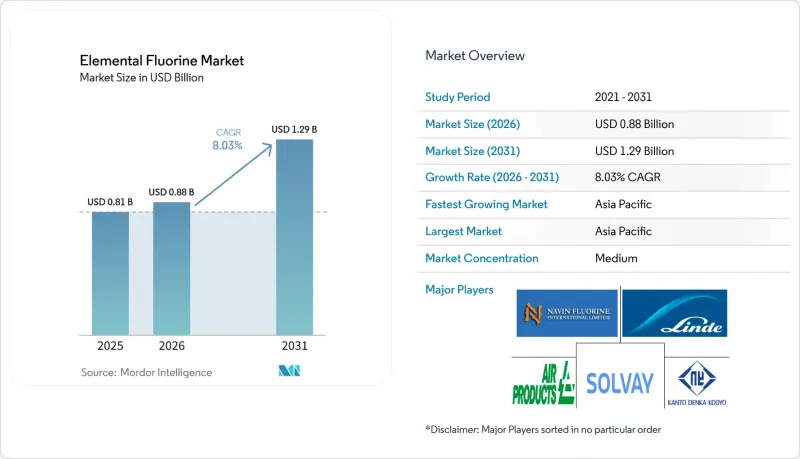

Elemental Fluorine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the elemental fluorine market size is projected to be USD 0.81 billion in 2025, USD 0.88 billion in 2026, and reach USD 1.29 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031.

This report is Segmented by Type (a-Fluorine and B-Fluorine), Application (Electronics and Semiconductors, Energy and Nuclear, Sulfur Hexafluoride, Chemical Processing, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Elemental Fluorine Market Trends and Insights

Expansion of UF6 Conversion/Enrichment Capacity for Nuclear Fuel

Government-supported enrichment projects are increasing fluorine consumption as advanced reactors transition from pilot phases to early commercial deployment. Centrus Energy's Piketon, Ohio site is expanding with thousands of centrifuges under a multi-year engineering contract awarded in 2026, positioning the facility as the West's only licensed source of high-assay LEU fuel. Each kilogram of LEU requires elemental fluorine during the UF4-to-UF6 conversion process, directly linking nuclear capacity to fluorine demand. Similar capacity expansions in France and India are further strengthening mid-term demand visibility. Suppliers offering nuclear-qualified purity grades are securing decade-long offtake agreements, which support investments in new electrolyzers.

Growth in Plastics, LCD and OLED Display Etching/Cleaning Uses

OLED penetration accounted for 61% of LG Display's revenue in 2025, with the company investing USD 970 million to expand panel production lines through 2027. Advanced display technologies require multiple dry-etch processes, where fluorinated gases remove polymeric residues without damaging underlying layers. Semiconductor fabs operating below the 5 nm node are adopting elemental fluorine for chamber cleaning due to its zero-GWP properties, which help meet Scope 1 emissions targets. These trends are particularly concentrated in the Asia-Pacific region, where over 80% of new display and semiconductor capacity is under construction, representing the largest near-term growth driver for the elemental fluorine market.

High Capex/Opex for Fluorine Electrolysis Production Plants

Electrolyzer cells require specialized materials such as nickel-copper alloys, double-walled piping, and continuous gas monitoring systems, driving installed costs above USD 10 million for large facilities. In Europe, high electricity tariffs further increase variable costs compared to Asian plants, limiting domestic expansion and encouraging the tolling of semi-finished intermediates back to Asia.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Phase-Down of High-GWP NF3 Favoring F2 Adoption

- On-Site Modular Fluorine Generators Reducing Logistics Risk

- Limited Global Supply of Battery-Grade Anhydrous HF Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

a-Fluorine accounted for 70.78% of the elemental fluorine market share in 2025, supported by long-established infrastructure used for nuclear fuel conversion and semiconductor chamber cleaning. This segment benefits from a stable customer base, proven passivation protocols, and readily available analytical standards.

B-Fluorine is projected to grow at a CAGR of 8.24% through 2031, albeit from a smaller base. Its unique reactivity for selective fluorination is increasingly valued by battery and pharmaceutical innovators. As production scales up, B-Fluorine's contribution to the elemental fluorine market size is expected to increase, though a-Fluorine is likely to retain its dominance through the forecast period.

Geography Analysis

Asia-Pacific controlled 54.45% of global revenue in 2025 thanks to the clustering of display, semiconductor, and EV supply chains. Chinese producers such as Dongyue are redirecting HK$191.9 million into high-purity PTFE for chip fabs and pilot tetrafluoropropylene lines that enable low-GWP refrigerants South Korean OLED expansions and Japanese fine-gas investments further strengthen the region's position, keeping Asia-Pacific on an 8.95% CAGR trajectory through 2031.

North America is regaining strategic weight as the CHIPS Act subsidizes fabs in Arizona and Texas, while the Inflation Reduction Act anchors battery-material projects in the Southeast. Centrus Energy's Piketon HALEU project alone creates a multiyear fluorine feed for nuclear fuel blending. Domestic fluorspar scarcity persists, so most anhydrous HF feedstock still ships from Mexico and China, nudging producers toward co-located HF plants on the Gulf Coast.

Europe faces the twin pressures of elevated electricity pricing and stringent F-gas quotas. Industrial-gas majors prefer brownfield expansions in Germany and Ireland, but many refrigerant and PVDF expansions are moving to Kentucky or Jiangsu to cap opex exposure. High anhydrous HF import costs place Europe at a structural disadvantage, keeping its Elemental fluorine market growth below the global mean despite regulatory incentives for low-GWP chemistries.

- Air Liquide

- Air Products and Chemicals, Inc.

- Arkema

- Central Glass Co., Ltd.

- DAIKIN INDUSTRIES, Ltd.

- Deepak Nitrite Limited

- DONGYUE GROUP

- F2 Chemicals Ltd.

- Inhance Technologies

- KANTO DENKA KOGYO CO., LTD.

- Linde PLC

- Messer SE & Co. KGaA

- Navin Fluorine International Limited

- Pelchem SOC Ltd.

- Resonac

- Solvay

- The Chemours Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of UF6 conversion/enrichment capacity for nuclear fuel

- 4.2.2 Growth in plastics, LCD and OLED display etching/cleaning uses

- 4.2.3 Regulatory phase-down of high-GWP NF3 favouring F2 adoption

- 4.2.4 On-site modular fluorine generators reducing logistics risk

- 4.2.5 Emerging use of high-purity F2 as lithium-ion battery electrolyte additive

- 4.3 Market Restraints

- 4.3.1 High capex/opex for fluorine electrolysis production plants

- 4.3.2 Limited global supply of battery-grade anhydrous HF feedstock

- 4.3.3 Shortage of certified fluorine-handling technicians

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 a- Fluorine

- 5.1.2 B- Fluorine

- 5.2 By Application

- 5.2.1 Electronics and Semiconductors

- 5.2.2 Energy and Nuclear

- 5.2.3 Sulfur Hexafluoride

- 5.2.4 Chemical Processing

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals, Inc.

- 6.4.3 Arkema

- 6.4.4 Central Glass Co., Ltd.

- 6.4.5 DAIKIN INDUSTRIES, Ltd.

- 6.4.6 Deepak Nitrite Limited

- 6.4.7 DONGYUE GROUP

- 6.4.8 F2 Chemicals Ltd.

- 6.4.9 Inhance Technologies

- 6.4.10 KANTO DENKA KOGYO CO., LTD.

- 6.4.11 Linde PLC

- 6.4.12 Messer SE & Co. KGaA

- 6.4.13 Navin Fluorine International Limited

- 6.4.14 Pelchem SOC Ltd.

- 6.4.15 Resonac

- 6.4.16 Solvay

- 6.4.17 The Chemours Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment