PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062143

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062143

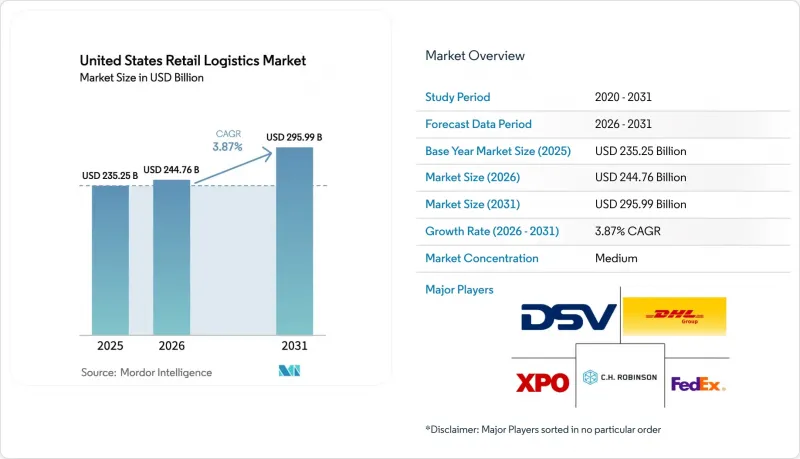

United States Retail Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states retail logistics market size was valued at USD 235.25 billion in 2025 and is estimated to grow from USD 244.76 billion in 2026 to reach USD 295.99 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031).

Retailers have begun converting stores into fulfillment nodes, temperature-controlled networks are expanding to serve complex biologics pipelines, and federal green-corridor programs are accelerating the shift toward electric line-haul fleets. This report is Segmented by Service Type (Transportation, Warehousing & Distribution, and More), by Temperature-Control (Ambient, Chilled, Frozen, Non Cold Chain), by Product Type (Food and Beverages, Apparel and Footwear, Electronic Appliances, Healthcare & Pharmaceuticals, and More), and by Region (Northeast, Southeast, Southwest). The Market Forecasts are Provided in Terms of Value (USD).

United States Retail Logistics Market Trends and Insights

Omnichannel BOPIS (Buy-Online-Pick-Up-In-Store) Expansion

Buy-online-pick-up-in-store (BOPIS) continues to reshape suburban retail logistics by blending digital convenience with physical store networks. Retailers are increasingly redesigning store footprints to accommodate dedicated pickup zones, curbside lanes, and micro-fulfillment backrooms that enable rapid order staging. This model reduces last-mile delivery costs while increasing store traffic, as customers frequently make incremental purchases during pickup visits. The competitive pressure is intensifying as large chains invest in real-time inventory visibility and seamless app-based ordering, raising customer expectations for speed and reliability capabilities that smaller retailers often struggle to match. As suburban populations grow and e-commerce penetration deepens, BOPIS is becoming a default fulfillment option rather than a value-added service.

Biologics-Led Ultra-Cold Demand

The rapid growth of biologic drugs, cell and gene therapies, and mRNA-based treatments is driving demand for specialized ultra-cold storage and distribution infrastructure. These therapies often require strict temperature ranges, sometimes as low as -70°C, creating a need for advanced cold chain logistics, redundant power systems, and highly monitored transportation networks. Innovation clusters such as Boston, San Francisco, and Research Triangle Park (RTP) are seeing increased investment in temperature-controlled warehousing and last-mile delivery solutions tailored to healthcare providers and research institutions. The complexity of handling sensitive biologics is also pushing logistics providers to adopt real-time tracking, predictive risk management, and compliance-focused operations, elevating the overall sophistication and cost structure of pharmaceutical supply chains.

Industrial Real Estate Vacancy Lows

Persistently low vacancy rates across major logistics hubs such as the Inland Empire, Dallas-Fort Worth, Chicago, and Northern New Jersey are constraining supply chain expansion. With available warehouse space at historic lows, tenants face rising lease rates, limited location choice, and longer lead times for securing capacity. This imbalance is particularly acute for modern, high-clearance facilities suited for e-commerce and automation, which remain in short supply. As a result, occupiers are forced into suboptimal locations or older assets, increasing transportation inefficiencies and operating costs. In the short term, these constraints limit network scalability and delay expansion plans, especially for fast-growing retailers and third-party logistics providers.

Other drivers and restraints analyzed in the detailed report include:

- Near-shoring & "Made in USA" Incentives

- Real-Time Freight Visibility Platforms

- Rising Cargo Theft & Insurance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services generated 60.26% of the 2025 United States retail logistics market share. Value-added offerings, kitting, reverse logistics, and labeling are increasing at 6.66% CAGR, reflecting retailers' shift toward differentiated fulfillment. Integrated partnerships now bundle transportation, warehousing, and customization, reducing hand-offs and improving visibility.

Warehouse operators embed light-manufacturing stations, returns centers, and package-level personalization inside distribution hubs. Brands pay premiums for these capabilities because customer experience metrics such as delivery accuracy and returns turnaround directly drive loyalty. This shift is transforming warehouses from cost centers into value-generating nodes within the supply chain. As a result, operators who can integrate speed, customization, and data visibility are gaining a competitive edge in both B2B and direct-to-consumer markets.

List of Companies Covered in this Report:

- UPS

- FedEx

- DHL Group

- C.H. Robinson

- XPO Inc.

- GXO Logistics

- Ryder System

- J.B. Hunt

- Schneider National

- Lineage Logistics

- Americold

- Penske Logistics

- Kuehne+Nagel

- DSV

- GEODIS

- NFI Industries

- Xpress Global Systems (XGS)

- Kenco Logistics

- Marten Transport

- CMA CGM Group (CEVA Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel "Buy-Online-Pick-Up" (BOPIS) Network Expansion

- 4.2.2 Biologics-Led Surge in Temperature-Controlled Pharma Shipments

- 4.2.3 Near-Shoring and Federal "Made In USA" Incentives Boosting Domestic Inventory Nodes

- 4.2.4 Widespread Roll-Out of Real-Time Freight-Visibility Platforms

- 4.2.5 Retail Subscription/Loyalty Programs Driving Scheduled Delivery Volumes

- 4.2.6 Federal Funding for Zero-Emission Truck Corridors (IIJA Grants)

- 4.3 Market Restraints

- 4.3.1 Record-Low Industrial Real-Estate Vacancy in Core Metros

- 4.3.2 Escalating Cargo-Theft and Insurance Premiums

- 4.3.3 Cyber-Security Vulnerabilities in Cloud Logistics Stacks

- 4.3.4 Persistent Chassis Shortages at Rail and Port Intermodal Hubs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Rail

- 5.1.1.4 Sea

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services and Others (Kitting, Packaging, Labeling)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Requirement

- 5.2.1 Cold Chian

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chian

- 5.3 By Product Type

- 5.3.1 Food and Beverages

- 5.3.2 Apparel and Footwear

- 5.3.3 Electronic Appliances

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Furniture and Home Furnishings

- 5.3.6 Others

- 5.4 By Region (United States)

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 Southeast

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 UPS

- 6.4.2 FedEx

- 6.4.3 DHL Group

- 6.4.4 C.H. Robinson

- 6.4.5 XPO Inc.

- 6.4.6 GXO Logistics

- 6.4.7 Ryder System

- 6.4.8 J.B. Hunt

- 6.4.9 Schneider National

- 6.4.10 Lineage Logistics

- 6.4.11 Americold

- 6.4.12 Penske Logistics

- 6.4.13 Kuehne+Nagel

- 6.4.14 DSV

- 6.4.15 GEODIS

- 6.4.16 NFI Industries

- 6.4.17 Xpress Global Systems (XGS)

- 6.4.18 Kenco Logistics

- 6.4.19 Marten Transport

- 6.4.20 CMA CGM Group (CEVA Logistics)

7 Market Opportunities and Future Outlook