PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062209

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062209

Commercial Ice Cream Freezers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

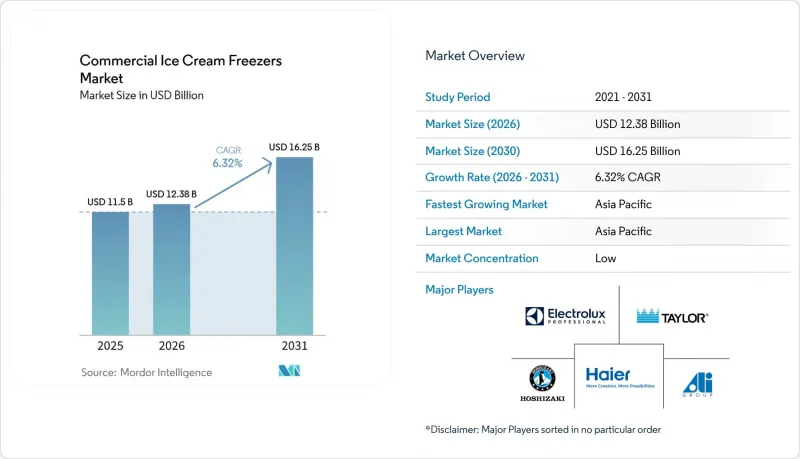

According to Mordor Intelligence, the commercial ice cream freezers market size is projected to be USD 11.5 billion in 2025, USD 12.38 billion in 2026, and reach USD 16.25 billion by 2031, growing at a CAGR of 6.32% from 2026 to 2031.

This report is Segmented by Product Type (Chest / Deep Freezers, and More), Cooling Technology (Static Cooling, and More), Capacity (Less Than Equal To 300 L, and More), End User (Ice-Cream Parlors & Gelaterias, and More), Sales Channel (Direct OEM, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Ice Cream Freezers Market Trends and Insights

Expansion of Quick-Service Restaurant Chains in Emerging Markets

QSR franchises are scaling up their frozen-dessert infrastructure across Asia-Pacific, the Middle East, and Latin America, significantly boosting the demand for commercial ice cream freezers. In February 2026, McDonald's Malaysia announced a major RM 1 billion (USD 255 million) investment. Out of this, RM 600 million is allocated for new restaurants, with plans to establish 45 to 75 franchised outlets over the next 5 to 10 years. Each outlet will require an investment of RM 5 million to RM 7 million, including refrigeration equipment. Similarly, Dairy Queen is focusing on expanding in the Middle East, particularly in the UAE and Saudi Arabia. With QSR markets in these regions expected to grow at a strong 14% CAGR and 85% of Saudi Arabia's fast-food consumers under 45, Dairy Queen's soft-serve and Blizzard offerings align well with market demand, as noted by FFCC Global. Central Retail is also pursuing growth in Vietnam, planning to open over 30 large-format stores between 2026 and 2028. This includes 10 to 12 Go! malls and hypermarkets, along with 23 to 25 mini Go! stores. Each store will require multiple freezer cabinets for impulse and take-home ice cream. These expansions are driving a steady yet uneven demand for freezers, as franchisees standardize equipment across chains to maintain product consistency and meet franchisor requirements.

Growth in Impulse Ice-Cream Retail at Convenience and Fuel Stops

Convenience stores and fuel stations are repositioning ice cream from seasonal add-ons to year-round traffic drivers, necessitating dedicated freezer cabinets with branded merchandising and flexible placement. Australia's petrol and convenience channel generated AUD 213 million in ice cream sales in 2024, up 3.1% year-over-year, with single-serve formats dominating and branded counter freezers delivering impulse uplift of up to 35% according to Mini Melts. Mini Melts expanded from 14 to over 950 Australian convenience stores within six months by offering 70g and 72g pouches in multipurpose freezers compatible with existing footprints, demonstrating how product-format innovation can rapidly scale distribution. Operators are rationalizing freezer space to favor high-velocity SKUs and premium trends such as pistachio, Biscoff, and matcha, while cross-category bundling with fuel, drinks, and snacks is boosting basket size. The shift toward health-conscious and inclusive offerings, including high-protein, reduced-calorie, gluten-free, dairy-free, and vegan options, is prompting retailers to install glass-top display freezers that showcase product variety and nutritional credentials at the point of sale.

High Upfront Procurement and Installation Costs

Capital intensity remains a formidable barrier for small operators and franchisees entering the commercial ice cream freezer market. Walk-in coolers and freezers range from USD 4,000 for small 6x6 units to over USD 35,000 for large 12x16 installations, with freezers commanding 20% to 40% premiums over coolers due to thicker insulation and more powerful refrigeration systems. Installation labor adds USD 2,000 to USD 7,000, electrical upgrades cost USD 200 to USD 500, and permits run USD 200 to USD 500, pushing total project costs 20% to 40% higher than equipment sticker prices. Reach-in freezers span USD 1,200 for entry-level economy units with 3 to 5 year lifespans to USD 10,000 for premium spec-line models with 15 to 20 year lifespans, with hidden costs including freight (USD 75 to USD 300), uncrating fees, and casters or shelves at USD 50 to USD 100 each. Energy costs dominate the total cost of ownership, with economy units consuming 12 kWh per day versus Energy Star models at 6 kWh per day, yielding USD 525 versus USD 262 annually at USD 0.12 per kWh and USD 2,630 in savings over 10 years.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Accelerating Equipment Replacements

- Rising Frozen-Dessert Consumption in Asia-Pacific

- Stringent Refrigerant Phase-Out Rules for HFC, HFO, and F-Gas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, chest and deep freezers accounted for 34.58% of product-type revenue, emphasizing their role in bulk storage for supermarkets, hypermarkets, and cold-storage warehouses. Gelato and soft-serve batch freezers are projected to grow at a 7.82% CAGR through 2031, driven by artisanal producers and QSRs adopting high-efficiency systems. Carpigiani's Labotronic HE-H batch freezer cuts electricity and water usage by 30% using Hard-O-Dynamic Adaptive technology. Nemox's Gelato 10K i-Green batch freezer, with R290 refrigerant (GWP 3), reduces CO2-equivalent emissions by 99.95% and produces 10 kg per hour in 12 to 15 minutes per cycle. Upright and glass-top freezers enhance product visibility, with glass-top units boosting convenience store sales by up to 35%.

Gelato batch freezers are gaining popularity in China and India, where consumers pay premiums for handcrafted products with natural ingredients and unique flavors. Cattabriga's Multifreeze Icona Hybrid batch freezer reduces water usage by 80% and electricity and water consumption by 30% using a patented dual-condensation system. Gram Equipment's Ice Technology Center in Denmark, operational since 2021, offers cost-effective pilot testing for new ice cream products, reducing testing costs by 70% to 80%. Chest freezers remain cost-effective for bulk storage but lack the merchandising appeal of upright and glass-top units. Batch freezers now incorporate Crystal programs for monoportions and frozen cakes, diversifying revenue streams.

In 2025, static cooling technology held a 45.62% market share due to lower upfront costs and easy installation. Remote glycol-cooled systems are projected to grow at an 8.11% CAGR through 2031, driven by large-format retailers and cold-storage operators seeking centralized refrigeration to reduce refrigerant charges, comply with EPA mandates, and lower energy use. Remote condensing units, while offering larger capacities and higher efficiencies, increase upfront costs by 20% to 40% due to additional installation requirements. Hussmann's Protocol CO2 rack supports California Title 24 compliance with modular architecture and iron/copper piping, while frost-free systems reduce maintenance labor. Liebherr's NoFrost technology targets foodservice and hospitality, offering Climate Class 5 reliability and energy ratings of C or above.

Remote glycol-cooled systems appeal to supermarkets and hypermarkets by reducing refrigerant charges below EPA thresholds and simplifying leak monitoring. Hussmann's Krack MicroDS and MicroSC Monoblock, launched in October 2023, integrate a pre-charged R290 condensing unit and evaporator, cutting refrigerant charges by up to 95% versus HFC systems and reducing annual CO2 emissions by 6%. Static cooling dominates small-format and budget-conscious installations due to simplicity and low costs, while frost-free systems gain traction in ice cream parlors by eliminating manual defrosting. Remote glycol-cooled systems are expected to grow in large-format installations and remodels, while static cooling remains prevalent in price-sensitive markets.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.92% of the market value and is expected to grow at a strong 7.68% CAGR through 2031. This growth is primarily driven by increasing per-capita consumption, the expansion of quick-service restaurants (QSRs), the growth of e-commerce cold chains, and urbanization in China, India, and Southeast Asia. India's organized ice cream sector, valued at Rs 30,000 crore (USD 3.5 billion) in 2023, is projected to reach Rs 50,000 crore (USD 5.83 billion) by 2028. Per-capita consumption has risen from 400 ml in 2011 to 1.6 liters in 2023. However, this remains significantly lower than New Zealand's 28.4 liters and the United States' 20.8 liters, highlighting substantial growth potential. China's ice cream market, valued at USD 20.57 billion in 2025, is forecast to grow to USD 35.44 billion by 2034, reflecting a 6.23% CAGR. This growth is fueled by millennial and Gen Z preferences for unique flavors such as matcha, red bean, taro, lychee, and mango. Artisanal shops and specialty boutiques are rapidly expanding in key cities like Beijing, Shanghai, Guangdong, and Jiangsu.

In India, quick-commerce platforms like Zepto, Swiggy Instamart, and Blinkit, along with e-commerce leaders in China, are driving frozen-food delivery growth. This trend necessitates increased freezer capacities at dark stores and micro-fulfillment centers. Central Retail is making significant investments in Vietnam, planning to open over 30 large-format stores between 2026 and 2028, including 10 to 12 Go! malls and hypermarkets, as well as 23 to 25 mini Go! stores. Hoshizaki Corporation has demonstrated its commitment to the region by acquiring additional shares in its Vietnamese subsidiary in March 2026 and expanding its natural-refrigerant lineup in November 2025. North America and Europe remain key markets. Regulatory mandates aimed at reducing high-GWP refrigerants and improving energy efficiency are driving equipment replacement cycles. Effective January 1, 2026, the U.S. EPA lowered the refrigerant charge threshold from 50 lb to 15 lb. Additionally, the AIM Act Technology Transition Rule prohibits the installation of new systems using high-GWP refrigerants after January 1, 2026. These regulations are accelerating the phase-out of legacy HFC-based units. Epta strengthened its industrial and geographic presence in DACH, Central Europe, and Central-Southeastern Europe with its March 2026 acquisition of Hauser for over EUR 2 billion (USD 2.2 billion). This acquisition added production facilities in Austria and the Czech Republic and enhanced Epta's offerings in natural refrigeration and energy-efficient solutions.

The Middle East is emerging as a key destination for QSR investments. Dairy Queen is targeting the UAE and Saudi Arabia, where QSR markets are expected to grow at over 14% CAGR. Notably, 85% of fast-food consumers in Saudi Arabia are under the age of 45. Meanwhile, Latin America faces challenges such as grid instability and capital constraints. South Africa's cold chain sector reports monthly mitigation costs ranging from ZAR 50,000 to over ZAR 1 million, along with revenue losses between ZAR 50,000 and ZAR 500,000 due to load-shedding. To address power fluctuations and minimize downtime, regions in Sub-Saharan Africa and parts of Latin America are adopting robust, low-tech units with manual controls and battery-backed alarms.

- Ali Group

- AHT Cooling Systems

- Taylor Company

- Electrolux Professional

- Haier Group

- Bonnet Neve

- Delfield (Middleby Corporation)

- Electrolux Professional

- Epta Group

- Excellence Industries

- Fagor Industrial

- Foster Refrigerator (ITV Group)

- GGM Gastro

- Gram Commercial A/S

- Haier Group (GE Appliances)

- Hoshizaki Corporation

- Hussmann Corp.

- Igloo Products Corp.

- Imbera Cooling

- ISA Italy

- Liebherr-Hausgerate GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion Of Quick-Service Restaurant Chains In Emerging Markets

- 4.2.2 Growth In Impulse Ice-Cream Retail At Convenience And Fuel Stops

- 4.2.3 Energy-Efficiency Regulations Accelerating Equipment Replacements

- 4.2.4 Rising Frozen-Dessert Consumption In Asia-Pacific

- 4.2.5 IoT-Enabled Predictive Maintenance Adoption

- 4.2.6 Freezer-As-A-Service Leasing Lowering Capital Expenditures

- 4.3 Market Restraints

- 4.3.1 High Upfront Procurement And Installation Costs

- 4.3.2 Stringent Refrigerant Phase-Out Rules For HFC, HFO, And F-Gas

- 4.3.3 Grid Instability In Developing Regions Reducing Uptime

- 4.3.4 Boom In Second-Hand Equipment Trade Cannibalizing New Sales

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Chest And Deep Freezers

- 5.1.2 Upright Freezers

- 5.1.3 Glass-Top Display Freezers

- 5.1.4 Ice-Cream Dipping Cabinets

- 5.1.5 Gelato And Soft-Serve Batch Freezers

- 5.2 By Cooling Technology

- 5.2.1 Static Cooling

- 5.2.2 Ventilated And Forced-Air Cooling

- 5.2.3 Frost-Free And No-Frost Systems

- 5.2.4 Remote Glycol-Cooled Systems

- 5.3 By Capacity

- 5.3.1 Less Than Or Equal To 300 Liters

- 5.3.2 301 To 600 Liters

- 5.3.3 Greater Than 600 Liters

- 5.4 By End User

- 5.4.1 Ice-Cream Parlors And Gelaterias

- 5.4.2 Quick-Service Restaurants (QSRs)

- 5.4.3 Supermarkets And Hypermarkets

- 5.4.4 Convenience Stores And Fuel Stations

- 5.4.5 Cinemas, Stadiums, And Entertainment Venues

- 5.4.6 Catering And Institutional Foodservice

- 5.5 By Sales Channel

- 5.5.1 Direct OEM

- 5.5.2 Distributor And Dealer

- 5.5.3 Online

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Sweden

- 5.6.2.8 Poland

- 5.6.2.9 Belgium

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Vietnam

- 5.6.3.7 Indonesia

- 5.6.3.8 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Peru

- 5.6.4.5 Colombia

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Ali Group

- 6.4.2 AHT Cooling Systems

- 6.4.3 Taylor Company

- 6.4.4 Electrolux Professional

- 6.4.5 Haier Group

- 6.4.6 Bonnet Neve

- 6.4.7 Delfield (Middleby Corporation)

- 6.4.8 Electrolux Professional

- 6.4.9 Epta Group

- 6.4.10 Excellence Industries

- 6.4.11 Fagor Industrial

- 6.4.12 Foster Refrigerator (ITV Group)

- 6.4.13 GGM Gastro

- 6.4.14 Gram Commercial A/S

- 6.4.15 Haier Group (GE Appliances)

- 6.4.16 Hoshizaki Corporation

- 6.4.17 Hussmann Corp.

- 6.4.18 Igloo Products Corp.

- 6.4.19 Imbera Cooling

- 6.4.20 ISA Italy

- 6.4.21 Liebherr-Hausgerate GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK