PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062213

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062213

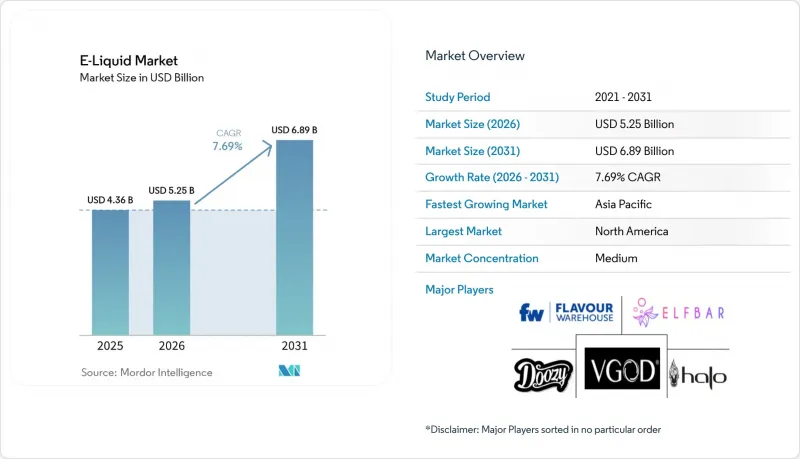

E-Liquid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the e-liquid market size is expected to be USD 4.36 billion in 2025, USD 5.25 billion in 2026, and reach USD 6.89 billion by 2031, growing at a CAGR of 7.69% from 2026 to 2031.

This report is Segmented by Flavor (Flavored and Unflavored), Bottle Size/E-Liquid Capacity (Below 30ml, 30ml To 60ml, and Above 60ml), Nicotine Type (With Nicotine and Without Nicotine), Distribution Channel (Offline Stores and Online Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global E-Liquid Market Trends and Insights

Increasing Appeal of Vaping as a Perceived Safer Alternative to Traditional Smoking

Harm-reduction positioning continues to anchor market expansion, yet the narrative is bifurcating between jurisdictions that embrace tobacco-harm-reduction frameworks and those imposing precautionary bans. Philip Morris International's smoke-free portfolio, which now generates 41.5% of net revenues, demonstrates how incumbents are pivoting capital toward reduced-risk products, with VEEV e-vapor unit shipments surging 102% to 3.3 billion in 2025. The company's over USD 20 billion investment since 2022 includes a USD 600 million ZYN nicotine-pouch facility in Colorado that opened in September 2025, signaling a broader shift toward oral nicotine as a complementary category. However, this growth trajectory faces headwinds from markets like India, where the Prohibition of Electronic Cigarettes Act 2019 imposes penalties of up to INR 500,000 (approximately USD 6,000) and 3 years' imprisonment for repeat offenses, yet sustains an estimated annual illicit market of USD 100 million. The regulatory divergence creates a dual-track industry where multinational firms pursue premium, compliant channels in regulated markets while gray-market operators exploit prohibition-driven demand in ban jurisdictions.

Broad Range of Flavors and Nicotine Strengths Designed to Attract Diverse Consumer Preferences

Flavor diversity remains the primary differentiation lever, with flavored formulations holding 95.48% share in 2025, yet regulatory momentum is shifting toward tobacco-only mandates that could reshape product portfolios. Seven European Union member states have enacted flavor bans, and 19 countries now tax vaping products, compressing margins and limiting SKU proliferation. The Fraunhofer Institute projects the EU illicit vape market will expand from EUR 6.6 billion currently to EUR 10.8 billion by 2030, driven largely by flavor bans that push consumers toward unregulated suppliers. This unintended consequence reveals a strategic blind spot: overly restrictive flavor policies erode tax revenue and public-health oversight without curbing demand. Conversely, markets like Chile, which implemented Law 21,642 in January 2024 with a 45mg/mL nicotine cap and mandatory health warnings but preserved flavor availability, demonstrate a middle path that balances youth-access controls with adult consumer choice.

Strict Regulations Governing Nicotine Levels and Advertising Restrictions

Regulatory fragmentation is compressing addressable markets and elevating compliance costs, with divergent nicotine caps and advertising bans creating operational complexity for multinational operators. The UAE's 20mg/mL nicotine limit and 10ml container cap align with European Union Tobacco Products Directive standards, yet markets like Chile permit 45mg/mL concentrations, forcing brands to maintain parallel SKU portfolios, according to the Emirates Authority for Standardization and Metrology. China's State Tobacco Monopoly Administration enforcement intensified in 2025, with 19,896 administrative cases and 5,539 criminal cases resulting in over 63.145 million illegal products seized and case values exceeding CNY 15 billion (approximately USD 2.1 billion) Vaping360. The UK's Vaping Products Duty, set at EUR 2.20 per 10ml effective October 2026, will add approximately 15-20% to retail prices, potentially dampening volume growth and incentivizing down-trading to lower-nicotine formulations. The FDA's March 2026 draft guidance on flavored ENDS introduces premarket tobacco application pathways that require clinical evidence of reduced youth appeal, a standard that smaller brands lack the resources to meet. This regulatory ratcheting favors vertically integrated tobacco companies like Philip Morris International, which deployed over USD 20 billion in US smoke-free infrastructure and can amortize compliance costs across broader portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Convenience and User-Friendly Nature of Pre-Filled Vaping Devices

- Expansion of Online Retail Channels Enhancing Product Availability and Accessibility

- Consumer Health Worries About the Long-Term Effects of Regular Vaping

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, flavored products accounted for a significant 95.48% of the turnover. However, these products are under increasing scrutiny from policymakers. At the same time, the e-liquid market is experiencing a shift, with unflavored lines projected to grow at an impressive 9.35% CAGR, surpassing the overall market growth. This trend is primarily driven by the alignment of risk-averse consumers and regulators who prefer simpler ingredient profiles. Premium brands are strategically emphasizing dessert and beverage notes, which not only help sustain profit margins but also position these flavors as alternatives for adult smokers, avoiding appeal to younger audiences. Nevertheless, a major challenge persists: seven EU nations have already prohibited non-tobacco flavors, disrupting supply chains and pushing price-sensitive consumers toward illicit imports.

The rise in unflavored product demand is also associated with the gradual reduction in nicotine strength. Many former smokers transitioning to zero-nicotine options prefer neutral flavors to avoid reminders of cigarettes. In North America, transparent bottle labeling and ISO-certified purity enhance consumer trust, enabling brands to justify slight price premiums. Flavor houses are responding by developing heat-stable compounds that reduce carbonyl formation, serving as a precaution against potential widespread flavor bans. As the e-liquid market continues to evolve, portfolio planners face the challenge of balancing flavor innovation with the preparation of contingency SKUs for markets with flavor restrictions.

By 2025, formats under 30 ml contributed 65.29% of the revenue and are expected to grow at a strong 9.56% CAGR through 2031. The EU's 10 ml restriction on nicotine liquids, along with the UAE's 10 ml container regulation, is driving demand for smaller bottles, ensuring both portability and compliance with regulations. At the same time, the market share for 30-to-60 ml e-liquids is shrinking. This reduction is primarily due to excise taxes linked to volume, which erode their cost advantage, a trend likely to accelerate with the upcoming U.K. duty.

Small packs are becoming increasingly popular, particularly with pod-based devices that use 2 ml cartridges. Consumers often opt for multiple smaller flavor shots instead of a single large bottle, increasing overall liquid sales. Packaging suppliers are differentiating themselves with features such as child-resistant caps and laser-etched batch codes, which simplify retail audits. While bottles over 60 ml still appeal to hobbyists using open-tank systems, this segment is declining. Mainstream users are shifting towards convenience, and the adoption of higher-efficiency coils has significantly reduced refill frequency.

Geography Analysis

In 2025, North America contributed 42.32% of global revenues, with the U.S. leading due to its extensive distribution networks, established hardware ecosystems, and a large smoker population. Since 2022, Philip Morris International has invested over USD 20 billion in U.S. smoke-free infrastructure, including a USD 600 million nicotine-pouch facility launched in Colorado in 2025. While FDA's pre-market pathways increase entry barriers, they also enhance consumer trust, supporting premium-brand pricing. Europe presents a varied landscape. The U.K.'s disposable ban, effective June 2025, has driven a shift to refillable pods, reducing annual consumer spending by approximately 74%, according to the Government of the United Kingdom . The upcoming EU Battery Regulation will eliminate single-use devices across 27 countries by February 2027, requiring manufacturers to quickly adapt their portfolios. Furthermore, a EUR 2.20 per 10 ml duty, starting October 2026, is expected to raise price floors, potentially reducing volume but increasing tax revenues.

Asia-Pacific is the key growth region, with a projected CAGR of 8.65% through 2031E. China's capacity caps and mandatory plant registrations are limiting unchecked expansions while protecting established players from oversupply risks. Japan's pharmacy-only rule for nicotine liquids supports a thriving zero-nicotine market, while Australia's prescription model demonstrates how medical frameworks can coexist with commercial supply chains. Latin America features a mix of restrictive and liberal policies. Chile's 2024 Law 21 642 maintained the legality of flavors but introduced a 45 mg/ml nicotine cap and enforced 18+ age verification. Although Brazil continues to ban sales, cross-border e-commerce sustains a significant gray market, highlighting how outright bans often redirect demand rather than eliminate it.

The Middle East and Africa exhibit diverse dynamics. The UAE's ESMA code enforces some of the world's strictest labeling requirements while allowing compliant products to succeed. Saudi Arabia's ongoing ban has resulted in spillover purchases in Bahrain and the UAE. In sub-Saharan Africa, Nigeria and South Africa, two of the region's fastest-growing economies, currently lack comprehensive regulations, creating opportunities for early entrants focused on quality assurance and youth protection.

- HALOCIGS

- FLAVOUR WAREHOUSE LTD

- Elf Bar

- Doozy Vape Co.

- VGOD INC.

- RELX Technology Ltd.

- Philip Morris International Inc.

- Turning Point Brands Inc.

- Nasty Worldwide Sdn Bhd

- Dinner Lady Ltd.

- Nicopure Labs LLC (Halo)

- Element E-Liquids LLC

- Vapetasia LLC

- Hangsen International Group

- FlavourArt Srl

- AVAIL Vapor LLC

- Black Note Inc.

- PachaMama (E-Liquid Labs)

- Riot Labs Ltd.

- Charlie's Chalk Dust LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Appeal Of Vaping As A Perceived Safer Alternative To Traditional Smoking

- 4.2.2 Broad Range Of Flavors And Nicotine Strengths Designed To Attract Diverse Consumer Preferences

- 4.2.3 Convenience And User-Friendly Nature Of Pre-Filled Vaping Devices

- 4.2.4 Expansion Of Online Retail Channels Enhancing Product Availability And Accessibility

- 4.2.5 Ongoing Product Innovation In Devices And E-Liquids

- 4.2.6 Greater Emphasis On Product Transparency Through Clear Ingredient And Nicotine Labeling

- 4.3 Market Restraints

- 4.3.1 Strict Regulations Governing Nicotine Levels And Advertising Restrictions

- 4.3.2 Consumer Health Worries About The Long-Term Effects Of Regular Vaping

- 4.3.3 Challenges In Securing Stable Supplies And Raw Materials For E-Liquid Production

- 4.3.4 Complex And Frequently Changing Compliance Requirements Across Markets

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Flavor

- 5.1.1 Flavored

- 5.1.2 Unflavored

- 5.2 By Bottle Size/E-Liquid Capacity

- 5.2.1 Below 30 ml

- 5.2.2 30 ml To 60 ml

- 5.2.3 Above 60 ml

- 5.3 By Nicotine Type

- 5.3.1 With Nicotine

- 5.3.2 Without Nicotine

- 5.4 By Distribution Channel

- 5.4.1 Offline Stores

- 5.4.2 Online Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Sweden

- 5.5.2.8 Poland

- 5.5.2.9 Belgium

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Vietnam

- 5.5.3.7 Indonesia

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Peru

- 5.5.4.5 Colombia

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 HALOCIGS

- 6.4.2 FLAVOUR WAREHOUSE LTD

- 6.4.3 Elf Bar

- 6.4.4 Doozy Vape Co.

- 6.4.5 VGOD INC.

- 6.4.6 RELX Technology Ltd.

- 6.4.7 Philip Morris International Inc.

- 6.4.8 Turning Point Brands Inc.

- 6.4.9 Nasty Worldwide Sdn Bhd

- 6.4.10 Dinner Lady Ltd.

- 6.4.11 Nicopure Labs LLC (Halo)

- 6.4.12 Element E-Liquids LLC

- 6.4.13 Vapetasia LLC

- 6.4.14 Hangsen International Group

- 6.4.15 FlavourArt Srl

- 6.4.16 AVAIL Vapor LLC

- 6.4.17 Black Note Inc.

- 6.4.18 PachaMama (E-Liquid Labs)

- 6.4.19 Riot Labs Ltd.

- 6.4.20 Charlie's Chalk Dust LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK