PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062226

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062226

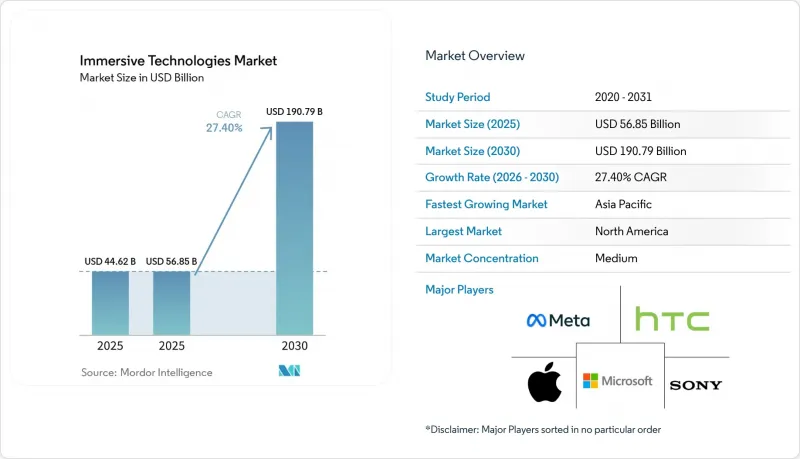

Immersive Technologies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the immersive technologies market size reached USD 44.62 billion in 2025 and is forecast to expand to USD 152.73 billion by 2030, reflecting a 27.90% CAGR during the period.

This report is Segmented by Technology (Augmented Reality, Virtual Reality, Mixed Reality, and More, Component (Hardware, Software, and Services), Application (Training and Simulation, Remote Collaboration), Product Design and Prototyping, and More), End-User Industry (Gaming and Entertainment, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Immersive Technologies Market Trends and Insights

Enterprise Training and Simulation Cost-Reduction Initiatives

Enterprises validate immersive deployments when financial models prove that shorter training cycles offset upfront device costs. Surgical rehearsal in orthopedics trimmed average operating-room time by 18 minutes and lowered complications by 15-20%. Manufacturers such as Roche compressed pharmaceutical line validation from six months to eight weeks using digital twins. At scale, fleets above 500 headsets reduce per-seat licensing by 35%, turning previously experimental pilots into standard operating procedure. These gains make the immersive technologies market attractive even to budget-constrained sectors seeking measurable productivity boosts.

Surging Consumer AR and VR Headset Adoption for Gaming and Entertainment

Consumer momentum spills into the enterprise when employees bring headset familiarity to work. China shipped 18 million consumer units in 2025, a 50% jump in one year. Meta's Ray-Ban smart glasses surpassed 1 million sales by mid-2025, showing that slimmer designs broaden appeal. Japan's metaverse spending is tracking toward JPY 1 trillion (USD 7.3 billion) in 2026 because virtual concerts and avatar commerce monetize longer engagement. Stand-alone headsets now launch in under three minutes, a usability leap that raised daily active users by 40% in Meta's ecosystem. The resulting familiarity lowers corporate onboarding time and accelerates project approval for new immersive rollouts.

High Upfront Capex for Enterprise-Grade Deployments

Comprehensive rollouts often require USD 50,000-USD 500,000 for hardware fleets, software licenses, and integration, which stretches payback beyond typical IT refresh windows. Smaller firms in emerging markets face scarce local integrators and must import expertise at daily rates above USD 2,000, adding 25-30% to project budgets. Financing models such as XR as a Service remain below 15% penetration because three-year minimum terms and double-digit effective interest rates blunt liquidity benefits. CFOs delay fleet orders until pilots prove ROI, slowing conversion from proof of concept to production use. Longer hardware life cycles will gradually ease this restraint, but capital intensity still tempers the near-term outlook for the immersive technologies market.

Other drivers and restraints analyzed in the detailed report include:

- 5G Edge Rendering Enabling Lighter, Cheaper Wearables

- Photogrammetry-Based Digital Twins Accelerating Design Cycles

- Health and Safety Concerns (Eye Strain, Cybersickness)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virtual reality accounted for 31.8% of revenue in 2025, dominating entertainment and fully immersive training programs. The immersive technologies market share is gradually shifting as mixed reality accelerates at a 32.3% CAGR through 2031, thanks to full-color passthrough that lets users see tools and teammates during digital interaction. Apple Vision Pro and Meta Quest 3 both toggle between VR and MR modes, eliminating procurement dilemmas and cutting device inventory. In manufacturing lines and operating rooms, teams favor MR for multi-hour workflows where physical situational awareness is mandatory. Augmented reality maintains a niche for field-service guidance because it overlays schematics without isolating the wearer. Extended reality serves as procurement shorthand for multi-modal deployments and increasingly appears in enterprise RFPs. Convergence is likely as software platforms speak to device-agnostic runtimes, letting firms deploy the right mode for each task without locking into single-use hardware.

Demand for MR elevates service engagements that integrate computer vision, spatial mapping, and safety certification. Integrators report that MR rollouts take 30% longer than VR because physical-world occlusion and object anchoring must remain precise. Nevertheless, per seat economics improve once deployments reach 500 devices, which is when shared content libraries amortize engineering costs. As vendors refine onboard depth sensors and pass-through latency falls below fifteen milliseconds, user comfort grows and dwell times lengthen. The resulting productivity boost reinforces MR's position as the primary growth engine for the immersive technologies market.

Hardware captured 63.9% of 2025 spending, reflecting the headset fleets that launched many proof-of-concept pilots. Yet services are scaling at a 31.8% CAGR because enterprises now purchase multi-year managed offerings that include content refresh, analytics, and user support. The immersive technologies market size for services is projected to outpace device revenue before 2031 as buyers trade capital expense for predictable operating budgets. Integrators bundle hardware leasing, custom 3D asset creation, and 24-hour help desks into contracts priced at USD 100,000-USD 2 million per year. Software platforms benefit indirectly because robust services teams drive higher seat utilization and license renewals.

Inside-out optical tracking has eliminated external base stations, shrinking set-up from forty-five to five minutes and making pop-up classrooms possible on factory floors. Collaborative display walls regain interest for design reviews because ten stakeholders can view a twin without donning separate headsets. Service providers add value by curating these multimodal environments and ensuring data security across devices and cloud endpoints. As regulations tighten around biometric information, compliance consulting further inflates the services opportunity. Hardware vendors respond by opening SDKs and partnering with integrators, a symbiosis that cements services as the fastest-growing slice of the immersive technologies market.

Geography Analysis

North America generated 27.4% of 2025 revenue and remains a reference region for enterprise best practices in manufacturing, healthcare and defense. Buyers emphasize integration with legacy IT and favor suppliers that document cybersecurity compliance. Federal training budgets and defense research grants ensure a baseline of multi-year demand, even when consumer sentiment fluctuates. Services partners cluster around metropolitan hubs, enabling nationwide coverage without diluting quality.

Asia-Pacific is the fastest climber at a 32.6% CAGR through 2031 as governments classify immersive labs as strategic infrastructure. China achieved 45% domestic device autonomy and 60% component localization in 2025, insulating production from export controls. India earmarked INR 391.15 crore (USD 46.8 million) for the Indian Institute of Creative Technologies and embedded AVGC labs in 15,000 schools and 500 colleges. Such public investment creates a predictable pipeline demand that venture funding can leverage. Regional vendors like Pico hold more than 25% of China's unit shipments, showing that local champions can thrive alongside multinationals.

Europe benefits from GDPR and the EU AI Act, which clarify biometric data rules and shorten enterprise procurement cycles in regulated sectors. Clear sovereignty guidelines lift buyer confidence, though compliance adds consulting overhead that favors vendors with dedicated legal teams. South America and the Middle East and Africa trail because 5G build-outs and device import duties raise effective headset prices by up to 50%. Nonetheless, pilot programs in Brazil and Saudi Arabia demonstrate pent-up interest once connectivity barriers fall. Overall, geographic diversification anchors the long-term resilience of the immersive technologies market.

- Meta Platforms (Reality Labs)

- Microsoft Corporation

- Apple Inc.

- HTC Corporation (Vive)

- Sony Group Corporation

- Alphabet Inc. (Google)

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Magic Leap, Inc.

- Unity Technologies

- NVIDIA Corporation

- PTC Inc. (Vuforia)

- Varjo Technologies

- Lenovo Group Limited

- Ultraleap Ltd.

- Pico Interactive

- DPVR (Deepoon)

- TeamViewer (Frontline)

- Epson (Moverio)

- Avegant Corporation

- Valve Corporation

- Snap Inc.

- Niantic, Inc.

- Vuzix Corporation

- Autodesk Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value / Supply-Chain Analysis

- 4.3 Impact of Macroeconomic Factors on the Market

- 4.4 Market Drivers

- 4.4.1 Surging Consumer AR/VR Headset Adoption for Gaming and Entertainment

- 4.4.2 Enterprise Training and Simulation Cost-Reduction Initiatives

- 4.4.3 Declining Hardware ASPs Driven by Next-Gen Chipsets

- 4.4.4 Content-as-a-Service Business Models Unlocking Recurring Revenue

- 4.4.5 5G Edge Rendering Enabling Lighter, Cheaper Wearables

- 4.4.6 Photogrammetry-Based Digital Twins Accelerating Design Cycles

- 4.5 Market Restraints

- 4.5.1 High Upfront Capex for Enterprise-Grade Deployments

- 4.5.2 Health and Safety Concerns (Eye Strain, Cybersickness)

- 4.5.3 Supply-Chain Reliance on Rare-Earth Magnets for Haptics

- 4.5.4 Spatial-Data Privacy and Sovereignty Regulations

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Augmented Reality (AR)

- 5.1.2 Virtual Reality (VR)

- 5.1.3 Mixed Reality (MR)

- 5.1.4 Extended Reality (XR)

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Head-Mounted Displays (HMDs)

- 5.2.1.2 Head-Up Displays (HUDs)

- 5.2.1.3 Projectors and Display Walls

- 5.2.1.4 Sensors and Tracking Systems

- 5.2.2 Software

- 5.2.2.1 AR/VR Content Creation Platforms

- 5.2.2.2 Simulation Software

- 5.2.2.3 Real-Time Rendering Engines

- 5.2.3 Services

- 5.2.3.1 Integration and Deployment

- 5.2.3.2 Consulting and Training

- 5.2.3.3 Support and Maintenance

- 5.2.1 Hardware

- 5.3 By Application

- 5.3.1 Training and Simulation

- 5.3.2 Remote Collaboration

- 5.3.3 Product Design and Prototyping

- 5.3.4 Marketing and Advertising

- 5.3.5 Retail Visualization

- 5.3.6 Patient Therapy and Surgical Planning

- 5.3.7 Entertainment and Gaming

- 5.3.8 Other Applications

- 5.4 By End-User Industry

- 5.4.1 Gaming and Entertainment

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Education and EdTech

- 5.4.4 Manufacturing and Industrial

- 5.4.5 Retail and E-Commerce

- 5.4.6 Aerospace and Defense

- 5.4.7 Automotive

- 5.4.8 Real Estate and Architecture

- 5.4.9 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Meta Platforms (Reality Labs)

- 6.4.2 Microsoft Corporation

- 6.4.3 Apple Inc.

- 6.4.4 HTC Corporation (Vive)

- 6.4.5 Sony Group Corporation

- 6.4.6 Alphabet Inc. (Google)

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Magic Leap, Inc.

- 6.4.10 Unity Technologies

- 6.4.11 NVIDIA Corporation

- 6.4.12 PTC Inc. (Vuforia)

- 6.4.13 Varjo Technologies

- 6.4.14 Lenovo Group Limited

- 6.4.15 Ultraleap Ltd.

- 6.4.16 Pico Interactive

- 6.4.17 DPVR (Deepoon)

- 6.4.18 TeamViewer (Frontline)

- 6.4.19 Epson (Moverio)

- 6.4.20 Avegant Corporation

- 6.4.21 Valve Corporation

- 6.4.22 Snap Inc.

- 6.4.23 Niantic, Inc.

- 6.4.24 Vuzix Corporation

- 6.4.25 Autodesk Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment