PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062258

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062258

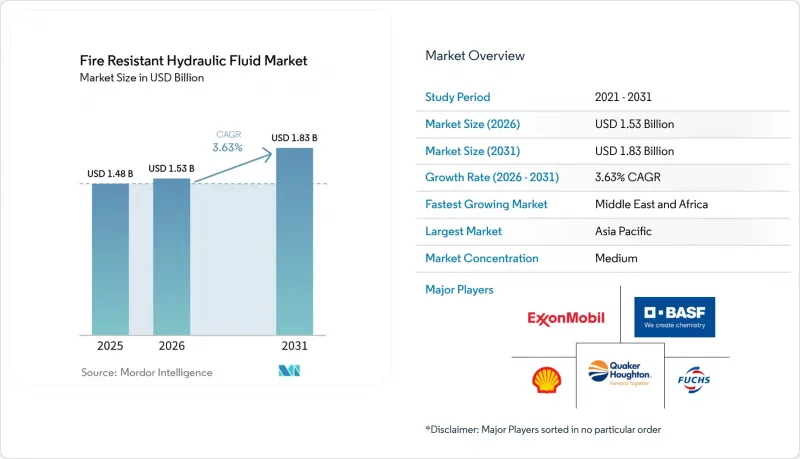

Fire Resistant Hydraulic Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fire resistant hydraulic fluid market size was valued at USD 1.48 billion in 2025 and is estimated to grow from USD 1.53 billion in 2026 to reach USD 1.83 billion by 2031, at a CAGR of 3.63% during the forecast period (2026-2031).

This report is Segmented by Fluid Type (HFAE Oil-In-Water Emulsion, HFAS Synthetic Solution, and More), Application (Steel and Foundry, Mining and Tunnelling, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Fire Resistant Hydraulic Fluid Market Trends and Insights

Automation and Electrification Raise Flash-Point Thresholds

As mobile machinery increasingly adopts electrification, the integration of batteries, inverters, and hydraulic drives into compact frames raises the risk of ignition, particularly in the presence of mineral oils. Major Original Equipment Manufacturers (OEMs) like Volvo and Caterpillar are mandating fire-resistant hydraulic fluids for electro-hydraulic steering systems and incorporating circuits designed to mitigate battery-related fires. Underground mines utilizing battery electric loaders have observed reduced insurance premiums when switching from mineral oils to HFDU (Hydraulic Fluid, Fire-Resistant, Synthetic Ester) esters. HFDU esters' self-extinguishing properties and minimal smoke emission in confined tunnels make them a preferred choice. Procurement teams are prioritizing ISO 6743/4 HFDU and HFC (Hydraulic Fluid, Fire-Resistant, Water-Containing) compliance as a standard for new model launches. Additionally, municipal contractors working near residential areas are increasingly opting for synthetic esters with EU Ecolabel credentials due to their low toxicity and odor profiles. This trend highlights a shift: fire-resistant hydraulic fluid products are now being integrated during the design phase rather than as retrofits.

Offshore Wind Expansion With Electro-Hydraulic Pitch Systems

Modern offshore wind turbines utilize electro-hydraulic cylinders to quickly pivot 20-ton blades, ensuring optimal power regulation even in 50 meters per second (m/s) wind gusts. These pitch circuits, operating at pressures up to 400 bar, must react promptly after periods of dormancy without succumbing to cavitation. This requirement eliminates the possibility of using water-based emulsions, which are prone to separation in cold, saline environments. OEM qualification lists are increasingly favoring HFDU esters, known for maintaining bulk modulus at -25°C and providing enhanced lubricity for bronze bearings in yaw drives. Environmental regulators are also emphasizing the need for fluids to be biodegradable, especially in scenarios of hub leakage at sea. With regions like the North Sea, Taiwan Strait, and the U.S. Atlantic coast introducing multi-megawatt turbines, each nacelle's recurring fill volume of nearly 1,000 liters is driving sustained demand for premium esters, even at a 20-25% price premium. This trend supports the long-term growth prospects of the fire-resistant hydraulic fluid market.

Seal and Elastomer Compatibility Limitations Elevate Maintenance Burden

Standard nitrile (NBR) seals can swell when exposed to phosphate-ester and certain ester chemistries. Additionally, some ionic fluids can reduce the durability of fluoroelastomer (FKM) seals after 70,000 pressure cycles. As a result, retrofit projects require seal kits, increasing component costs by up to 20%, which can be a challenge for smaller operators. Furthermore, water-glycol fluids may corrode zinc or magnesium in valve bodies unless mitigated by special coatings. These compatibility challenges hinder the conversion of installed equipment and impact the growth rate of the fire-resistant hydraulic fluid market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Safety-Critical Hydraulics in Aerospace Production

- Real-Time Fluid Monitoring Extends Drain Intervals

- Phosphate-Ester Raw-Material Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Hydrofluorocarbon (HFC) water-glycol secured a 31.22% share of the fire-resistant hydraulic fluid market, primarily due to cost advantages. This was particularly evident in steel-mill caster hydraulics, which can accommodate its lower lubricity. Meanwhile, the market for Hydraulic Fluid Type Universal (HFDU) esters is set to grow at a 3.56% Compound Annual Growth Rate (CAGR) until 2031. This growth is driven by marine, mining, and construction fleets opting for fluids compliant with FM 6930 and ISO 15380, ensuring protection against water-related corrosion. Quaker Houghton's QUINTOLUBRIC 888 series offers over 86% biodegradability and a fire point of 357°C, making it a preferred choice for offshore cranes. TotalEnergies' Hydransafe HFDU 46, with a 310°C flash point and over 61% biodegradability, positions esters as alternatives to phosphate esters, especially as environmental regulations tighten. While phosphate-ester Hydraulic Fluid Type Resistant (HFDR) fluids maintain a niche leadership in aerospace due to their 200°C thermal stability, pressures from Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) labeling are prompting end users to consider alternatives. Hydraulic Fluid Type Aqueous Emulsion (HFAE) and Hydraulic Fluid Type Aqueous Solution (HFAS) oil-in-water solutions are tailored for underground coal equipment, adhering to 30 CFR 75 regulations. In contrast, Polyalkylene Glycol (PAG)-based and ionic liquids, though occupying a specialty niche, hold a combined share of less than 5%, constrained by ongoing seal-compatibility research.

Synthetic esters, despite being priced about 20% higher per liter, offer extended service life through predictive maintenance, reducing the lifecycle premium. Endorsements from Original Equipment Manufacturers (OEMs) in sectors like wind, tunneling, and hydropower further validate HFDU technology, reinforcing its role in future formulations. As Environmental, Social, and Governance (ESG) mandates gain traction, the industry is shifting towards esters, prompting a reevaluation of competitive strategies in the fire-resistant hydraulic fluid market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 34.11% of global revenue, supported by China's steel production and local suppliers like Hardcastle Petrofer in India. Chemical producers in the region are offering Hydraulic Fluid Designed for Use (HFDU) fluids at competitive rates of USD 2-5 per kg, driving domestic adoption. Additionally, government initiatives promoting green mining in China's Hebei and Shanxi provinces have increased demand for biodegradable esters. Meanwhile, Japan and South Korea are importing aviation-grade phosphate esters, ensuring compliance with stringent purity standards for aerospace programs.

The Middle East and Africa are projected to experience the fastest growth, with a Compound Annual Growth Rate (CAGR) of 4.67% from 2026. This growth is driven by offshore rigs in Saudi Arabia and the United Arab Emirates (UAE), which require Factory Mutual (FM)-approved fluids to meet insurance requirements. Furthermore, new wind concessions in the Red Sea and the Gulf of Suez are increasing demand for turbine hydraulic volumes. In South Africa, gold and platinum mines, adhering to stricter underground fire codes, are increasingly adopting HFDU esters compatible with Hydrogenated Nitrile Butadiene Rubber (HNBR) seals.

North America is benefiting from reshored glycol blending operations in Ohio and Ontario, ensuring a stable supply for steel plants around the Great Lakes. Steady defense orders in the United States (U.S.) are supporting phosphate ester throughput, while wind farms along the Atlantic coast are driving consistent demand for esters. In Mexico, automotive casting plants are transitioning to water-glycol alternatives to meet safety audit standards, strengthening cross-border trade under the United States-Mexico-Canada Agreement (USMCA).

Europe, led by Germany's heavy industry and platforms in the United Kingdom (U.K.) North Sea, is a key consumer. REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) toxicity constraints are encouraging ester substitutions, and European Union (EU) Ecolabel regulations are promoting biodegradable options, particularly in Alpine hydropower assets. The growing offshore wind sector in Scandinavia is reinforcing this demand, while Eastern European steel mills continue to prefer Hydrofluorocarbon (HFC) fluids due to cost considerations.

South America, while smaller in scale, holds strategic importance. Brazilian iron-ore operations and offshore explorations in Argentina are creating niche opportunities. However, challenges such as logistical hurdles and currency fluctuations are moderating immediate growth. Nevertheless, service contracts with Original Equipment Manufacturers (OEMs) are laying the foundation for the adoption of premium esters in the fire-resistant hydraulic fluid market.

- Afton Chemical

- BASF

- Castrol Limited

- CLARIANT

- Exxon Mobil Corporation

- FUCHS

- Greenwood Aerospace

- Houghton International

- ICL

- Idemitsu Kosan

- Kawasaki KGR

- LANXESS

- Panolin AG

- Quaker Chemical Corporation

- Shell plc

- Sinopec Lubricants

- Solvay

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acceleration of automation and electrification raises flash-point thresholds

- 4.2.2 Expansion of offshore wind platforms using hydraulic pitch and mooring systems

- 4.2.3 Growth of safety-critical hydraulics in aviation and aerospace production

- 4.2.4 Real-time fluid-condition monitoring extends drain intervals and lowers TCO

- 4.2.5 Tariff-driven reshoring of glycol blending improves domestic supply security

- 4.3 Market Restraints

- 4.3.1 Seal/elastomer compatibility limitations elevate maintenance burden

- 4.3.2 Supply bottlenecks for phosphate-ester raw materials

- 4.3.3 Feed-stock tariff volatility and ESG scrutiny inflate HFC costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fluid Type

- 5.1.1 HFAE Oil-in-Water Emulsion

- 5.1.2 HFAS Synthetic Solution

- 5.1.3 HFB Water-in-Oil Emulsion

- 5.1.4 HFC Water-Glycol Solution

- 5.1.5 HFDR Phosphate-Ester

- 5.1.6 HFDU Synthetic/Ester

- 5.1.7 Other Niche Chemistries (PAG, Silicone, Ionic liquids)

- 5.2 By Application

- 5.2.1 Steel and Foundry

- 5.2.2 Mining and Tunnelling

- 5.2.3 Aviation and Aerospace Manufacturing

- 5.2.4 Power Generation (Thermal, Nuclear, Hydro)

- 5.2.5 Offshore Oil, Gas and Wind

- 5.2.6 Construction and Heavy Equipment

- 5.2.7 Automotive and Metal-Press Shops

- 5.2.8 Other Industries (Food, Die-casting, Marine)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Afton Chemical

- 6.4.2 BASF

- 6.4.3 Castrol Limited

- 6.4.4 CLARIANT

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 FUCHS

- 6.4.7 Greenwood Aerospace

- 6.4.8 Houghton International

- 6.4.9 ICL

- 6.4.10 Idemitsu Kosan

- 6.4.11 Kawasaki KGR

- 6.4.12 LANXESS

- 6.4.13 Panolin AG

- 6.4.14 Quaker Chemical Corporation

- 6.4.15 Shell plc

- 6.4.16 Sinopec Lubricants

- 6.4.17 Solvay

- 6.4.18 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment