PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062261

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062261

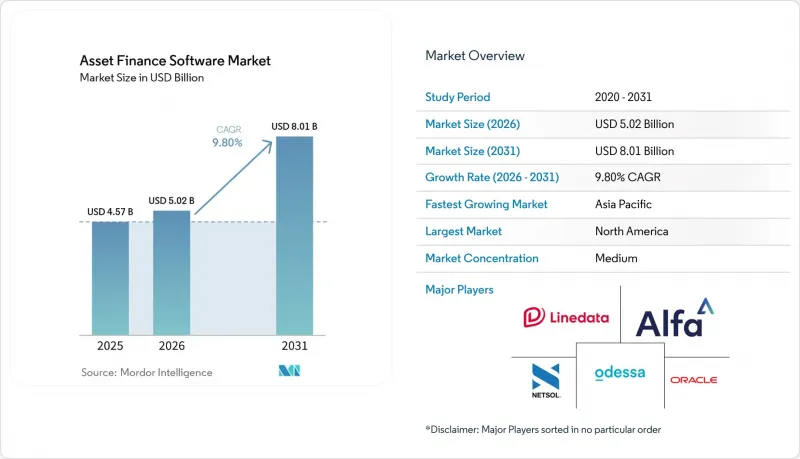

Asset Finance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asset finance software market size is projected to expand from USD 4.57 billion in 2025 and USD 5.02 billion in 2026 to USD 8.01 billion by 2031, registering a CAGR of 9.8% between 2026 and 2031.

This report is Segmented by Asset Type (Equipment Leasing, Real-Estate and Mortgage, Aircraft and Marine, and More), Deployment Model (Cloud and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Banks and Captive Finance Subsidiaries, Independent Finance and Leasing Companies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Asset Finance Software Market Trends and Insights

Growing Adoption of Digitalization and Automation in Asset-Finance Workflows

Manual origination once absorbed up to 40% of a lessor's operating costs. Platforms such as Odessa Auto now parse dealer invoices with intelligent document processing and trigger credit-risk APIs in real time, shrinking cycle times from three days to half a day. UniCredit's 2025 migration to Google Cloud allowed sub-hourly portfolio analytics, letting the bank reprice residual values daily. Robotic process automation (RPA) manages payment posting and delinquency queues, while AI chatbots handle routine borrower queries. Labor-intensive Western markets adopted first, yet digital-native lessors in India and Indonesia leapfrog directly to fully automated stacks.

Rising Demand for Cloud-Based Deployment Models

Cloud deployments save capital, shorten implementation, and support elastic scaling during seasonal peaks. FIS's 2025 release lets mid-market lessors spin up new product lines in weeks. Sopra Banking Software's 2026 Lending Suite launches with pre-integrated APIs to bureaus, telematics, and payments, eliminating year-long on-premise buildouts. APAC greenfield entrants prefer subscription pricing, while European incumbents embrace cloud to meet DORA resilience testing. A Singapore-based lessor can now activate an Indonesian instance with localized compliance settings in days instead of months.

High Implementation and Integration Costs for Complex Legacy Estates

Tier-1 banks spend nearly half their IT budget on maintaining 15-year-old core systems, stretching new platform rollouts to two years. On-premise licenses plus professional services can top USD 500,000 for just 50 users. Even SaaS adoptions must fund data migration, dual-running, and staff retraining, raising total ownership. Vendor-imposed proprietary APIs further lock incumbents into staged roadmaps that slow competitive response.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Equipment Leasing and Rental Volumes Worldwide

- Strengthening Regulatory Push for Granular Compliance and Reporting

- Persistent Data-Security and Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment leasing accounted for 42.9% of revenue in 2025, highlighting its breadth across machinery, IT, and medical devices. The segment benefits from large installed bases and predictable upgrade cycles, anchoring the asset finance software market. Aircraft and marine financing is forecast to post an 11.9% CAGR through 2031 as IoT sensors feed real-time engine data into residual-value analytics, reducing remarketing risk. Vendors that model component-level depreciation and multi-currency cash flows stand out.

Regional nuances sustain growth. North American hospitals lease surgical robots to preserve cash, while Southeast Asian airlines deploy software to align lease rentals with usage. Alfa Start's rapid-launch cloud suite trims go-live to 16 weeks for European mid-market lessors, illustrating demand for configurable, multi-asset coverage. As sustainability regulations tighten, platforms increasingly track carbon metrics alongside financial KPIs, differentiating offers for green fleets.

Cloud accounted for 57.8% of installations in 2025 and is projected to grow at a 13.5% CAGR, far exceeding on-premise expansions. The shift reflects subscription economics, vendor-managed infrastructure, and weekly feature drops that reduce backlog risk. Svea Bank's Nordic migration enabled seasonal scaling without hardware over-provisioning. Oracle's 2026 Agentic AI, offered only in cloud form, underscores the innovation gap widening between deployment models.

On-premise persists where data-sovereignty laws or mainframe ties prevail, especially among state-owned lenders. These customers accept a higher total cost for perceived control. Over time, however, R&D budgets tilt toward cloud, prompting legacy users to consider hybrid models. The asset finance software market size linked to cloud is expected to surpass USD 5 billion by 2031, reflecting this structural pivot.

Geography Analysis

North America accounted for 32.4% of revenue in 2025, supported by a mature equipment-leasing sector, deep captive-finance penetration, and early cloud adoption. DORA-style resilience rules have not yet arrived, but U.S. regulators are intensifying cyber-incident reporting, nudging cloud migrations. Software vendors co-develop residual-value analytics with fleet telematics providers to address the region's electrification drive. Europe benefits from DORA's January 2025 enforcement. Institutions prioritize platforms with built-in ICT testing, third-party oversight, and automated incident logs.

Germany, the United Kingdom, and France are advancing fastest, while Eastern Europe is accelerating as cross-border lessors unify systems to cut compliance overhead. The asset finance software market size in Europe is forecast to reach USD 2.6 billion by 2031. Asia-Pacific posts the highest regional CAGR at 12.8% through 2031. India and China ride SME equipment-finance booms embedded in e-commerce and supply-chain portals.

Nucleus Software's FinnOne Neo 8.5 targets these needs with localized language packs and plug-and-play bureau APIs. Southeast Asian lessors favor SaaS to bypass data-center buildouts, while Australia's miners seek AI-driven predictive maintenance for yellow-goods fleets. South America revives after currency volatility subsides. Argentina and Brazil both recorded above-40% leasing growth in 2025, driven by logistics and aircraft upgrades. Platforms with hedging modules and inflation indexing gain favor. The Middle East and Africa remain smaller but show bursts of activity as Islamic-finance houses digitize ijarah leasing and sovereign funds finance infrastructure.

- Odessa, Inc.

- Alfa Financial Software Holdings Plc

- Fidelity National Information Services, Inc.

- Linedata Services S.A.

- NETSOL Technologies, Inc.

- Oracle Corporation

- CGI Inc.

- Sopra Banking Software S.A.S.

- International Decision Systems, Inc.

- White Clarke Group Limited

- Infor, Inc.

- Banqsoft AS

- Intellect Design Arena Limited

- Nucleus Software Exports Limited

- Q2 Holdings, Inc.

- Temenos AG

- TRF Systems Inc.

- Cloud Lending, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Digitalization and Automation in Asset-Finance Workflows

- 4.2.2 Rising Demand for Cloud-Based Deployment Models

- 4.2.3 Expanding Equipment Leasing and Rental Volumes Worldwide

- 4.2.4 Strengthening Regulatory Push for Granular Compliance and Reporting

- 4.2.5 AI-Driven Residual-Value Analytics and Predictive Maintenance Integration

- 4.2.6 Rise of API-First Platforms Enabling Embedded Asset Finance

- 4.3 Market Restraints

- 4.3.1 High Implementation and Integration Costs for Complex Legacy Estates

- 4.3.2 Persistent Data-Security and Privacy Concerns

- 4.3.3 Legacy Core-Banking Lock-In Limiting Migration Velocity

- 4.3.4 Shortage of Domain-Specific Tech Talent for Asset-Finance Software

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porters Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Asset Type

- 5.1.1 Equipment Leasing

- 5.1.2 Automotive Finance

- 5.1.3 Real-Estate and Mortgage

- 5.1.4 Aircraft and Marine

- 5.1.5 Other Asset Types

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Banks and Captive Finance Subsidiaries

- 5.4.2 Independent Finance and Leasing Companies

- 5.4.3 FinTech and Digital-Only Lenders

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Odessa, Inc.

- 6.4.2 Alfa Financial Software Holdings Plc

- 6.4.3 Fidelity National Information Services, Inc.

- 6.4.4 Linedata Services S.A.

- 6.4.5 NETSOL Technologies, Inc.

- 6.4.6 Oracle Corporation

- 6.4.7 CGI Inc.

- 6.4.8 Sopra Banking Software S.A.S.

- 6.4.9 International Decision Systems, Inc.

- 6.4.10 White Clarke Group Limited

- 6.4.11 Infor, Inc.

- 6.4.12 Banqsoft AS

- 6.4.13 Intellect Design Arena Limited

- 6.4.14 Nucleus Software Exports Limited

- 6.4.15 Q2 Holdings, Inc.

- 6.4.16 Temenos AG

- 6.4.17 TRF Systems Inc.

- 6.4.18 Cloud Lending, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment