PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062266

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062266

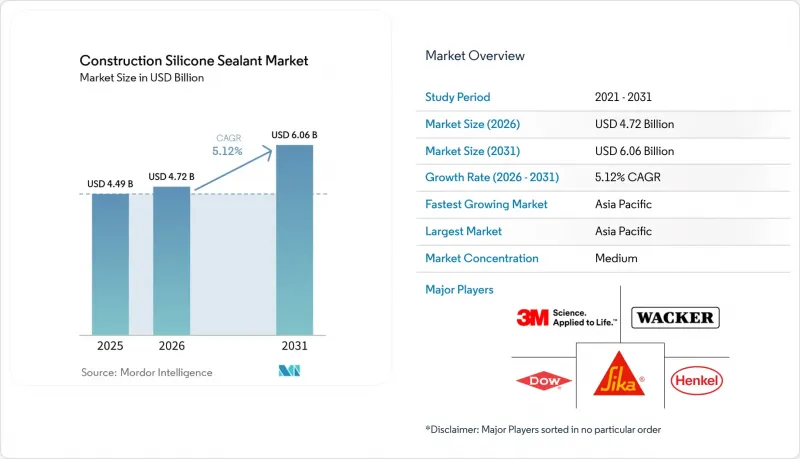

Construction Silicone Sealant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the construction silicone sealant market size is expected to increase from USD 4.49 billion in 2025 to USD 4.72 billion in 2026 and reach USD 6.06 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

This report is Segmented by Product Type (Neutral-Cure Silicone Sealants, Acetoxy-Cure Silicone Sealants, and More), Application (Joint Sealing, Glazing and Weatherproofing, and More), End-User (Residential Construction and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Silicone Sealant Market Trends and Insights

Rising Demand from Residential and Commercial Construction

In 2026, new office fit-out costs in the United States reached USD 149 per square foot, reflecting a 5.5% increase from 2025. This rise is driving developers to adopt longer-life sealants to reduce maintenance schedules. In China, prefabrication mandates are directing high-movement joints into factory environments, where neutral-cure silicones are predominantly used. Homeowners in tier-1 Asian cities are selecting low-odor products that resist substrate staining, a feature not commonly found in lower-cost acrylics. As labor markets tighten, project managers are focusing on total installed costs rather than just material prices. These factors collectively enhance silicone's positioning in premium residential towers and Grade-A commercial spaces.

Infrastructure Boom in Emerging Economies

India's Noida International Airport and Delhi Metro Phase V(A) represent a combined civil expenditure exceeding USD 2.7 billion, requiring sealants certified for +-25% movement and higher fire ratings. Similarly, expansions at Saudi Arabia's King Salman International and Dubai's Al Maktoum airports, with a combined value exceeding USD 64 billion, demand UV-stable, sand-resistant silicone joints to withstand extreme desert conditions. These large-scale projects provide multi-year opportunities for suppliers capable of ensuring batch consistency and offering on-site technical support. Additionally, extended design lead times benefit manufacturers that mitigate raw-material price volatility through backward integration or long-term silicon-metal contracts.

Volatility in Silicone and Additive Raw-Material Prices

In Q1 2026, prices for Dimethyldichlorosilane increased by 28% year-on-year, driven by outages at Chinese chlor-alkali units and higher tariffs on silicon metal. This price rise has impacted formulators reliant on spot market purchases. Additionally, shortages in fumed silica extended lead times from four to twelve weeks in late 2025. This situation benefited vertically integrated companies while creating challenges for small-batch contractors. In response to these market conditions, Wacker announced a mid-single-digit price increase in April 2026. Concurrently, Dow shifted its siloxane production from high-cost Europe to other regions to maintain competitiveness. These market dynamics introduce uncertainties in project budgeting and may lead to a shift toward more cost-effective chemistries when project specifications allow.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use in Green Buildings and Sustainable Architecture

- Surge in Unitized Curtain-Wall Adoption (High-Movement Joints)

- Competition from Acrylic, Polyurethane, and Polysulfide Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, neutral-cure products accounted for 44.11% of the construction silicone sealant market, supported by their compatibility with anodized aluminum, coated glass, and natural stone. Meanwhile, the market for acetoxy-cure grades is projected to grow at a 5.66% compound annual growth rate (CAGR) through 2031, driven by residential builders in Southeast Asia and Latin America who prefer the rapid moisture cure and a 30-40% lower unit cost. Oxime- and alkoxy-cure chemistries occupy smaller niches, catering to specialized needs like potable-water systems and automotive elastomer bonding. Premium tiers, exemplified by Momentive's 2025 bio-attributed room-temperature vulcanizing (RTV) range, are evolving to meet embodied-carbon disclosure demands. This competitive shift towards verified sustainability aims to address acetoxy-cure's growth in mainstream glazing applications.

The evolving product mix highlights a pricing hierarchy rather than a direct substitution. Dow's DOWSIL 791, a widely used acetoxy product, dominates over half of Southeast Asia's window-perimeter installations, reflecting cost-driven decisions in mass housing. On the other hand, Wacker's alkoxy-cure ELASTOSIL A07, compliant with Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) 177.2600 sanitization standards, secures demand from food-processing cleanrooms. Additionally, oxime-cure products are gaining traction in 3D-printed concrete facades due to their superior adhesion on porous substrates crafted through robotic extrusion. As building codes diversify based on specific use cases, no single chemistry is expected to dominate all niches, ensuring the relevance of multigrade portfolios.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.78% of global revenue and is projected to grow at a 6.11% compound annual growth rate (CAGR) through 2031, maintaining its leadership in the construction silicone sealant market. China's focus on prefabrication and India's expanding aviation sector indicate consistent demand, with coastal provinces consuming over 40% of the nation's sealants. Regional producers with local mixing plants benefit from shorter lead times and preferred status in state projects, creating challenges for import-dependent competitors.

North America is experiencing a shift as office spaces convert to residential use, altering urban landscapes. Vacancy rates improved in 2025, and rising fit-out costs have driven demand for premium, durable materials, reducing the need for frequent resealing. Additionally, federal energy performance mandates for government buildings are directing retrofit investments into high-performance silicone joints, ensuring stable demand even as new construction levels off.

In Europe, regulatory frameworks play a more significant role than new construction. The Corporate Sustainability Reporting Directive (CSRD) and the Energy Performance of Buildings Directive (EPBD) are driving procurement toward low-volatile organic compound (VOC), carbon-verified products, while suppliers with traceable supply chains gain pricing advantages. Although macroeconomic growth remains slow, retrofitting aging social housing is increasing demand for cladding and insulation joints. South America and the Middle East-Africa, while smaller markets, are showing rapid growth. Airports such as Dubai's Al Maktoum and Riyadh's King Salman are expected to utilize millions of linear meters of UV-stable sealants designed for arid climates. NEOM's mirrored facades are setting new technical requirements, including sand-erosion resistance and optical clarity at ambient temperatures of 45 °C.

- 3M

- Arkema

- Beijing Zhongtian

- CHEMENCE

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Mapei

- Momentive

- Pecora Corporation

- Pidilite Industries Ltd.

- RPM International, Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand From Residential and Commercial Construction

- 4.2.2 Growing Use in Green Buildings and Sustainable Architecture

- 4.2.3 Infrastructure Boom in Emerging Economies

- 4.2.4 Excellent Weatherability and Durability of Silicone Sealants

- 4.2.5 Adoption of High-movement Sealants for 3-D-printed Building Facades

- 4.3 Market Restraints

- 4.3.1 Volatility in Silicone and Additive Raw-material Prices

- 4.3.2 Availability of Acrylic, Polysulfide, and Polyurethane Substitutes

- 4.3.3 Regulatory Pressure on VOC and Tin-catalyst Formulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Neutral-cure silicone sealants

- 5.1.2 Acetoxy-cure silicone sealants

- 5.1.3 Oxime-cure silicone sealants

- 5.1.4 Alkoxy-cure silicone sealants

- 5.2 By Application

- 5.2.1 Joint sealing (expansion and movement joints)

- 5.2.2 Glazing and weatherproofing

- 5.2.3 Insulation and cladding

- 5.2.4 Kitchen and sanitary

- 5.2.5 Fire-resistant applications

- 5.2.6 Other Applications (sound-proofing, electrical, etc.)

- 5.3 By End-user

- 5.3.1 Residential construction

- 5.3.2 Commercial construction

- 5.3.3 Industrial construction

- 5.3.4 Infrastructure (bridges, roads, airports)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beijing Zhongtian

- 6.4.4 CHEMENCE

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 Mapei

- 6.4.9 Momentive

- 6.4.10 Pecora Corporation

- 6.4.11 Pidilite Industries Ltd.

- 6.4.12 RPM International, Inc.

- 6.4.13 Shin-Etsu Chemical Co., Ltd.

- 6.4.14 Sika AG

- 6.4.15 Soudal Group

- 6.4.16 Tremco

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growth Potential in Prefabricated and Modular Construction