PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062271

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062271

Self-testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031)

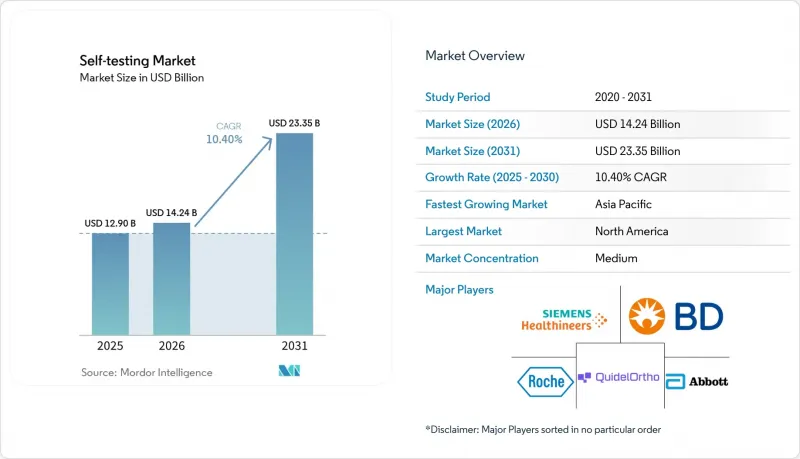

According to Mordor Intelligence, the self-testing market size is expected to grow from USD 12.90 billion in 2025 to USD 14.24 billion in 2026 and is forecast to reach USD 23.35 billion by 2031 at 10.40% CAGR over 2026-2031.

This report is Segmented by Test Type (Blood Glucose Tests, Pregnancy & Fertility Tests, and More), Sample Type (Blood, Urine, Saliva, and More), Distribution Channel (Retail Pharmacies & Drug Stores, Online Pharmacies & DTC Websites, Supermarkets/Hypermarkets, and More), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Self-testing Market Trends and Insights

Explosion of Post-COVID Consumer Acceptance of Home Diagnostics

Sustained behavioral change following pandemic lockdowns keeps home testing the preferred first step for everyday health queries. Over-the-counter antigen kits familiarized households with sample collection, and satisfaction scores from hospital-at-home programs remain high, prompting health systems to expand remote-first care pathways. Connected lateral-flow readers now transmit time-stamped results to clinicians, supporting prescription workflows without in-person visits. Medicare billing codes for remote monitoring reinforce physician adoption, and major pharmacy chains curate dedicated aisles for multi-condition self-tests. These shifts anchor recurring demand across metabolic, infectious, and hormonal panels.

Rising Diabetes & Chronic-Disease Burden Prompting Frequent Self-Monitoring

Global escalation of type 2 diabetes creates continuous need for finger-stick glucose strips and emerging continuous glucose monitors (CGMs). Abbott's Lingo sensor targets an expanding pre-diabetic population that seeks lifestyle guidance rather than insulin titration. Beyond glycemia, at-home lipid, renal and coagulation kits support proactive management of cardiovascular and renal conditions. Population aging amplifies multi-morbidities, and clinical guidelines increasingly endorse patient-initiated testing between clinic visits, sustaining long-term volume growth.

Accuracy & False-Negative Concerns Limiting Clinical Adoption

Sensitivity gaps between home antigen kits and centralized PCR assays prompt clinician requests for confirmatory testing, prolonging diagnostic pathways and dampening full substitution. Pre-analytic errors-such as insufficient sample volume-represent the majority of discrepancies, yet user education materials remain inconsistent. While regulatory post-market surveillance captures serious adverse events, real-world nuisance errors continue to erode physician confidence, particularly for complex multi-analyte panels.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Relaxation for OTC/At-Home Test Approvals in Key Markets

- Smartphone-Linked LFA Readers Enabling Tele-Consult Billing

- Fragmented Reimbursement & Regulatory Complexity Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood-glucose kits captured 41.8% of 2025 revenue, making them the largest contributor to the self-testing market size. Strong insurance coverage, embedded care guidelines and continuous innovation-ranging from micro-sampling strips to factory-calibrated CGMs-consolidate this lead. Digital platforms now overlay behavior-change nudges, shifting value from consumables to data services.

Growing consumer appetite for ancestry and health-trait insights propels genetic self-tests at an 11.8% CAGR, the fastest pace among all panels. Lower sequencing costs allow multi-gene reporting, and saliva collection simplifies logistics. Industry partnerships with oncology networks position hereditary cancer screens for mainstream pharmacy shelves, signaling further share expansion within the self-testing market. Steady pregnancy-test turnover, a relaunch of respiratory panels targeting RSV and flu, and cholesterol kits leveraging smartphone colorimetry round out the menu. Each category benefits from retail brand diversification, yet none rival the scale of glucose in present-day sales.

Geography Analysis

North America's 49.7% revenue share derives from reimbursement alignment for chronic-disease supplies, early adoption of telehealth billing, and high smartphone ownership that facilitates connected diagnostics. FDA clearances of OTC syphilis and combo flu/COVID-19 kits underscore regulatory agility, while payer policy endorsements for remote physiologic monitoring codes underpin usage continuity.

The Asia Pacific self-testing market is projected to expand at 12.8% CAGR through 2031, outpacing all regions. Urban middle-class growth intersects with national e-health blueprints that incentivize remote diagnostics to combat physician shortages. Governments in Japan, South Korea, and Australia grant accelerated review to telehealth-linked tests, and rising digital-wallet penetration eases direct-to-consumer sales. Supply-chain localization initiatives further reduce import dependency, spurring domestic manufacturing investments.

Europe holds meaningful volume but confronts fragmented reimbursement. While the In Vitro Diagnostics Regulation harmonizes safety standards, individual payer debates over cost-effectiveness prolong country-by-country launches. Green-procurement rules, however, position the region as a leader in sustainability-driven product redesign.

Latin America, the Middle East and Africa collectively advance from low bases. Pilot programs in Brazil and Saudi Arabia couple rapid antigen tests with tele-consult stalls inside pharmacies, illustrating localized innovation. Yet limited insurance coverage and import tariffs temper acceleration, leaving multinational corporations to pursue phased rollouts aligned with economic modernization efforts.

- Abbott Laboratories

- Roche

- Siemens Healthineers

- QuidelOrtho

- Beckton Dickinson

- Thermo Fisher Scientific

- Danaher Corp. (Cepheid)

- Bio-Rad Laboratories

- Orasure Technologies

- Everlywell Inc.

- LetsGetChecked

- Cue Health

- Acon Laboratories

- Access Bio

- Mylab Discovery Solutions

- Arkray

- Bionime

- Genomex (23andMe)

- Chembio Diagnostics

- Binx Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion Of Post-COVID Consumer Acceptance Of Home Diagnostics

- 4.2.2 Rising Diabetes & Chronic-Disease Burden Prompting Frequent Self-Monitoring

- 4.2.3 Regulatory Relaxation For OTC/At-Home Test Approvals In Key Markets

- 4.2.4 Smartphone-Linked LFA Readers Enabling Tele-Consult Billing

- 4.2.5 Employer-Sponsored Wellness Testing Programs Expanding Access

- 4.2.6 Self-Collected Specimens Driving Faster Antiviral Prescriptions Via Telehealth

- 4.3 Market Restraints

- 4.3.1 Accuracy & False-Negative Concerns Limiting Clinical Adoption

- 4.3.2 Fragmented Reimbursement & Regulatory Complexity Across Regions

- 4.3.3 Data-Privacy Risks From Cloud-Connected Home Tests

- 4.3.4 Environmental Waste From Single-Use Plastic Test Kits

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Test Type

- 5.1.1 Blood Glucose Tests

- 5.1.2 Pregnancy & Fertility Tests

- 5.1.3 Infectious Disease Tests (HIV, COVID-19, Flu, etc.)

- 5.1.4 Cholesterol & Lipid Tests

- 5.1.5 Genetic & Ancestry Tests

- 5.2 By Sample Type

- 5.2.1 Blood

- 5.2.2 Urine

- 5.2.3 Saliva

- 5.2.4 Nasal / Throat Swab

- 5.2.5 Other Specimens (Stool, Hair, etc.)

- 5.3 By Distribution Channel

- 5.3.1 Retail Pharmacies & Drug Stores

- 5.3.2 Online Pharmacies & DTC Websites

- 5.3.3 Supermarkets / Hypermarkets

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Siemens Healthineers

- 6.3.4 QuidelOrtho Corporation

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 Thermo Fisher Scientific Inc.

- 6.3.7 Danaher Corp. (Cepheid)

- 6.3.8 Bio-Rad Laboratories

- 6.3.9 OraSure Technologies

- 6.3.10 Everlywell Inc.

- 6.3.11 LetsGetChecked

- 6.3.12 Cue Health Inc.

- 6.3.13 ACON Laboratories

- 6.3.14 Access Bio Inc.

- 6.3.15 Mylab Discovery Solutions

- 6.3.16 ARKRAY Inc.

- 6.3.17 Bionime Corporation

- 6.3.18 Genomex (23andMe)

- 6.3.19 Chembio Diagnostics

- 6.3.20 Binx Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment