PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062315

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062315

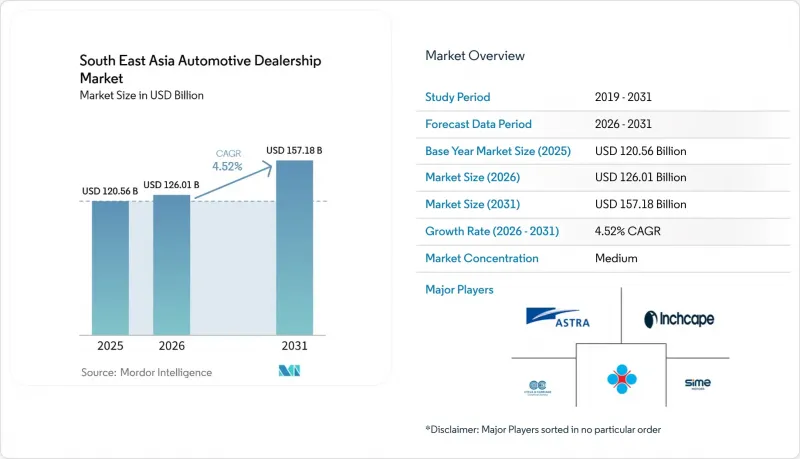

South East Asia Automotive Dealership - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the southeast asia automotive dealership market size is expected to grow from USD 120.56 billion in 2025 to USD 126.01 billion in 2026 and is forecast to reach USD 157.18 billion by 2031, advancing at a 4.52% CAGR during the forecast period (2026-2031).

This report is Segmented by Type (New-Vehicle Dealership, Used-Vehicle Dealership, Parts and Service, and More), Retailer (Franchised Retailer and Non-Franchised Retailer), Vehicle Type (Passenger Cars and More), Propulsion (Internal-Combustion-Engine and Electric Vehicles), and Country (Indonesia, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD).

South East Asia Automotive Dealership Market Trends and Insights

Surging New-Vehicle Demand Across Indonesia, Thailand and Vietnam

Combined new-vehicle registrations across three markets surpassed significant volumes, enabling dealer groups to justify the establishment of new outlets and service bays. Indonesian conglomerate Indomobil is eyeing additional sites to enhance its presence in Jakarta, Bandung, and Surabaya. Meanwhile, Vietnam's THACO is setting up rural showrooms to make maintenance services more convenient for customers. In Thailand, robust commercial vehicle pipelines are bolstered by public infrastructure spending, which in turn fuels demand for light trucks. Dealer financiers are enticing first-time buyers-who had delayed purchases during the pandemic-with bundled low-down-payment offers and manufacturer cash rebates. These combined factors not only bolster foot traffic but also highlight the growing influence of online configurators in the early stages of vehicle consideration.

Rapid Digital Retailing and Omnichannel Buying Journeys

Consumers now expect price transparency, virtual vehicle walk-arounds, and at-home test drives, pushing the Southeast Asia automotive dealership market toward full inventory visibility across apps and showroom tablets. Toyota Philippines' end-to-end SAP rollout reduces quotation time and synchronizes parts availability, boosting conversion rates and service retention. Partnerships such as GAC-Grab fold ride-hailing data into cockpit interfaces, hinting at future subscription revenue for dealers that manage fleet uptime. VinFast's web portal allows 90% financing approvals within minutes, raising the competitive bar on loan processing speed. Dealers embracing click-to-buy funnels can capture browsing signals that guide stocking decisions, whereas legacy outlets reliant on walk-ins lose share to digitally native rivals .

High Capex and Working-Capital Needs for Multi-Brand Showrooms

Flagship outlets integrating EV chargers, digital screens, and certified workshops can top USD 10 million, stretching dealer leverage ratios. Perodua's capital plan underscores the unpredictable nature of cash outflows, especially when investments in production, retail, and services converge. As the proliferation of models demands a deeper stock to meet immediate fulfillment expectations, inventory carrying costs inevitably escalate. Small independent entities, lacking OEM co-investment programs, frequently merge into larger groups, hastening consolidation. Meanwhile, access to green financing and vendor-managed inventory programs emerges as a key differentiator, influencing the speed of network expansion.

Other drivers and restraints analyzed in the detailed report include:

- After-Sales Expansion by OEM-Backed Dealer Groups

- Booming Pre-Owned Vehicle Platforms and Classifieds

- Direct-to-Consumer Online Sales Pilots by Global OEMs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Southeast Asia automotive dealership market size for new-vehicle outlets accounted for 55.33% in 2025 and is projected to grow at a 6.12% CAGR to 2031. OEMs prioritize these channels for EV rollouts, offering co-funded charger installations that reduce payback periods. BMW's new store in Jakarta features digital configurators and lounge spaces, enhancing the brand's storytelling. As battery-electric vehicles gain popularity, inventory is shifting toward models with higher gross margins. This adjustment helps mitigate the downward pressure caused by online price transparency.

Used-vehicle operations, though fragmented, remain a profitable market. Platforms are utilizing AI for valuations to expand beyond traditional physical lot capacities. Dealer groups are also partnering with insurers to offer bundled extended warranties. Finance and insurance products tied to pre-owned purchases generate additional yield, offsetting narrower profit margins on vehicle sales. Additionally, new-vehicle dealers are increasingly operating adjacent certified lots. This approach enables them to quickly recycle trade-ins, reducing the risk of losing sales to independent e-commerce marketplaces.

Franchised retailers accounted for 64.47% of the Southeast Asia automotive dealership market share in 2025 and are projected to grow at a 6.21% CAGR through 2031, underscoring OEM commitment to brand-compliant environments that host EV chargers and software update zones. Multi-brand halls lower per-brand capex, and regional conglomerates leverage centralized parts warehouses to support dozens of badges with leaner inventory. Digital integration lets customers transition from the website to the showroom to the service bay under a single sign-on, bolstering retention rates.

Independent dealers excel in agility and price competition, particularly in the used-car arena. Carsome's profitability milestone is pressuring franchised operators to match its seven-day buyback guarantees. Non-aligned outlets often pivot to niche imports or performance models excluded from franchised catalogs. As agency sales models spread, franchised groups may morph into service-centric businesses, charging OEMs for handover and maintenance while ceding transactional control.

List of Companies Covered in this Report:

- PT Astra International Tbk

- Sime Darby Motors

- Cycle and Carriage (Jardine Matheson)

- Tan Chong Motor Holdings Berhad

- Inchcape plc

- Naza Automotive Group

- PT Indomobil Sukses Internasional Tbk

- Hasjrat Abadi

- VinFast Trading and Production

- Truong Hai Auto (THACO)

- TC Subaru (Singapore)

- Honda Cars Thailand

- Bermaz Auto Berhad

- UMW Toyota Motor Malaysia

- United Tractors Indonesia

- Berjaya Auto Philippines

- Motor Image Enterprises

- Boon Siew Honda Malaysia

- MBM Resources Berhad

- Vinacar (Philippines)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging New-Vehicle Demand Across Indonesia, Thailand and Vietnam

- 4.2.2 Rapid Digital Retailing and Omnichannel Buying Journeys

- 4.2.3 After-Sales (Parts and Service) Expansion By OEM-Backed Dealer Groups

- 4.2.4 Booming Pre-Owned Vehicle Platforms and Classifieds

- 4.2.5 EV-Exclusive Dealership Formats Encouraged by Government Incentives

- 4.2.6 ASEAN Grey-Market Liberalisation for Used-Vehicle Cross-Border Flows

- 4.3 Market Restraints

- 4.3.1 High Capex and Working-Capital Needs for Multi-Brand Showrooms

- 4.3.2 Direct-To-Consumer Online Sales Pilots by Global Oems

- 4.3.3 Import Quota / Tariff Uncertainty for Used Cars in Malaysia and Thailand

- 4.3.4 Shortage Of Certified EV Technicians and Diagnostic Tooling

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 New-Vehicle Dealership

- 5.1.2 Used-Vehicle Dealership

- 5.1.3 Parts and Service

- 5.1.4 Finance and Insurance

- 5.2 By Retailer

- 5.2.1 Franchised Retailer

- 5.2.2 Non-franchised Retailer

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Two-Wheelers

- 5.4 By Propulsion

- 5.4.1 Internal-Combustion-Engine Vehicles

- 5.4.2 Electric Vehicles

- 5.5 By Country

- 5.5.1 Indonesia

- 5.5.2 Thailand

- 5.5.3 Malaysia

- 5.5.4 Philippines

- 5.5.5 Vietnam

- 5.5.6 Singapore

- 5.5.7 Rest of South East Asia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PT Astra International Tbk

- 6.4.2 Sime Darby Motors

- 6.4.3 Cycle and Carriage (Jardine Matheson)

- 6.4.4 Tan Chong Motor Holdings Berhad

- 6.4.5 Inchcape plc

- 6.4.6 Naza Automotive Group

- 6.4.7 PT Indomobil Sukses Internasional Tbk

- 6.4.8 Hasjrat Abadi

- 6.4.9 VinFast Trading and Production

- 6.4.10 Truong Hai Auto (THACO)

- 6.4.11 TC Subaru (Singapore)

- 6.4.12 Honda Cars Thailand

- 6.4.13 Bermaz Auto Berhad

- 6.4.14 UMW Toyota Motor Malaysia

- 6.4.15 United Tractors Indonesia

- 6.4.16 Berjaya Auto Philippines

- 6.4.17 Motor Image Enterprises

- 6.4.18 Boon Siew Honda Malaysia

- 6.4.19 MBM Resources Berhad

- 6.4.20 Vinacar (Philippines)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment