PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062327

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062327

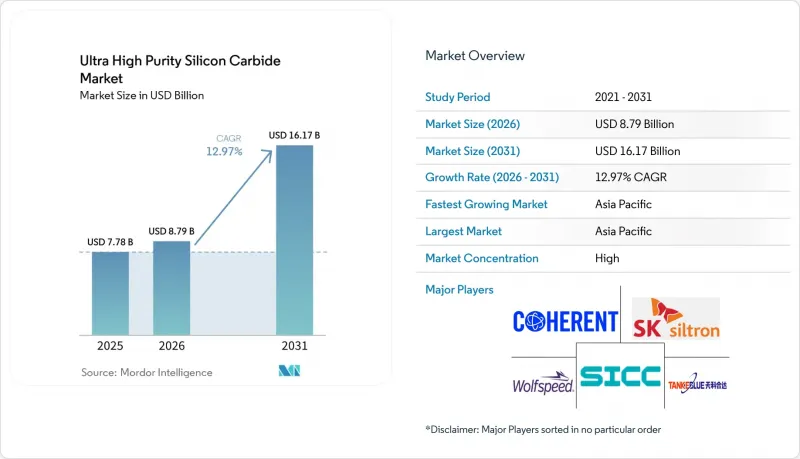

Ultra High Purity Silicon Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the ultra high purity silicon carbide market size was valued at USD 7.78 billion in 2025 and is estimated to grow from USD 8.79 billion in 2026 to reach USD 16.17 billion by 2031, at a CAGR of 12.97% during the forecast period (2026-2031).

This report is Segmented by Purity Level (Greater Than 99. 9999% (6N), Greater Than 99. 999% (5N), and More), Form (Powder, and More), Application (Power Electronics, and More), End-User Industry (Automotive, Renewable Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Ultra High Purity Silicon Carbide Market Trends and Insights

EV Traction Inverters and On-Board Chargers

Automakers have standardized SiC MOSFETs in traction inverters to unlock 5%-10% efficiency gains over silicon, extending driving range without enlarging the battery pack. Junction temperatures up to 200°C halve the cooling-system mass and allow inverters to be integrated within the e-motor housing. Lifetime revenue contracts exceeding USD 1 billion between Onsemi and BorgWarner underscore mainstream adoption. Three-phase 22 kW on-board chargers now exploit SiC's high-frequency switching to shrink magnetics by 40%, a key win as battery capacities exceed 100 kWh. China surpassed 1.2 million 800-V EVs in 2025, and SiC captured more than 80% of their inverters, creating a resilient demand floor.

Grid-Scale and Commercial Solar Inverters

SiC topologies yield 99.1% peak efficiency versus 98.0% for silicon, an absolute 1-point gain that equates to an extra 600 MW annually per 60 GW of installations. Fraunhofer's 250 kW demo cut inverter volume by 40%, enabling rooftop deployments on weight-limited structures. Higher efficiency shortens payback by up to nine months in high-irradiance regions, spurring adoption in India and the Middle East. The EU-funded SiC4GRID project earmarked EUR 15 million (USD 16.96 million) for medium-voltage converters that will debut on North Sea wind farms in 2027. Kaco's 100 kW and 125 kW SiC products already lead the fast-growing distributed-generation niche.

High Purification and Crystal-Growth Cost

Each 200 mm boule requires 7-10 days of physical-vapor transport at 2,300°C, consuming as much as 20 MWh and expensive ultra-pure argon. The resulting USD 400-USD 600 substrate contrasts with USD 50-USD 80 silicon, a 5X-10X penalty. Epitaxy adds another USD 150-USD 200 per wafer. Chinese suppliers cut prices 40% between 2023 and 2025 through scale and cheaper labor, pressuring incumbents to accelerate 300 mm transitions.

Other drivers and restraints analyzed in the detailed report include:

- Demand Spike from 800 V Vehicle Architectures

- Government On-Shoring Incentives for SiC Fabs

- Limited Ultra-Pure Feedstock Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The greater than 99.99999% (7 N+) segment is poised for a 13.68% CAGR during the forecast period (2026-2031), eclipsing the greater than 99.9999% (6 N) tier that dominated 48.04% of Ultra High Purity Silicon Carbide market share in 2025. Demand comes from 1,200 V and 1,700 V automotive inverters and 3,300 V solar converters that mandate sub-1 ppb impurity levels. Infineon's CoolSiC Gen2 relies exclusively on 7N+ substrates, while Coherent rolled out thick-epitaxy 7N+ wafers aimed at 10 kV AI-datacenter power modules. Although 5N material maintains a niche in legacy LED and abrasive uses, device makers are locking in 7N+ supply contracts to future-proof high-voltage roadmaps.

Cost sensitivity keeps 6N substrates relevant for mainstream 650 V-1,200 V EV traction applications. ROHM's 5th-generation MOSFET achieves 1.0 mΩ on-resistance on a 7 mm X 7 mm die using 6N, satisfying thermal budgets up to 175°C. Long term, yield improvements and larger wafer diameters are expected to narrow the cost delta, accelerating 7N+ adoption even in mid-voltage classes.

Epitaxial 4-inch wafers still held 45.06% of the Ultra High Purity Silicon Carbide market size in 2025, but 6-inch and 8-inch formats are stealing share as capital budgets shift to 200 mm lines. Resonac's third-generation HGE-3G epi wafers entered mass production in 2023, and the firm shipped its first 200 mm volumes in 2025. Powder, primarily for abrasives and ceramics, remains a low-growth adjunct.

Bulk crystal output is forecast to grow at 13.92% as Integrated Device Manufacturers (IDMs) bring substrate fabrication in-house. STMicroelectronics' EUR 5 billion (USD 5.65 billion) Catania campus exemplifies the powder-to-module model, targeting 15,000 wafers per week by 2033. Denso's joint venture with Fuji Electric will supply 310,000 wafers annually to Toyota by 2027, underscoring OEM appetite for captive crystal capacity.

Geography Analysis

Asia-Pacific generated 52.67% of 2025 revenue and is on course for a 14.09% CAGR during the forecast period (2026-2031). Japan allocated JPY 350.3 billion (USD 2.4 billion) in subsidies to reinforce domestic SiC supply lines, and China's TankeBlue plus SICC jointly stepped up to a significant share of global substrate output by undercutting prices. South Korea aims for 20% SiC self-sufficiency, backstopping SK Siltron CSS with federal and Michigan incentives to multiply 200 mm capacity tenfold by 2027. India remains confined to device packaging, while Malaysia's Kulim hub hosts Infineon's scaling 200 mm fab.

North America benefits from the CHIPS Act's USD 750 million grant to Wolfspeed's Siler City plant, slated to triple domestic capacity by 2030. The United States held the largest share of global substrate production in 2025, but leads in 300 mm research and development. Canada and Mexico are minor assembly nodes. Onsemi's South Korea expansion services North American auto customers, reinforcing bilateral supply security.

Europe consolidates capacity via state-aided megaprojects. STMicroelectronics brought its EUR 5 billion (USD 5.65 billion) Catania campus online in 2025, and Infineon's Dresden Smart Power Fab received EUR 1 billion (USD 1.65 billion) in EU funds. Onsemi is building Europe's first fully integrated SiC line in the Czech Republic. ROHM's SiCrystal will triple its German capacity by 2027. The U.K. and France contribute design expertise but modest wafer volumes.

South America and the Middle East & Africa remain the lowest contributors, focused on downstream renewable projects rather than upstream substrate manufacturing. Brazil's EV programs import SiC devices, and the Middle East's 50 GW solar pipeline should lift inverter demand, but neither region has announced high-purity boule capacity.

- 5N Plus

- Coherent Corp.

- CoorsTek Inc.

- Entegris

- Fujimi Corporation

- Infineon Technologies AG

- Nippon Steel Corporation

- Resonac Holdings Corporation

- ROHM Co., Ltd.

- Semiconductor Components Industries, LLC

- SiCrystal GmbH

- SICC Co., Ltd.

- SK Siltron CSS

- STMicroelectronics

- TankeBlue Co., Ltd.

- Tokai Carbon Co., Ltd.

- Washington Mills

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV traction inverters and on-board chargers

- 4.2.2 Grid-scale and C&I renewable inverters

- 4.2.3 Demand spike from 800 V vehicle architectures

- 4.2.4 Government on-shoring incentives for SiC wafer fabs

- 4.2.5 300 mm SiC boule breakthroughs lifting 7 N yield

- 4.3 Market Restraints

- 4.3.1 High purification and crystal-growth cost

- 4.3.2 Limited ultra-pure feed-stock availability

- 4.3.3 Wafer yield losses from basal-plane dislocations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Purity Level

- 5.1.1 greater than 99.999% (5 N)

- 5.1.2 greater than 99.9999% (6 N)

- 5.1.3 greater than 99.99999% (7 N+)

- 5.2 By Form

- 5.2.1 Bulk Crystal

- 5.2.2 Epitaxial Wafer (4-inch)

- 5.2.3 Epitaxial Wafer (6- and 8-inch)

- 5.2.4 Powder

- 5.3 By Application

- 5.3.1 Power Electronics

- 5.3.2 Semiconductors (Discrete and IC)

- 5.3.3 LEDs and Optoelectronics

- 5.3.4 Photovoltaics

- 5.3.5 Advanced Ceramics and Others

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Renewable Energy

- 5.4.3 Telecommunications and 5G

- 5.4.4 Consumer Electronics

- 5.4.5 Defense and Aerospace

- 5.4.6 Industrial and Others

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 5N Plus

- 6.4.2 Coherent Corp.

- 6.4.3 CoorsTek Inc.

- 6.4.4 Entegris

- 6.4.5 Fujimi Corporation

- 6.4.6 Infineon Technologies AG

- 6.4.7 Nippon Steel Corporation

- 6.4.8 Resonac Holdings Corporation

- 6.4.9 ROHM Co., Ltd.

- 6.4.10 Semiconductor Components Industries, LLC

- 6.4.11 SiCrystal GmbH

- 6.4.12 SICC Co., Ltd.

- 6.4.13 SK Siltron CSS

- 6.4.14 STMicroelectronics

- 6.4.15 TankeBlue Co., Ltd.

- 6.4.16 Tokai Carbon Co., Ltd.

- 6.4.17 Washington Mills

- 6.4.18 Wolfspeed, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment