PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062351

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062351

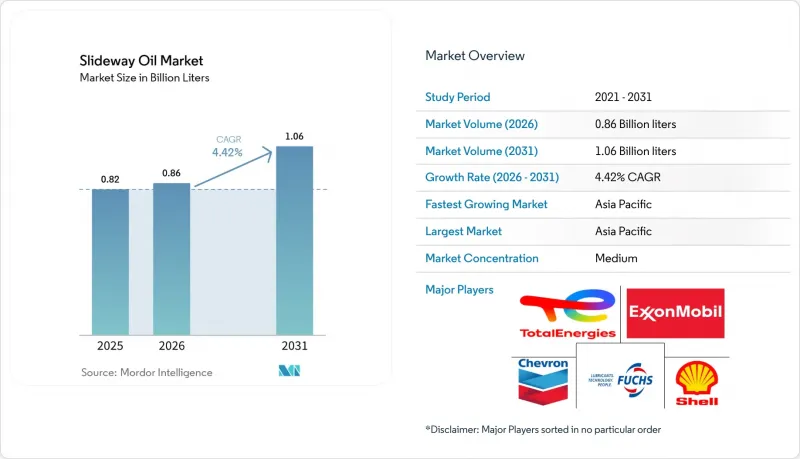

Slideway Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the slideway oil market size was valued at 0.82 Billion liters in 2025 and is estimated to grow from 0.86 Billion liters in 2026 to reach 1.06 Billion liters by 2031, at a CAGR of 4.42% during the forecast period (2026-2031).

This report is Segmented by Base Oil (Mineral Oil-Based, Synthetic Oil-Based, and Bio-Based), Application (CNC Machines, Horizontal Slideways, Vertical Slideways, and More), End-User Industry (Metalworking Heavy Equipment and Machining, Automotive and Auto Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Liters).

Global Slideway Oil Market Trends and Insights

Expanding Precision Machining and CNC Penetration

China shipped 700,000 machine-tool units in 2024, setting a benchmark for future lubricant volumes as each new five-axis center requires low-migration slideway oil. FANUC's USD 1.2 billion Chongqing expansion and TRUMPF's Connecticut smart factory highlight similar growth trends in North America, reflecting the global demand for high-accuracy beds with closed-loop lubrication systems compatible with automated pallet changers. The increasing adoption of compact CNC lathes in Vietnam and Indonesia is further expanding the installed base, boosting replacement consumption, and encouraging suppliers to introduce synthetic-ester blends that extend drain intervals by 30-40%.

Accelerating Metal-Working Output in Emerging Economies

India's INR 100 billion machine-tool production and Mexico's USD 36 billion in nearshoring inflows are driving demand for slideway oils that ensure reliable film formation in humid, high-temperature environments. At the same time, China's CNY 30.8 trillion machinery industry continues to rely on demulsifying formulations that prevent sump contamination in shared-fluid CNC cells. Suppliers offering oil-analysis services alongside product sales are securing multi-year maintenance contracts, insulating themselves from spot-price competition.

Crude-Linked Volatility in Base-Oil Prices

In the fourth quarter of 2025, the U.S. Producer Price Index for lubricants reached its lowest level since 2021. However, unplanned outages in the Middle-East subsequently tightened supply and drove up spot prices, squeezing margins for formulators without hedging programs. A 10% fluctuation in Brent crude prices translates to a 6-8% shift in base-oil costs, prompting Sinopec to invest in a 30,000 tpa metallocene PAO plant to reduce reliance on crude benchmarks for premium supply.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Investments in Automated Tool Rooms

- Tightening VOC-Emission Rules Favoring Bio-Based Slideway Fluids

- Chemical Incompatibility with Water-Miscible Metalworking Fluids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oil-based represented 55.89% of the slideway oil market share in 2025, with synthetic PAO and ester blends serving high-temperature applications. The bio-based segment is anticipated to grow at a CAGR of 5.16% through 2031, surpassing all other base oil categories. Products such as Shell PANOLIN and TotalEnergies BIOHYDRAN illustrate that certified biodegradable oils can maintain extreme-pressure performance while reducing CO2 life-cycle emissions by up to 84%.

Nevertheless, high feedstock costs and the limited availability of HEES-certified fluids above ISO VG 320 hinder adoption in heavy-duty vertical slideways. Expanding the production of epoxidized-soybean and tall-oil esters could help bridge the price gap with Group II mineral oils by 2029.

Geography Analysis

Asia-Pacific accounted for 47.57% of the slideway oil market share in 2025 and is projected to grow at a CAGR of 5.23% through 2031, supported by China's machine-tool production of 700,000 units and India's growing export machining clusters. North America benefits from USD 239 billion in U.S. manufacturing construction, with EPA Risk Management Plan revisions encouraging the adoption of bio-based products. Europe, while facing mixed machine-tool order volumes, leads in regulatory advancements, positioning it as a hub for PFAS-free innovations. The Middle-East and Africa, though starting from a smaller base, are attracting tailored solutions through partnerships like Quaker Houghton-Petrolube, which localizes blending for high-temperature environments.

- Blaser Swisslube AG

- BP p.l.c.

- Chem Arrow Corporation

- Chevron Corporation

- ENEOS Corporation

- Exxon Mobil Corporation

- FUCHS

- Kluber Lubrication SE

- LUKOIL

- MotulTech (Motul SA)

- Petro-Canada Lubricants Inc.

- PETRONAS Lubricants International

- PT Idemitsu Lube Techno Indonesia

- Quaker Houghton

- Shell plc

- Sinopec Lubricants Co.

- TotalEnergies

- Valvoline Global Operations

- Yushiro Chemical Industry Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding precision machining and CNC penetration

- 4.2.2 Accelerating metal-working output in emerging economies

- 4.2.3 Industry 4.0 investments in automated tool rooms

- 4.2.4 Surge in retrofit/maintenance of ageing slideway beds

- 4.2.5 Tightening VOC-emission rules favouring bio-based slideway fluids

- 4.2.6 IIoT-enabled "smart-lubrication" demand for condition-based dosing

- 4.3 Market Restraints

- 4.3.1 Crude-linked volatility in base-oil prices

- 4.3.2 Chemical incompatibility with water-miscible metal-working fluids

- 4.3.3 Stringent disposal and REACH/EPA compliance costs

- 4.3.4 Adoption of dry/self-lubricating linear-motion polymers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Base Oil

- 5.1.1 Mineral oil-based

- 5.1.2 Synthetic oil-based

- 5.1.3 Bio-based

- 5.2 By Application

- 5.2.1 CNC Machines

- 5.2.2 Horizontal Slideways

- 5.2.3 Vertical Slideways

- 5.2.4 Grinders

- 5.2.5 Lathes

- 5.2.6 Other Applications (clean-room tools, etc.)

- 5.3 By End-user Industry

- 5.3.1 Metalworking, Heavy Equipment and Machining

- 5.3.2 Automotive and Auto Components

- 5.3.3 Aerospace and Defense

- 5.3.4 Marine and Rail

- 5.3.5 Other Industries (Electronics, Energy and Power)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Blaser Swisslube AG

- 6.4.2 BP p.l.c.

- 6.4.3 Chem Arrow Corporation

- 6.4.4 Chevron Corporation

- 6.4.5 ENEOS Corporation

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Kluber Lubrication SE

- 6.4.9 LUKOIL

- 6.4.10 MotulTech (Motul SA)

- 6.4.11 Petro-Canada Lubricants Inc.

- 6.4.12 PETRONAS Lubricants International

- 6.4.13 PT Idemitsu Lube Techno Indonesia

- 6.4.14 Quaker Houghton

- 6.4.15 Shell plc

- 6.4.16 Sinopec Lubricants Co.

- 6.4.17 TotalEnergies

- 6.4.18 Valvoline Global Operations

- 6.4.19 Yushiro Chemical Industry Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment