PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062363

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062363

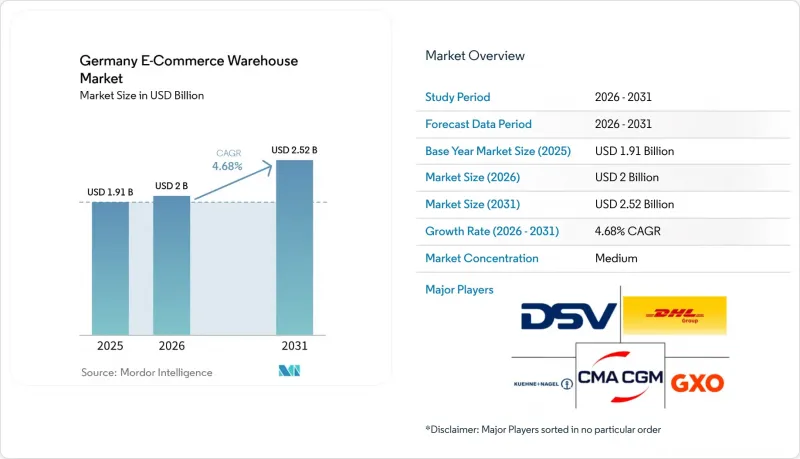

Germany E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany e-commerce warehouse market size is expected to grow from USD 1.91 billion in 2025 to USD 2.00 billion in 2026 and is forecast to reach USD 2.52 billion by 2031 at 4.68% CAGR over 2026-2031.

An investment shift toward automation retrofits, multi-temperature capabilities, and vertical expansions is redefining capacity planning as operators favor density over new footprints. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, and More), by Service Type (Storage, Picking and Packing, and More), by Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel and Footwear, Consumer Electronics, and More), and by Geography (North Rhine-Westphalia, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany E-Commerce Warehouse Market Trends and Insights

Booming Cross-Border EU E-Commerce Flows

Germany's central geography and Rhine-Alpine corridor connectivity make it the preferred consolidation point for pan-European e-commerce. Operators deploy customs-bonded zones that defer duties until final delivery, lowering working-capital exposure for merchants. DHL's 1 million-parcel-per-day hub in nearby Poznan exemplifies network extensions that knit German and Eastern European facilities into a single fulfillment mesh. Growth in multi-currency invoicing, localized packaging, and VAT-compliant documentation strengthens demand for value-added services, while multilingual labor pools and in-house brokerage expertise emerge as competitive moats.

Acceleration of Online Grocery & Q-Commerce Demand

Online grocery sales are on track to hit EUR 18 billion (USD 20.6 billion) by 2030 as penetration climbs to 17% of food outlays. REWE's EUR 250 million (USD 286 million) Magdeburg hub processes 286,000 packages daily with 50% automation, showing the capital intensity of multi-temperature fulfillment. Quick-commerce brands place micro-fulfillment nodes within 3-5 km of customers, compressing delivery windows below 60 minutes. Multi-zone storage grids that integrate ambient, chilled, and frozen SKUs inside the same automation framework are becoming standard, allowing high-velocity SKU handling without capacity trade-offs.

Electric-Grid Capacity Bottlenecks for High-Power Automation

Robotic systems typically consume 3-5 MW of continuous power, frequently surpassing the spare capacity of local substations. This high energy demand often creates significant challenges for infrastructure readiness. With connection queues stretching up to 18 months, rollouts face delays, nudging operators towards phased deployments or temporary semi-automated solutions to maintain operational continuity. The scale of necessary upgrades is underscored by partnerships with utilities, exemplified by DHL-E.ON's DC electrification program, which highlights the critical need for modernized energy infrastructure to support advanced robotic systems.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Subscription/Auto-Replenishment Commerce

- Omni-channel Inventory Consolidation by Legacy Retailers

- Rising Cybersecurity Threats to Warehouse OT Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfilment centers held 52.94% of the Germany e-commerce warehouse market size in 2025, reflecting their versatility across product categories and order profiles. Dark Stores and micro-fulfilment centers, however, post a brisk 9.1% CAGR through 2031 as quick-commerce players require inventory within minutes of end users. The rise of cold-chain automation brings multi-zone temperature designs to both large fulfilment hubs and compact urban nodes. Distribution centres continue to serve bulk replenishment for legacy retailers, while cold-chain warehouses gain traction among pharma and fresh-food operators. Reverse-logistics hubs and bonded sites populate the others category, offering specialized value propositions like duty-deferred storage and returns processing.

Technical sophistication grows in all formats. Flaschenpost's Langenfeld facility processes 1,000 orders per hour via integrated ambient and chilled AutoStore grids, showcasing how automation harmonizes speed and temperature control. Legacy fulfilment centres reply with modular robotics that flex capacity across seasons, minimizing sunk costs while future-proofing against evolving product mixes. Blurred lines between warehouse types emerge as omni-channel merchants demand spaces able to pivot from bulk pallet moves to single-unit picks with minimal reconfiguration.

Storage remains foundational at 54.11% of 2025 revenue, a function every operator must offer. Yet Value-Added Services grow 7.92% CAGR to 2031 as brands outsource kitting, labeling, and localization to reduce lead times and complexity. Picking and packing, the labor-intensive heart of e-commerce, drives most automation spend because accuracy and speed here translate directly into customer satisfaction. REWE's Magdeburg hub, automated to 50% across storage and pick zones, illustrates how integrated service bundles cut dwell times and curb workforce dependency.

Operators who master regulatory compliance, testing, and light customization create sticky relationships and margin uplifts. AI-enhanced WMS solutions optimize order batching and labor allocation, while robotics shrinks error rates and supports 24/7 peaks. As commoditized storage yields lower margins, diversified service portfolios become decisive in client retention and contract renewals.

List of Companies Covered in this Report:

- DHL Group

- DSV (incl. Schenker)

- Otto Group

- Fiege Logistik

- Rhenus Logistics

- GXO Logistics

- CMA CGM Group (Including CEVA Logistics)

- B+S Logistics

- Kuehne+Nagel

- Arvato Supply Chain Solutions

- Zalando Logistics

- Loxxess AG

- Pfenning Logistics Group

- BLG Logistics Group

- DACHSER

- Hellmann Worldwide Logistics

- GEODIS

- Hermes Fulfilment

- Geis Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming Cross-Border EU E-Commerce Flows

- 4.2.2 Acceleration of Online Grocery and Q-Commerce Demand

- 4.2.3 Surge in Subscription/Auto-Replenishment Commerce

- 4.2.4 Omni-Channel Inventory Consolidation by Legacy Retailers

- 4.2.5 Vertical Automated Mezzanine Retrofits in Existing Sites

- 4.2.6 ESG-Linked Green-Warehouse Financing Incentives

- 4.3 Market Restraints

- 4.3.1 Electric-Grid Capacity Bottlenecks for High-Power Automation

- 4.3.2 Rising Cybersecurity Threats to Warehouse OT Systems

- 4.3.3 Stricter EU Packaging and Waste-Compliance Directives

- 4.3.4 Construction-Material Supply Shocks & Cost Spikes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-Use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking and Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By States - Germany (Value)

- 5.5.1 North Rhine-Westphalia

- 5.5.2 Bavaria (Bayern)

- 5.5.3 Baden-Wurttemberg

- 5.5.4 Rest of States

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 DHL Group

- 6.4.2 DSV (incl. Schenker)

- 6.4.3 Otto Group

- 6.4.4 Fiege Logistik

- 6.4.5 Rhenus Logistics

- 6.4.6 GXO Logistics

- 6.4.7 CMA CGM Group (Including CEVA Logistics)

- 6.4.8 B+S Logistics

- 6.4.9 Kuehne+Nagel

- 6.4.10 Arvato Supply Chain Solutions

- 6.4.11 Zalando Logistics

- 6.4.12 Loxxess AG

- 6.4.13 Pfenning Logistics Group

- 6.4.14 BLG Logistics Group

- 6.4.15 DACHSER

- 6.4.16 Hellmann Worldwide Logistics

- 6.4.17 GEODIS

- 6.4.18 Hermes Fulfilment

- 6.4.19 Geis Group

7 Market Opportunities and Future Outlook