PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062389

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062389

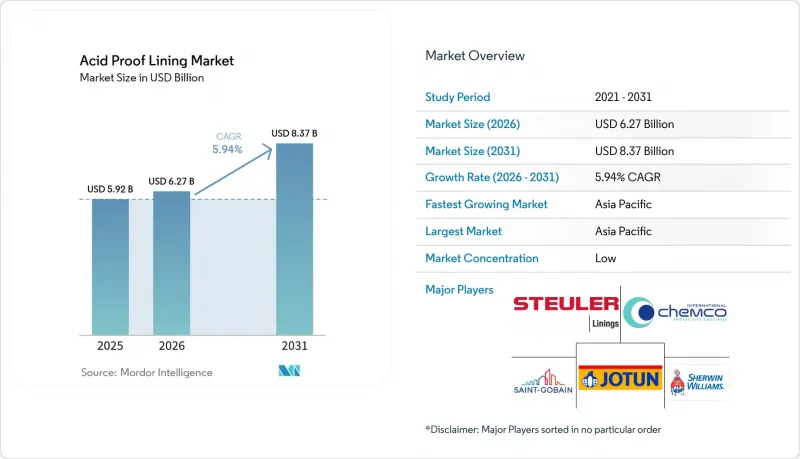

Acid Proof Lining - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the acid proof lining market size is projected to be USD 5.92 billion in 2025, USD 6.27 billion in 2026, and reach USD 8.37 billion by 2031, growing at a CAGR of 5.94% from 2026 to 2031.

This report is Segmented by Material Type (Fiber-Reinforced Polymer Lining, Carbon Brick Lining, and More), Lining Type (Tile Lining, Brick Lining, and More), Application (Tanks and Vessels, Storage and Containment Systems, and More), End-User Industry (Chemical Processing, Fertilizer, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Acid Proof Lining Market Trends and Insights

Rising Corrosion-Resistant Demand in Chemical Processing

Process operators are increasing reaction conditions to boost yield, which accelerates corrosion on legacy carbon-brick systems and drives demand for duplex stainless and high-build glass-flake linings that extend service intervals from 18 months to 5 years. Unplanned shutdowns at large ammonia-urea complexes cost USD 2 million-USD 4 million per day, making durability a direct factor in protecting profit. Procurement tenders now require a minimum 15-year design life and ISO 16276-1:2025 certification, reducing the pool of approved vendors and increasing average bid values. Semiconductor fabs transitioning to 2-nanometer nodes have doubled hydrofluoric-acid exposure, increasing demand for premium PFA and PTFE linings that ensure zero ionic contamination. This has created a bifurcated acid proof lining market: commodity plants opt for cost-efficient vinyl-ester systems, while ultrapure environments pay three-to-five-times premiums for fluoropolymers.

Expansion of Wastewater and Desalination Infrastructure

Municipal and industrial wastewater capacity is expanding across the Asia-Pacific and the Middle-East as governments prioritize water security. Desalination plants expose linings to hypersaline brine, sulfuric-acid dosing, and continuous chlorine injection, conditions that ceramic brick can endure for 30 years with minimal permeation. Polyurea membranes, sprayed at 3 millimeters thickness, cure quickly and reduce downtime on retrofit work by 24 hours per tank, cutting maintenance budgets by 60% over a decade. Failure risk is costly: a single outage at a 500,000 m3-per-day plant triggers USD 1.5 million in water-purchase penalties. Regulatory tightening, such as China's 2025 GB 8978 heavy-metal limits, requires manufacturers to install acid-resistant linings in neutralization vessels to prevent contaminant leaching.

High Installation and Lifecycle Cost

Installed costs range between USD 150 and USD 600 per m2, with specialty fluoropolymers being twenty times more expensive than commodity rubber systems, deterring projects with 3-to-5-year payback periods. Humid environments further increase costs, as meeting Sa2.5 blast standards can account for 40% of total labor hours. Chinese methanol plants in 2026 attracted only three bids on a corrosion-reinforcement tender, indicating that price barriers are reducing the contractor base. Material costs also vary significantly; heavy-duty epoxies priced at CNY 50-150 per kg translate to installed costs of CNY 200-500 per m2 when labor and scaffolding are included.

Other drivers and restraints analyzed in the detailed report include:

- Refurbishment of Aging Industrial Assets

- Tightening Worker-Safety Durability Mandates

- Skilled-Applicator Scarcity and Complex Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber-reinforced polymer (FRP) lining accounted for 33.03% of 2025 revenue, emphasizing its adaptability across temperature ranges from -40 °C to 120 °C and compatibility with a wide range of chemical classes. Carbon brick remains relevant in reactors operating above 200 °C but is labor-intensive to install. Ceramic brick performs well in abrasive slurry applications but increases structural weight by 15%. Rubber continues to dominate in mining applications where impact resistance is critical.

The other materials segment, including epoxy, phenolic, and bio-based options, is projected to grow at a 6.42% CAGR through 2031, driven by a shift away from petroleum-based systems as buyers increasingly prioritize CO2 footprint reductions in procurement decisions. Soy-based Soy-PK epoxy, which achieves tensile strength exceeding 25 MPa and reduces embodied carbon by 40%, is gaining traction in food-grade tank linings. PVC and CPVC remain key materials in pharmaceutical processing due to FDA compliance, but upcoming chlorine restrictions under REACH regulations may impact their medium-term outlook.

Tile linings accounted for 75.75% of 2025 revenue, supported by decades of field data demonstrating 25-year durability in sulfuric and phosphoric acid applications. Brick linings remain relevant in chimney and stack retrofits where refractory properties are essential.

Monolithic linings are expected to grow at a 6.73% CAGR through 2031, driven by the adoption of plural-component spray systems that cure within minutes, enabling 24-hour turnaround times and reducing outage windows by 50%. Glass-flake epoxies, which incorporate up to 40% flake by weight, reduce permeability tenfold compared to standard epoxy and meet ultrapure pharmaceutical standards. Seamless membranes also distribute stress more evenly than grouted tiles, as confirmed by finite-element simulations of cyclic pressure loads in hydrogen reactors.

Geography Analysis

Asia-Pacific contributed 46.27% of global revenue in 2025 and is expected to grow at a 6.92% CAGR through 2031. Growth is supported by China's petrochemical upgrade initiatives, India's fertilizer plant expansions, and Japan's refurbishment projects driven by diagnostic assessments. South Korea and Taiwan's semiconductor industries require HF-resistant containment, while ASEAN's waste-to-energy plants drive demand for FGD linings despite permitting delays.

North America faces challenges from an aging plant infrastructure and labor shortages, which have increased installation costs by up to 35%. U.S. federal funding for water infrastructure is driving demand for wastewater digester linings, while nearshoring in Mexico is boosting demand for electronics wastewater systems. However, contractor shortages are slowing project execution.

Europe's market is shaped by regulatory mandates requiring lining upgrades in chemical and pharmaceutical facilities. Germany's BASF is consolidating capacity while reinvesting in protective systems, and the UK's post-Brexit pharmaceutical growth is driving demand for FDA-compliant epoxy linings. Nordic green hydrogen pilot projects are contributing small but strategic volumes.

South America, and Middle-East and Africa accounted for smaller shares of the market. In South America, Brazil's pulp industry expansions and Argentina's lithium brine projects are driving demand for caustic-resistant linings. In the Middle-East, Saudi Arabia's Rabigh 4 and the UAE's Hatta desalination projects are key contributors. South Africa's mining sector faces challenges from power outages, delaying maintenance activities to 2026-2027.

- Ashland

- Axalta Coating Systems

- Carboline Company

- Chemco International Ltd

- Corrosion Resistant Products

- Hempel A/S

- Indochem Engineering Company

- Jindal Refractories

- Jotun

- Knight Material Technologies

- Kothari Corrosion Controllers

- PSK LININGS

- Saint-Gobain

- Sauereisen

- Sika AG

- STERLING ENGINEERING PLASTIC

- STEULER-KCH GmbH

- The Sherwin-Williams Company

- VECOM GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising corrosion-resistant demand in chemical processing

- 4.2.2 Expansion of wastewater and desalination infrastructure

- 4.2.3 Refurbishment of aging industrial assets

- 4.2.4 Tightening worker-safety durability mandates

- 4.2.5 Demand for HF-resistant linings in semiconductor etching

- 4.3 Market Restraints

- 4.3.1 High installation and lifecycle cost

- 4.3.2 Skilled-applicator scarcity and complex procedures

- 4.3.3 Low awareness among SMEs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Fiber-Reinforced Polymer (FRP) Lining

- 5.1.2 Carbon Brick Lining

- 5.1.3 Ceramic Brick Lining

- 5.1.4 Rubber Lining

- 5.1.5 PVC/CPVC Lining

- 5.1.6 Other Material Types (Epoxy, Phenolic, Bio-based)

- 5.2 By Lining Type

- 5.2.1 Tile Lining

- 5.2.2 Brick Lining

- 5.2.3 Monolithic Lining

- 5.2.4 Membrane Lining

- 5.3 By Application

- 5.3.1 Tanks and Vessels

- 5.3.2 Storage and Containment Systems

- 5.3.3 Ducts, Pipes and Flues

- 5.3.4 Floors and Drains

- 5.3.5 Towers and Reactors

- 5.3.6 Chimneys and Stacks

- 5.4 By End-user Industry

- 5.4.1 Chemical Processing

- 5.4.2 Fertilizer

- 5.4.3 Mining and Metallurgy

- 5.4.4 Oil and Gas

- 5.4.5 Power Generation

- 5.4.6 Water and Wastewater Treatment

- 5.4.7 Pulp and Paper

- 5.4.8 Food and Beverage

- 5.4.9 Pharmaceuticals

- 5.4.10 Other End-user Industries (Electroplating, Textile, Marine)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ashland

- 6.4.2 Axalta Coating Systems

- 6.4.3 Carboline Company

- 6.4.4 Chemco International Ltd

- 6.4.5 Corrosion Resistant Products

- 6.4.6 Hempel A/S

- 6.4.7 Indochem Engineering Company

- 6.4.8 Jindal Refractories

- 6.4.9 Jotun

- 6.4.10 Knight Material Technologies

- 6.4.11 Kothari Corrosion Controllers

- 6.4.12 PSK LININGS

- 6.4.13 Saint-Gobain

- 6.4.14 Sauereisen

- 6.4.15 Sika AG

- 6.4.16 STERLING ENGINEERING PLASTIC

- 6.4.17 STEULER-KCH GmbH

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 VECOM GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment