PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062396

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062396

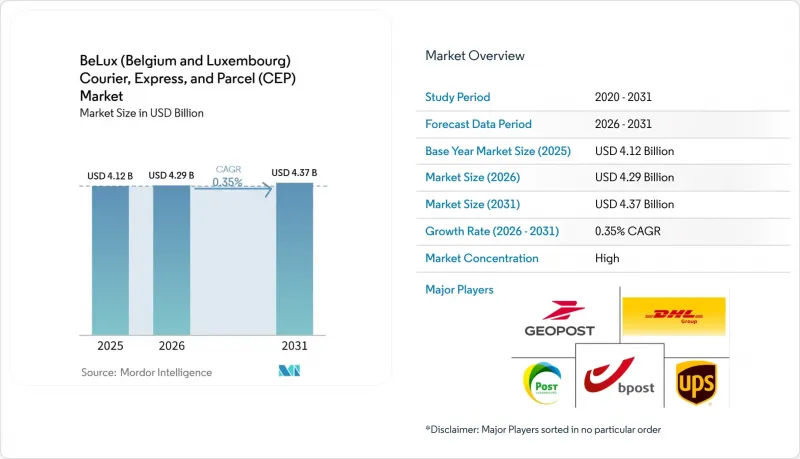

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the beLux courier, express, and parcel (CEP) market size was valued at USD 4.12 billion in 2025 and is expected to increase to USD 4.29 billion in 2026 and reach USD 4.37 billion by 2031, growing at a 0.35% CAGR from 2026 to 2031.

The near-flat growth trajectory reflects a mature landscape where incremental volume gains from cross-border e-commerce and ultrafast grocery delivery barely offset mounting cost headwinds tied to congestion charges, carbon pricing, and persistent driver shortages. This report is Segmented by Destination (Domestic, International), by Speed of Delivery (Express, Non-Express), by Model (B2B, B2C, C2C), by Shipment Weight (Heavy, Light, Medium), by Mode of Transport (Air, Road, Others), by End-User (E-Commerce, BFSI, Healthcare, Manufacturing, and More), and by Country (Belgium, Luxembourg). The Market Forecasts are Provided in Terms of Value (USD).

BeLux (Belgium And Luxembourg) Courier, Express, And Parcel (CEP) Market Trends and Insights

Acceleration of Cross-Border E-Commerce Under the VAT One-Stop-Shop

Simplified VAT registration lets Belgian and Luxembourg sellers serve all 27 EU states through a single filing portal, eliminating compliance costs that previously deterred exports. International parcel volumes are therefore set to rise at 5.97% CAGR, far eclipsing domestic growth. Clearance times have dropped to hours thanks to the Import Control System 2, unlocking next-day delivery economics for low-value items. Luxembourg's hosting of major fulfillment hubs such as Amazon further amplifies outbound flows, while SMEs leverage marketplaces to reach pan-EU buyers without setting up foreign entities. The BeLux courier express parcel market benefits from the premium service levels and customs-cleared options these merchants require.

Rise of Ultrafast <=2 h Grocery Delivery

Operators like Getir and Flink operate more than 40 micro-fulfillment sites across Brussels, stocking 2,000-3,000 SKUs and dispatching e-bikes for emission-free drops. Order density above 50 orders/km2 and baskets topping EUR 25 (USD 29) underpin viable unit economics in dense urban cores. Consolidation evidenced by Gorillas' 2025 sale to Getir signals a pivot toward scale. Restocking those dark stores generates B2B parcel demand, giving road carriers fresh revenue pockets. Ultrafast fulfillment, therefore, stimulates medium-weight parcel growth inside the BeLux courier express parcel market while accelerating locker use for returns.

Urban Congestion-Charging Zones in Brussels & Antwerp Inflating Last-Mile Costs

Brussels' 2025 Low Emission Zone (EUR 35 (USD 41)/day for non-Euro 6 diesel) and Antwerp's 2027 congestion charges (EUR 8-12 (USD 9.4-14.1)) are driving up last-mile delivery costs, especially for small operators. Large integrators like DHL and UPS benefit from scale and electrification plans. Fragmented regional rules complicate compliance, while hub-and-spoke models with electric vehicles raise handling costs. E-commerce pricing pressures prevent passing charges to customers, squeezing margins.

Other drivers and restraints analyzed in the detailed report include:

- Luxembourg Findel & Liege Airport Dual-Gateway

- Corporate Sustainability Targets and Fleet Electrification

- Chronic Driver Shortage Amid Aging Workforce and Rigid Labor Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

By destination, domestic flows held 71.83% of the BeLux courier, express, and parcel (CEP) market share in 2025, while international parcels are set to grow fastest, at a 5.97% CAGR through 2031. Although domestic shipments remain the volume backbone, they face congestion charges and rising labor costs.

Operators investing in bilingual tracking, EU-wide returns, and locker networks reduce cross-border friction and protect customer loyalty. Competitive advantage hinges on customs expertise, with EU-compliant firms commanding up to 30% per-parcel premiums. Road-rail intermodal pilots on the Brussels-Luxembourg corridor may unlock subsidies, making international niches a growing driver of strategic capex across the BeLux courier express parcel market.

By business model, the B2C segment led with 57.5% of the BeLux courier, express, and parcel (CEP) market share in 2025, while C2C is set to grow fastest, posting a 7.64% CAGR from 2026 to 2031. C2C already accounts for 1 in 5 parcels and is expected to nearly double by 2031 as resale apps like Vinted drive circular consumption.

Locker networks reduce privacy concerns, and in-app shipping fees of EUR 3-4 are widely accepted. If locker density rises, C2C's BeLux courier express parcel market share could increase significantly. B2C remains the largest revenue contributor, though free shipping pressures squeeze margins. B2B volumes decline as digital invoicing reduces document courier needs, pushing operators toward pharmaceuticals, groceries, and high-value reverse logistics. Diversification becomes essential for survival.

List of Companies Covered in this Report:

- Bpost Group (Belgian Post Group) - Including Dynalogic Belgium NV

- CMA CGM (Including Colis Prive Belgique NV)

- DHL Group

- FedEx

- GEODIS (Owned by SNCF)

- GO! (General Overnight) Express & Logistics

- InPost Sp. z o.o. (Including InPost S.A., and Mondial Relay Belgium NV)

- International Distribution Services PLC (Including GLS Group)

- Jost Group

- LaPoste Group (Including DPD Group)

- Logista (Including Belgium Parcels Service SRL - BPS)

- POST Luxembourg (Including Inflow SA, and POST Courrier)

- PostNL

- Record Express SA

- Redspher SA (Including Flash by Redspher)

- Starco Transport

- United Parcel Service of America, Inc. (UPS) - (Including Kiala SA)

- VPD NV (Vervoer en Opslag Van Peteghem-Debraekeleer NV)

- Wallenborn

- 4U-Express BVBA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Acceleration of Cross-Border E-Commerce Flows Within the EU's "VAT One-Stop-Shop" Regime

- 4.15.2 Rise of Ultrafast (<= 2 H) Grocery Deliveries Stimulating Micro-Hub Networks

- 4.15.3 Luxembourg Findel Airport's Freighter Connectivity Positioning Liege-Findel as a Dual-Gateway CEP Corridor

- 4.15.4 Corporate Sustainability Targets Driving Electrification of Last-Mile Fleets

- 4.15.5 Digital Customs & Smart-Lockers Speeding Returns and Reverse-Logistics Volumes

- 4.15.6 Growing Demand from Life-Science and Cold-Chain Parcels Supported by Pharma Clusters in Wallonia

- 4.16 Market Restraints

- 4.16.1 Urban Congestion-Charging Zones in Brussels & Antwerp Inflating Last-Mile Costs

- 4.16.2 Chronic Driver Shortage Amid Ageing Workforce and Rigid Labor Regulations

- 4.16.3 Air-Cargo Slot Scarcity at Luxembourg Findel During Peak Seasons

- 4.16.4 EU "Fit For 55" Carbon Pricing Elevating Road-Linehaul Operating Expenses

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End-User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

- 5.7 Country

- 5.7.1 Belgium

- 5.7.2 Luxembourg

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Bpost Group (Belgian Post Group) - Including Dynalogic Belgium NV

- 6.4.2 CMA CGM (Including Colis Prive Belgique NV)

- 6.4.3 DHL Group

- 6.4.4 FedEx

- 6.4.5 GEODIS (Owned by SNCF)

- 6.4.6 GO! (General Overnight) Express & Logistics

- 6.4.7 InPost Sp. z o.o. (Including InPost S.A., and Mondial Relay Belgium NV)

- 6.4.8 International Distribution Services PLC (Including GLS Group)

- 6.4.9 Jost Group

- 6.4.10 LaPoste Group (Including DPD Group)

- 6.4.11 Logista (Including Belgium Parcels Service SRL - BPS)

- 6.4.12 POST Luxembourg (Including Inflow SA, and POST Courrier)

- 6.4.13 PostNL

- 6.4.14 Record Express SA

- 6.4.15 Redspher SA (Including Flash by Redspher)

- 6.4.16 Starco Transport

- 6.4.17 United Parcel Service of America, Inc. (UPS) - (Including Kiala SA)

- 6.4.18 VPD NV (Vervoer en Opslag Van Peteghem-Debraekeleer NV)

- 6.4.19 Wallenborn

- 6.4.20 4U-Express BVBA

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment