PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062416

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062416

E-Compass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

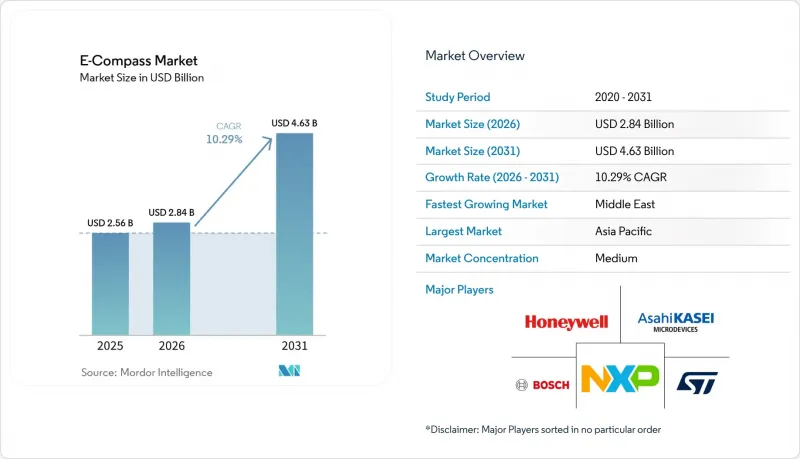

According to Mordor Intelligence, the e-Compass market size is projected to be USD 2.56 billion in 2025, USD 2.84 billion in 2026, and reach USD 4.63 billion by 2031, growing at a CAGR of 10.29% from 2026 to 2031.

This report is Segmented by Technology (Hall-Effect, Anisotropic, Giant, Tunnel Magneto-Resistive, Fluxgate, and More), Axis Orientation (1-2-Axis, 3-Axis, and 6- and 9-Axis Sensor-Fusion), Application (Consumer Electronics, and More), Form Factor (Discrete Compass Modules, Integrated Sensor-Combo, SoC-Embedded E-Compass, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global E-Compass Market Trends and Insights

Proliferation of Smartphones Integrating Navigation Sensors

Smartphone subscriptions stood at 6.9 billion in 2025, and virtually every mid-tier or flagship handset embeds a 9-axis sensor hub that blends magnetometer, accelerometer, and gyroscope data for augmented-reality overlays and indoor navigation. Integrated combo modules trimmed bill-of-material cost by 25% and enabled sub-1 millimeter package heights suitable for foldable displays. Pedestrian dead-reckoning in subways and malls now depends on magnetometer-driven heading when GNSS is unavailable. Asahi Kasei's AK09974C, released in October 2025, achieves 0.15 µT resolution in a wafer-level 1.2 X 1.2 mm package, showcasing aggressive miniaturization. Because fewer than 40% of users perform manual figure-eight calibration, vendors are building auto-calibration based on machine-learning models harvested from millions of motion traces.

Rising Adoption of ADAS in Passenger and Commercial Vehicles

Advanced Driver Assistance Systems (ADAS) were shipped in 45% of new passenger vehicles in 2025, and each Level 2+ platform includes at least one 6-axis or 9-axis inertial measurement unit to meet ISO 26262 functional-safety requirements. Magnetometers within these IMUs correct gyroscope drift during prolonged highway driving, preventing cumulative heading error. TDK's PositionSense, qualified to AEC-Q100 Grade 1 in 2024, now ships to European and Japanese OEMs, prepping 2027 model launches. Fleet operators add compass-equipped telematics boxes that shave 3-5% fuel through optimized routing, offsetting the USD 15-25 incremental sensor cost. Mandatory emergency braking and lane-keeping systems introduced in the European Union from 2024 onward continue to elevate accident rates.

Susceptibility to Magnetic Interference and Calibration Drift

Local ferrous objects and current loops create magnetic disturbances exceeding 500 µT, orders above Earth's 25-65 µT field, causing heading errors beyond 30 degrees in phones, robots, and drones. Urban skyscrapers, subway rails, and factory motors exacerbate distortion. Only 60% of end users complete manual calibration, leaving a residual offset that degrades indoor navigation. Automotive systems mitigate drift by fusing GNSS and wheel-speed encoders, but stationary service robots must rely on lookup tables or periodically updated magnetic-anomaly maps. Asahi Kasei partnered with Aizip in December 2025 to crowd-source magnetic-field maps that shorten calibration cycles from days to hours.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization and Cost Reduction Through MEMS Processes

- Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- Commodity Pricing Pressure in Consumer-Grade Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect, TMR sensors commanded 42.19% of 2025 revenue, anchored by sub-nanotesla sensitivity and thermal stability that meet AEC-Q100 and IEC 61508 norms for powertrain, avionics, and factory automation. The E-Compass market for TMR modules is set to grow at a steady, high-single-digit pace as carmakers and industrial integrators choose the architecture for long-life-cycle platforms. Hall-effect alternatives keep share in cost-constrained phones because their unit cost stays below USD 0.40, but their 10 µT noise floor caps accuracy at around 5 degrees, a ceiling that limits premium adoption. Fluxgate compasses deliver sub-degree precision for submarines and aircraft, but consume 50-200 mW, so they remain niche.

Quantum compasses using nitrogen-vacancy diamond or optically pumped alkali vapor cells are poised to grow at a 10.99% CAGR through 2031, the fastest in the E-Compass market, because they resist magnetic interference in defense and subsea environments where heading drift is unacceptable. A 2024 laboratory record showed 0.1-degree accuracy, and prototypes are undergoing trials on autonomous vehicles. Vendors such as Q-Nav are packaging diamond sensors with FPGA controllers that filter microwave drive noise, slimming form factors to 45 cm3. Governments fund pilot deployments despite 5-10X higher power draw, betting that unmanned underwater or space platforms will prioritize accuracy over battery life. Parallel R&D in chip-scale optically pumped vapor cells could shrink quantum modules to several cubic centimeters by 2030.

Three-axis compasses still accounted for 61.18% of shipments in 2025 because they meet the cost ceilings for smartphones and drones and have well-understood legacy software stacks. E-Compass market share for single-axis and dual-axis units slipped to 12% as developers reject mechanical alignment constraints. Six-axis and nine-axis packages that integrate accelerometers and gyroscopes are forecast to rise 10.57% over 2026-2031, helped by automotive Tier-1 moves to single-system-in-package units that save 40% of board area and enable tightly coupled Kalman filters.

In the automotive domain, dual 9-axis setups provide redundancy to meet ISO 26262 compliance requirements, ensuring limp-home steering even if one sensor fails. Wearables exploit 9-axis hubs to recognize gestures and detect falls, as magnetometer data improves classifier accuracy by 15% when distinguishing rotation from translation. PNI Sensor's RM3100-based NaviGuider bundles continuous hard-iron and soft-iron autocalibration, aimed at ocean gliders that cannot surface for manual routines. As downstream firmware unifies sensor-fusion libraries, manufacturers are transitioning from discrete compasses to integrated hubs that deliver quaternion vectors at 200 Hz directly to application processors, reducing development time.

Geography Analysis

Asia-Pacific accounted for 48.79% of the 2025 value, driven by China, Japan, and South Korea, which supply roughly 70% of the global Hall-effect and AMR dies. Despite the large E-Compass market share, regional players face margin compression because automotive qualification cycles stretch past 24 months and OEMs demand zero-defect supply. China absorbs 35% of local shipments through domestic phone and EV assembly, yet export restrictions on high-grade fluxgate and quantum sensors limit defense uptake, spurring indigenous firms like Bewis Sensing to fill the gap.

Japan and South Korea specialize in automotive-grade TMR and integrated IMU modules under long-term contracts with European and North American OEMs that guarantee volume until 2028. India is emerging as a leading electronics manufacturing hub, supported by electronics manufacturing incentives totaling USD 1.2 billion during 2024-2025, positioning the country as a low-cost alternative for consumer and industrial markets. The E-Compass market size in Asia-Pacific is expected to expand steadily but at slower margins than in Western regions.

The Middle East shows the fastest trajectory, slated for a 19.84% CAGR through 2031, as Saudi Vision 2030 drives local sensor production and defense programs procure ITAR-free navigation systems. Teledyne's 2025 launch of its Dammam plant and KROHNE's 2026 localization MoU underscore thee riseof regional supply chains. North America and Europe together accounted for 32% of 2025 revenue, driven by the aerospace, defense, and industrial robotics sectors, which demand radiation-hardened, tilt-compensated compasses. South America remained below 5%, but precision agriculture in Brazil and Argentina is prompting the adoption of GNSS-aided compass arrays for centimeter-level row guidance.

- STMicroelectronics N.V.

- Honeywell International Inc.

- Robert Bosch GmbH (Bosch Sensortec GmbH)

- Asahi Kasei Microdevices Corporation

- NXP Semiconductors N.V.

- TDK Corporation (Invensense Inc.)

- MEMSIC Semiconductor (Shanghai) Co., Ltd.

- PNI Sensor Corporation

- Analog Devices, Inc.

- Alps Alpine Co., Ltd.

- Infineon Technologies AG

- TE Connectivity Ltd.

- Shanghai Bewis Sensing Technology LLC

- Ericco International Limited

- Jewell Instruments, LLC

- Melexis N.V.

- MagnaChip Semiconductor Corp.

- Renesas Electronics Corporation

- Lake Shore Cryotronics, Inc.

- VectorNav Technologies, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Proliferation of Smartphones Integrating Navigation Sensors

- 4.7.2 Rising Adoption of ADAS in Passenger and Commercial Vehicles

- 4.7.3 Miniaturization and Cost Reduction Through MEMS Processes

- 4.7.4 Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- 4.7.5 Autonomous Maritime Drones Needing Tilt-Compensated Heading

- 4.7.6 Precision-Ag-Robots Deploying Row-Guidance E-Compass Arrays

- 4.8 Market Restraints

- 4.8.1 Susceptibility to Magnetic Interference and Calibration Drift

- 4.8.2 Commodity Pricing Pressure in Consumer-Grade Devices

- 4.8.3 High Power Consumption in Fluxgate and Quantum Compass Designs

- 4.8.4 Export-Control Limits on High-Sensitivity Fluxgate Modules

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Hall-Effect

- 5.1.2 Anisotropic, Giant, Tunnel Magneto-Resistive

- 5.1.3 Fluxgate

- 5.1.4 Magneto-Inductive

- 5.1.5 Quantum

- 5.2 By Axis Orientation

- 5.2.1 1-2-Axis

- 5.2.2 3-Axis

- 5.2.3 6- and 9-Axis Sensor-Fusion

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Industrial and Robotics

- 5.3.5 Marine and Sub-Sea

- 5.3.6 Healthcare and Wearables

- 5.4 By Form Factor

- 5.4.1 Discrete Compass Modules

- 5.4.2 Integrated Sensor-Combo

- 5.4.3 SoC-Embedded E-Compass

- 5.4.4 Dev-Boards and Custom ASICs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Robert Bosch GmbH (Bosch Sensortec GmbH)

- 6.4.4 Asahi Kasei Microdevices Corporation

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 TDK Corporation (Invensense Inc.)

- 6.4.7 MEMSIC Semiconductor (Shanghai) Co., Ltd.

- 6.4.8 PNI Sensor Corporation

- 6.4.9 Analog Devices, Inc.

- 6.4.10 Alps Alpine Co., Ltd.

- 6.4.11 Infineon Technologies AG

- 6.4.12 TE Connectivity Ltd.

- 6.4.13 Shanghai Bewis Sensing Technology LLC

- 6.4.14 Ericco International Limited

- 6.4.15 Jewell Instruments, LLC

- 6.4.16 Melexis N.V.

- 6.4.17 MagnaChip Semiconductor Corp.

- 6.4.18 Renesas Electronics Corporation

- 6.4.19 Lake Shore Cryotronics, Inc.

- 6.4.20 VectorNav Technologies, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment