PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062446

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062446

Dielectric Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

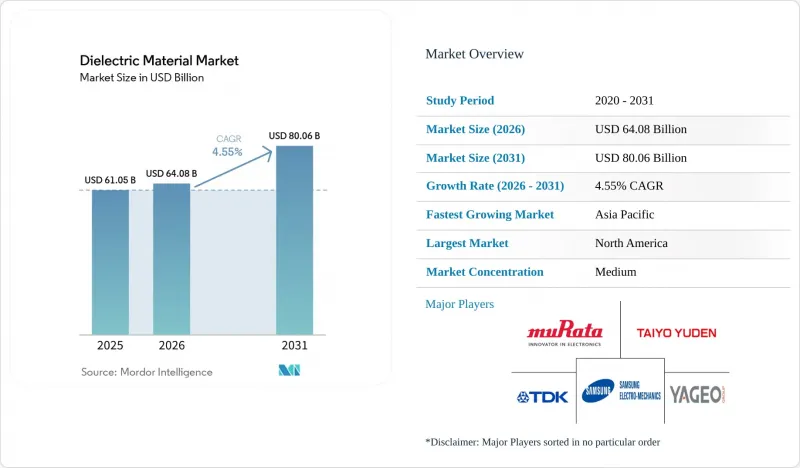

According to Mordor Intelligence, the dielectric material market size is projected to be USD 61.05 billion in 2025, USD 64.08 billion in 2026, and reach USD 80.06 billion by 2031, growing at a CAGR of 4.55% from 2026 to 2031.

This report is Segmented by Material Type (Ceramic, Polymer Film, Glass and Glass-Ceramics, and More), Form Factor (MLCC Dielectric, Thin/Thick Film Dielectric, and More), Dielectric Constant Category (Low-K, Medium-K, and More), Application (Passive Electronic Components, and More), End-Use Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Dielectric Material Market Trends and Insights

Proliferation of Electric Vehicles Boosting Demand for High-Energy Film Capacitors

Electric-vehicle architectures moving to 800-volt batteries need film capacitors that store more than 5 J/cm3 at 900 Vdc without catastrophic failure at 105 °C. Metalized polypropylene winds enhanced with nano-aluminum electrodes meet these thresholds and self-heal after transient spikes, giving inverter makers confidence in 15-year warranties. Silicon-carbide switches that toggle above 100 kHz increase harmonic stress, prompting multilayer polypropylene-polyethylene films to spread heat faster and shave 1.5 kg from inverter weight. Qualification cycles that run 1,000 thermal shocks and 2,000 h humidity aging now dominate launch schedules and tilt volume toward incumbents that can certify at scale. Automakers have responded with multi-year allocation contracts, locking in visibility into demand through the decade.

Rapid Expansion of 5G and High-Frequency Communication Devices

Millimeter-wave radios above 24 GHz impose loss-tangent limits below 0.002 on substrates, propelling low-temperature co-fired alumina-glass composites that condense filters and couplers into a single laminated block. Each macro-cell radio consumes hundreds of high-frequency capacitors, and with over 1 million 5G sites installed in China by 2025, volume pull-through is significant. Temperature-stable X7R stacks maintain +-15% capacitance from -55 °C to +125 °C, meeting the requirements of outdoor and automotive radios deployed on rooftops and roadway gantries. As operators pivot to standalone 5G core networks in 2026, edge servers require large banks of 100 A ripple-rated multilayer ceramic capacitors, a spec only a handful of suppliers can meet today.

Volatile Prices and Limited Supply of Rare-Earth Elements for High-K Ceramics

Yttrium and lanthanum oxides swung 15-25% in price during 2024-2025 after export-quota moves in China, adding direct material inflation to X7R and X8R stacks. Japanese and South Korean producers resorted to six-month stockpiles, tying up working capital and slicing 200 bp off gross margins. Substitution with bismuth-sodium-titanate or potassium-sodium-niobate lowers permittivity by up to 30%, so layer counts creep upward, eroding miniaturization gains. Geopolitical risk has attracted U.S. Department of Energy funding for domestic separation plants, yet commercial volumes are unlikely before 2028, keeping the dielectric material market exposed in the mid-term.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization Trend in Consumer Electronics Driving Ultra-Thin MLCC Dielectrics

- Growth in Renewable Energy Installations Requiring High-Voltage Power Capacitors

- Stringent Environmental Rules on Fluorinated Polymer Dielectrics Disposal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceramic grades secured 46.11% of the dielectric material market share in 2025 on the strength of barium-titanate systems that pack dielectric constants above 10,000, meeting X5R and X7R codes. Glass and glass-ceramic alternatives are growing at 4.96% through 2031 as power-electronics designers seek thermal-shock tolerance for -40 °C to +150 °C cycling. Polymer films hold a niche high-voltage territory, where self-healing prevents runaway failure in automotive and solar inverters. Mica and tantalum oxide remain specialized for aerospace radar and implantable devices, where lifetime reliability eclipses cost.

Advances in barium-strontium-titanate thin films support 5G tunable filters, while potassium-sodium-niobate piezoelectrics offer lead-free compliance but face 400 °C Curie points. Glass-ceramic substrates with lithium-aluminum-silicate phases are now being used in gallium-nitride HEMTs, offering near-zero expansion that reduces die stress. Polymer-film suppliers layer polypropylene with polyethylene naphthalate to lift thermal conductivity by 35%, giving the dielectric material market size a shot at durability for 15-year electric-vehicle lifetimes.

Multilayer ceramic capacitor stacks accounted for 39.42% of 2025 revenue, thanks to unmatched volumetric efficiency that smartphones, EVs, and industrial drives rely on. Dielectric inks and pastes, however, are sprinting at a 4.81% CAGR, promoted by roll-to-roll antenna and sensor printing on flexible PET. Thin- and thick-film coatings on alumina or AlN address hybrid microwave modules, while bulk sheets machined from sintered blocks stay relevant for traction drives and pulsed-power labs.

Ink formulations blending barium-titanate nanoparticles with silver flakes hit sheet resistances below 0.1 Ω/□, yet 900 °C sinter limits polymer substrates, so photonic flash sintering is the new frontier. Reliability lags MLCCs, with 15% drift after 500 thermal cycles, delaying automotive adoption. Bulk glass-ceramic plates still dominate medium-voltage vacuum interrupters, underlining how each form factor defends its sweet spot within the dielectric material market.

Geography Analysis

Asia-Pacific retained 47.67% of the dielectric material market share in 2025 and is forecast to grow at a 5.22% CAGR through 2031. Japan and South Korea anchor multibillion-unit MLCC output, leveraging vertically integrated powder-to-placement lines capable of sub-0201 geometries at 10 billion units per month. China's Fenghua Advanced Technology and Torch Electron are buying shares in consumer-grade segments by parlaying labor subsidies and provincial incentives, though they still lag automotive-grade quality metrics. India's production-linked incentive program is attracting passive-component assembly from Taiwan-origin firms, helping cushion the impact of supply diversification.

Europe and North America combined for roughly 35% of revenue in 2025, led by Germany's 800 V drivetrain projects and France's offshore wind farms that specify glass-ceramic capacitors for 50-year turbine lives. Brussels-driven PFAS restrictions are accelerating film-to-ceramic substitution, while the United States CHIPS Act's USD 52 billion outlay is pulling high-K dielectric volume into new Arizona and Texas fabs. Canada's rare-earth exploration in Saskatchewan and Quebec could temper dependence on yttrium post-2028, yet near-term supply remains Asia-centric.

Middle East and Africa, plus South Americ, a, accounted for the remaining 18% in 2025, driven by telecom densification and renewable-energy rollouts. Saudi Arabia's NEOM city blueprint specifies low-loss ceramic nodes for pervasive 5G, and the United Arab Emirates' 950 MW solar park relies on polypropylene capacitors in string inverters. South Africa's EV shift is driving partnerships with regional distributors for AEC-Q200 passives, while Brazil's 25 GW wind fleet is boosting demand for medium-voltage capacitors despite 15% import tariffs that favor local assembly. Argentina's lithium boom is drawing battery-pack investments, creating downstream pull for dielectric materials in battery-management and charging gear.

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Taiyo Yuden Co., Ltd.

- Kyocera Corporation

- KEMET Corporation (a Yageo Company)

- Yageo Corporation

- Nippon Chemi-Con Corporation

- Samwha Electric Co., Ltd.

- Vishay Intertechnology, Inc.

- Rubicon Technology, Inc.

- Rogers Corporation

- Showa Denko Materials Co., Ltd.

- Panasonic Holdings Corporation

- Walsin Technology Corporation

- Samsung Electro-Mechanics Co., Ltd.

- Ferro Corporation

- Cangzhou Mingzhu Plastic Co., Ltd.

- Hexagon Energy Materials Limited

- Solvay S.A.

- AVX Corporation (a Kyocera Group Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of 5G and High-Frequency Communication Devices

- 4.2.2 Proliferation of Electric Vehicles Boosting Demand for High-Energy Film Capacitors

- 4.2.3 Growth in Renewable Energy Installations Requiring High-Voltage Power Capacitors

- 4.2.4 Miniaturization Trend in Consumer Electronics Driving Ultra-Thin MLCC Dielectrics

- 4.2.5 Emerging Use of Ferroelectric Hafnium-Oxide in Advanced Logic and Memory Chips

- 4.2.6 Rising Adoption of Wireless-Charging Furniture with Embedded Dielectric Resonators

- 4.3 Market Restraints

- 4.3.1 Volatile Prices and Limited Supply of Rare-Earth Elements for High-K Ceramics

- 4.3.2 Stringent Environmental Rules on Fluorinated Polymer Dielectrics Disposal

- 4.3.3 Reliability Issues of Additive-Manufactured Dielectric Inks

- 4.3.4 Thermal-Runaway Concerns in Solid-State Capacitor Banks

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Ceramic

- 5.1.2 Polymer Film

- 5.1.3 Glass and Glass-Ceramics

- 5.1.4 Other Material Type

- 5.2 By Form Factor

- 5.2.1 Multilayer Ceramic Chip Capacitor (MLCC) Dielectric

- 5.2.2 Thin / Thick Film Dielectric

- 5.2.3 Bulk Sheet / Plate

- 5.2.4 Dielectric Ink and Paste

- 5.3 By Dielectric Constant Category

- 5.3.1 Low-K

- 5.3.2 Medium-K

- 5.3.3 High-K

- 5.4 By Application

- 5.4.1 Passive Electronic Components, Capacitors, Resonators

- 5.4.2 Semiconductor Gate Dielectric

- 5.4.3 Power Electronics Insulation

- 5.4.4 RF and Microwave Substrates

- 5.4.5 Printed and Flexible Electronics

- 5.5 By End-Use Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Automotive and E-Mobility

- 5.5.3 Energy and Power, Renewables, Grid

- 5.5.4 Telecommunications

- 5.5.5 Industrial and Manufacturing

- 5.5.6 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 TDK Corporation

- 6.4.3 Taiyo Yuden Co., Ltd.

- 6.4.4 Kyocera Corporation

- 6.4.5 KEMET Corporation (a Yageo Company)

- 6.4.6 Yageo Corporation

- 6.4.7 Nippon Chemi-Con Corporation

- 6.4.8 Samwha Electric Co., Ltd.

- 6.4.9 Vishay Intertechnology, Inc.

- 6.4.10 Rubicon Technology, Inc.

- 6.4.11 Rogers Corporation

- 6.4.12 Showa Denko Materials Co., Ltd.

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Walsin Technology Corporation

- 6.4.15 Samsung Electro-Mechanics Co., Ltd.

- 6.4.16 Ferro Corporation

- 6.4.17 Cangzhou Mingzhu Plastic Co., Ltd.

- 6.4.18 Hexagon Energy Materials Limited

- 6.4.19 Solvay S.A.

- 6.4.20 AVX Corporation (a Kyocera Group Company)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment