PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062447

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062447

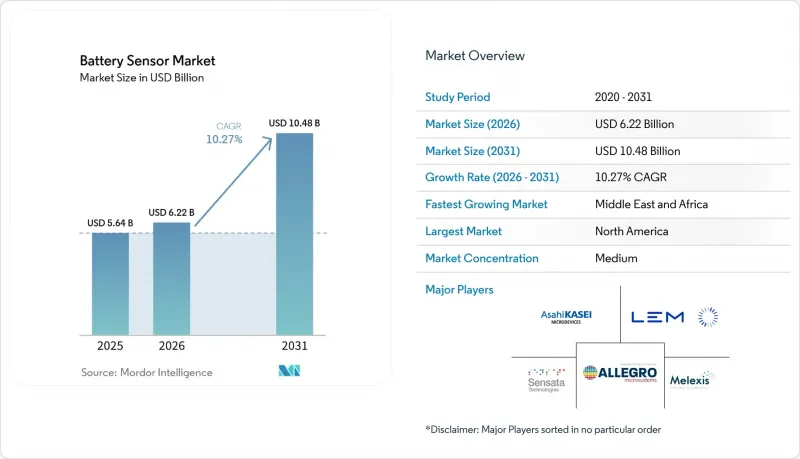

Battery Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the battery sensor market size is expected to increase from USD 5.64 billion in 2025 and USD 6.22 billion in 2026 to reach USD 10.48 billion by 2031, growing at a CAGR of 10.27% over 2026-2031.

This report is Segmented by Sensor Type (Hall-Effect Current Sensors, and More), Technology (Closed-Loop Sensors, Open-Loop Sensors, and More), Application (Electric Passenger Vehicles, Electric Commercial Vehicles, and More), End-User Industry (Automotive, Energy and Utilities, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Battery Sensor Market Trends and Insights

EV Production Surge And Stringent xEV Battery-Safety Mandates

China's GB38031-2025 standard obliges passenger cars and fleets to detect thermal runaway within five minutes, forcing a shift from simple thermistor strings to multi-sensor fusion that couples Hall-effect current, fiber-optic temperature, and MEMS pressure channels. The ISO 21498 interface, ratified in 2024, adds bidirectional data paths between battery management systems and vehicle control units, enabling real-time power limitation that curbs over-discharge events. ZOE Energy Storage fielded a four-parameter detection stack in 2025 that identifies runaway 20 times earlier than legacy packs, illustrating how regulatory pressure is reshaping design rules.

Rapid Growth Of Utility-Scale Energy-Storage Installations

Alliant Energy's 200 MW-400 MWh site in Wisconsin, commissioned in March 2026, relies on 12,000 monitored cells across 50 containers, highlighting the scale of sensor deployment in modern grids. SSE's 100 MW Ferrybridge system uses impedance spectroscopy to flag internal resistance drift and lengthen service life. Wireless monitors at Georgia Power's 65 MW facility removed two kilometers of copper harness, cutting installation outlay by USD 120,000. These installations show how sensor-enabled predictive maintenance underpins lower levelized cost of storage.

Wide Temperature-Drift And Offset Errors In Low-Cost Shunt Solutions

Automotive temperature cycles induce 50 µV °C-1 offset drift in bare shunts, translating into 3% range-prediction error over vehicle life. External op-amps with 120 dB common-mode rejection are required, adding USD 1.20 in components and offsetting shunts' perceived savings. EMI from 800 V inverters further pushes total error beyond 0.5%, breaching ISO 21498 accuracy limits.

Other drivers and restraints analyzed in the detailed report include:

- Falling Cost And Accuracy Gains In Hall-Effect Current Sensors

- Standardization Of ISO 21498 Battery Monitoring Interfaces

- Volatile Pricing And Supply Of Ferrite Or Permalloy Magnetic Cores

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect devices owned 43.2% Battery sensor market share in 2025, thanks to contactless bidirectional measurement vital for regenerative braking. Fiber-optic sensors are on an 11.9% CAGR path to 2031, propelled by solid-state battery pilots that require ceramic-safe, distributed temperature reading. Shunts stay relevant in consumer gadgets where +-1% suffices, yet ISO 21498 pushes automotive platforms toward Hall accuracies. Texas Instruments' 18-channel voltage IC, shipping since August 2025, resolves 1 mV differentials, reinforcing integrated monitoring roadmaps.

Fiber Bragg grating strings are gaining in utility-scale systems, resisting electromagnetic interference that plagues thermistors near high-voltage inverters. MEMS pressure chips, such as Honeywell's 0.25%-FS BPS line, detect 2 kPa gas buildup well before exothermic escalation. Growth is tempered by the lack of automotive-rated fiber connectors that survive 3,000 matings and -40 °C to 125 °C cycles, a gap both Corning and Prysmian address with rugged LC variants.

Closed-loop isolated designs delivered 40.5% revenue in 2025, driven by the increasing demand for drift-free 1,000 A sensing in 800 V platforms, which are critical for high-performance electric vehicles and industrial applications. Wireless nodes are forecast to grow at an 11.7% CAGR, as Dukosi's C-SynQ technology demonstrated a 15% reduction in pack mass and a 40% decrease in assembly time, particularly benefiting commercial fleet operators. NXP's ultra-wideband platform offers precise 10 cm 3-D cell location capabilities, simplifying warranty forensics by enabling quick identification and mapping of faulty units, which is crucial for minimizing downtime and operational inefficiencies.

Digital output sensors utilizing CAN FD and I2C protocols are expanding rapidly, with Infineon's XDM700-1 sensor transferring 18-channel data at 5 Mbps, catering to the growing need for high-speed data communication in modern battery management systems. Meanwhile, analog variants are increasingly relegated to legacy industrial UPS roles due to their limited capabilities. Renesas' DA14533 sensor supports a 10-year coin-cell lifetime for Bluetooth Low Energy sensors, making it an ideal solution for e-scooters and other compact mobility devices. However, the dual certification process for CAN-to-Bluetooth gateways has been identified as a bottleneck, extending product launch timelines by approximately 9 months, posing challenges for manufacturers aiming to meet market demand swiftly.

Geography Analysis

Asia-Pacific generated 33.3% of the battery sensor market revenue in 2025 and is set for an 11.1% CAGR to 2031 as GB38031-2025 makes thermal-runaway detection compulsory. Japanese vendors, exemplified by B-and-Plus's April 2026 wireless monitor, scrap harnesses in automated guided vehicles, improving swap speed. South Korea specifies impedance spectroscopy for 350 kW charging, satisfied by NXP's BMA7418 chipset. India's above 50 MW renewable projects mandate battery energy-storage add-ons, spurring demand for cost-optimized sensors.

North America and Europe prioritize ISO 26262 ASIL D dual-channel current sensing. Germany champions coreless Hall sensors, with Infineon trimming EUR 0.80 (USD 0.85) per unit by deleting ferrite cores. The United Kingdom's Ferrybridge site projects an 8% lower levelized storage cost via impedance spectroscopy. U.S. utilities in Wisconsin and Georgia illustrate the cost case for wireless monitors that wipe out thousands of dollars in copper.

The Middle East and Africa adopt battery storage in megaprojects such as Saudi Arabia's NEOM, specifying hydrogen gas detection to tackle high-ambient heat. South Africa's renewables program turns to shunt solutions at 40% lower cost where 1% accuracy suffices. South American adoption is concentrated in Brazil, where NOM-194-SCFI-2015 aligns with digital monitors built on CAN FD.

- Allegro MicroSystems, Inc.

- Asahi Kasei Microdevices Corporation

- Melexis NV

- LEM Holding SA

- Sensata Technologies Holding plc

- Texas Instruments Incorporated

- Infineon Technologies AG

- TDK Corporation

- Honeywell International Inc.

- TE Connectivity Ltd.

- Analog Devices, Inc.

- NXP Semiconductors N.V.

- Murata Manufacturing Co., Ltd.

- HIOKI E.E. Corporation

- Littelfuse, Inc.

- Renesas Electronics Corporation

- Alpha and Omega Semiconductor Limited

- Silicon Laboratories Inc.

- Eaton Corporation plc

- ROHM Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Production Surge and Stringent xEV Battery-Safety Mandates

- 4.2.2 Rapid Growth of Utility-Scale Energy-Storage Installations

- 4.2.3 Falling Cost and Accuracy Gains in Hall-Effect Current Sensors

- 4.2.4 Standardization of ISO 21498 Battery Monitoring Interfaces

- 4.2.5 Integration of Cell-Level Fiber-Optic Sensing in Solid-State Battery Pilots

- 4.2.6 Adoption of Wake-on-CAN Ultra-Low-Power Sensing for Micro-Mobility Packs

- 4.3 Market Restraints

- 4.3.1 Wide Temperature-Drift and Offset Errors in Low-Cost Shunt Solutions

- 4.3.2 Volatile Pricing and Supply of Ferrite or Permalloy Magnetic Cores

- 4.3.3 EMC Compliance Hurdles for 1 MHz Isolated Current-Sensor Modulation

- 4.3.4 Scarcity of Certification Labs for Wireless Battery-Sensor Protocols

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Hall-Effect Current Sensors

- 5.1.2 Shunt-Based Current Sensors

- 5.1.3 Voltage Monitoring ICs

- 5.1.4 Temperature (NTC / PTC) Sensors

- 5.1.5 Fiber-Optic Battery Sensors

- 5.1.6 MEMS Pressure Sensors (Cell-Level)

- 5.2 By Technology

- 5.2.1 Closed-Loop (Isolated) Sensors

- 5.2.2 Open-Loop Sensors

- 5.2.3 Digital (I2C / CAN / SENT) Output

- 5.2.4 Analog Output

- 5.2.5 Wireless Battery Sensors

- 5.3 By Application

- 5.3.1 Electric Passenger Vehicles

- 5.3.2 Electric Commercial Vehicles

- 5.3.3 Hybrid and Plug-in Hybrid Vehicles

- 5.3.4 Stationary Energy-Storage Systems

- 5.3.5 Consumer Electronics

- 5.3.6 Industrial UPS and Backup

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Energy and Utilities

- 5.4.3 Consumer Electronics

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Telecommunications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Allegro MicroSystems, Inc.

- 6.4.2 Asahi Kasei Microdevices Corporation

- 6.4.3 Melexis NV

- 6.4.4 LEM Holding SA

- 6.4.5 Sensata Technologies Holding plc

- 6.4.6 Texas Instruments Incorporated

- 6.4.7 Infineon Technologies AG

- 6.4.8 TDK Corporation

- 6.4.9 Honeywell International Inc.

- 6.4.10 TE Connectivity Ltd.

- 6.4.11 Analog Devices, Inc.

- 6.4.12 NXP Semiconductors N.V.

- 6.4.13 Murata Manufacturing Co., Ltd.

- 6.4.14 HIOKI E.E. Corporation

- 6.4.15 Littelfuse, Inc.

- 6.4.16 Renesas Electronics Corporation

- 6.4.17 Alpha and Omega Semiconductor Limited

- 6.4.18 Silicon Laboratories Inc.

- 6.4.19 Eaton Corporation plc

- 6.4.20 ROHM Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment