PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062451

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062451

RAN Analytics And Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

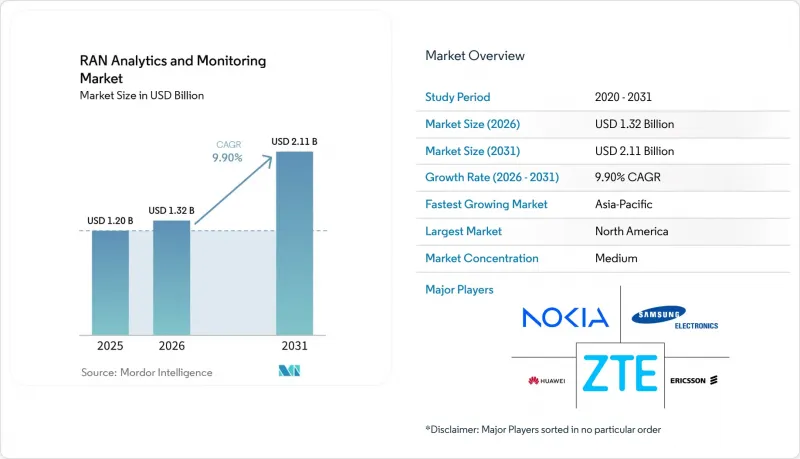

According to Mordor Intelligence, the rAN analytics and monitoring market size is projected to expand from USD 1.20 billion in 2025 and USD 1.32 billion in 2026 to USD 2.11 billion by 2031, registering a CAGR of 9.9% between 2026 to 2031.

This report is Segmented by Component (Platform/Software, and Services), Deployment Mode (On-Premises, and Cloud-Based), Network Technology (4G/LTE, and More), Application (Performance Management, Fault and Event Management, and More), End User (Tier-1 Mobile Network Operators, Mobile Virtual Network Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global RAN Analytics And Monitoring Market Trends and Insights

AI-Driven Predictive Maintenance For 5G Densification

Predictive maintenance is becoming essential as operators add thousands of small cells to satisfy mid-band capacity requirements. The shift cuts manual engineering hours by automatically detecting interference, sleeping cells, or degraded beams before service quality dips. Deployments such as Huawei and China Mobile's 400,000-site project have proven the scalability of autonomous agents at carrier-grade. Vendors now compete on providing pre-trained models and closed-loop workflows that can be activated without deep data-science skills, shortening time to value. Commercial success stories are accelerating budget reallocation from legacy key performance indicator dashboards to automated remediation platforms. The prevailing expectation is that software able to predict and prevent outages will underpin most new contracts signed after 2026.

Cloud-Native RAN Disaggregation Accelerates Data Visibility

Breaking the RAN into centralized, distributed, and radio units opens additional telemetry points that cloud-native analytics harness in real time. Solutions such as Nokia's Autonomous Network Fabric and Infovista's driverless field validation stream gigabit-per-second data streams into elastic, API-first backends. Operators gain fine-grained visibility across multiple vendors, reduce lock-in, and can spin up new analytic functions without forklift upgrades. This architectural freedom is offset by the need to run dual assurance stacks while legacy systems are retired, yet most tier-1 carriers judge the benefits of flexibility and speed to outweigh transitional complexity.

Fragmented data standards across multi-vendor RAN

Heterogeneous log formats impede the training of unified models, forcing operators to maintain custom parsers that raise integration costs. NETSCOUT's 2024 AIOps survey lists inconsistent schemas as the top inhibitor of machine-learning rollouts, ahead of compute shortages and licensing fees. Indian carriers piloting multi-vendor Open RAN cite the need for third-party system integrators to normalize data as a major expense spike, often doubling project timelines. The O-RAN Alliance promotes common information models, but equipment makers still release proprietary counters for competitive edge, prolonging normalization efforts.

Other drivers and restraints analyzed in the detailed report include:

- Surge Of Private 5G Networks In Industry 4.0 Plants

- Open RAN Automation And xApps-rApps Ecosystem Expansion

- Skills gap in AI/ML model engineering for CSPs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software accounted for the bulk of 2025 revenue, yet rising multi-vendor complexity means services are climbing faster. Operators recognize that continuous model retraining and cross-domain correlation exceed routine network operations center competencies, so they purchase deployment, customization, and lifecycle management as outcome-based engagements. The RAN analytics and monitoring market size attributed to managed services is therefore expanding at a double-digit pace, while suppliers differentiate through libraries of pre-built use cases and service-level guarantees.

Services growth also reflects skills shortages in AI engineering and open-RAN orchestration. System integrators such as Capgemini and HCL Technologies are building 24/7 centers of excellence, and vendors bundle evergreen upgrades into subscriptions that convert capital outlays into predictable operating expenses. Because most tier-2 carriers and enterprise private-network owners lack specialist teams, service-led delivery will remain the preferred model through 2031, even as larger operators keep investing in proprietary software stacks.

Cloud-based implementations already hold a majority of deployments thanks to elasticity, pay-as-you-grow economics, and native integration with hyperscale AI toolchains. Streaming telemetry from tens of thousands of cell sites is better handled by horizontal auto-scaling than by fixed on-premises clusters. As a result, cloud platforms frequently demonstrate the lowest total cost of ownership when traffic spikes, firmware upgrades, or new spectrum bands multiply data volumes.

On-premises and hybrid models persist for latency-sensitive or sovereignty-constrained workloads. European carriers, for example, process personal-data-heavy analytics in private clouds to comply with the General Data Protection Regulation, while exporting non-identifiable training sets to public clouds for cheaper model iteration. Over the forecast horizon, the RAN analytics and monitoring market will continue shifting toward a cloud-first stance, but vendors able to unify edge, private, and public resources under a single policy framework will enjoy the widest adoption.

Geography Analysis

North America drives the largest share of spending thanks to aggressive mid-band spectrum roll-outs by Verizon, AT&T, and T-Mobile, and a pervasive move toward open RAN test beds. Early trials of multi-vendor RAN intelligent controllers have boosted confidence in standards-based telemetry, unlocking budgets for vendor-agnostic monitoring suites. Densification has also spilled into tower-company capital expenditure, cementing analytics demand across both carriers and infrastructure owners.

Europe combines regulatory support for open interfaces with stringent energy-efficiency directives, channeling investment into power analytics modules and cyber-secure, disaggregated architectures. Operators such as Deutsche Telekom and Vodafone are building internal digital twins to benchmark suppliers and comply with NIS2 requirements, ensuring steady procurement of cross-vendor correlation engines. Germany leads private-network uptake in automotive manufacturing, while the United Kingdom and France prioritize carbon-tracking dashboards to meet national sustainability targets.

Asia-Pacific posts the fastest CAGR as India's greenfield 5G, China's autonomous-agent deployments, and Southeast Asia's virtualized RAN pilots scale concurrently. Projects such as China Mobile's 400,000-site intelligent-agent deployment validate carrier-grade AI operations, encouraging regional peers to adopt similar frameworks. Japan's push into software-defined RAN and Australia's focus on rural coverage round out a highly diverse patchwork, yet all sub-regions converge on a playbook that values cloud elasticity, energy savings, and open-interface flexibility.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Samsung Electronics Co., Ltd. (Network Business)

- NEC Corporation

- Mavenir Systems, Inc.

- Viavi Solutions Inc.

- MYCOM OSI Limited

- Infovista SAS

- TEOCO Corporation

- EXFO Inc.

- NETSCOUT Systems, Inc.

- Cellwize Wireless Technologies Pte Ltd.

- AirHop Communications, Inc.

- Parallel Wireless, Inc.

- Tupl, Inc.

- Rakuten Symphony Inc.

- Capgemini SE (Engineering and RAN Analytics)

- HCL Technologies Limited

- Amdocs Limited

- VMware, Inc. (Service Management and Analytics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-driven Predictive Maintenance for 5G Densification

- 4.2.2 Cloud-native RAN Disaggregation Accelerates Data Visibility

- 4.2.3 Surge of Private 5G Networks in Industry 4.0 Plants

- 4.2.4 Open RAN Automation/xApps-rApps Ecosystem Expansion

- 4.2.5 Energy-efficiency Mandates Driving RAN Power Analytics

- 4.2.6 Telco Push Toward Zero-touch Operations (ZTO)

- 4.3 Market Restraints

- 4.3.1 Fragmented Data Standards Across Multi-vendor RAN

- 4.3.2 Skills Gap in AI/ML Model Engineering for CSPs

- 4.3.3 Rising Cyber-attack Surface on Virtualised RAN

- 4.3.4 ROI Uncertainty in Brown-field 4G Modernisations

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform / Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud-based

- 5.3 By Network Technology

- 5.3.1 2G / 3G

- 5.3.2 4G / LTE

- 5.3.3 5G NR

- 5.3.4 Open RAN / vRAN

- 5.4 By Application

- 5.4.1 Performance Management

- 5.4.2 Fault and Event Management

- 5.4.3 Mobility and Handover Optimisation

- 5.4.4 Energy and Capacity Optimisation

- 5.5 By End User

- 5.5.1 Tier-1 Mobile Network Operators

- 5.5.2 Mobile Virtual Network Operators

- 5.5.3 Private Enterprise Networks

- 5.5.4 Neutral-Host / TowerCos

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Nokia Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 ZTE Corporation

- 6.4.5 Samsung Electronics Co., Ltd. (Network Business)

- 6.4.6 NEC Corporation

- 6.4.7 Mavenir Systems, Inc.

- 6.4.8 Viavi Solutions Inc.

- 6.4.9 MYCOM OSI Limited

- 6.4.10 Infovista SAS

- 6.4.11 TEOCO Corporation

- 6.4.12 EXFO Inc.

- 6.4.13 NETSCOUT Systems, Inc.

- 6.4.14 Cellwize Wireless Technologies Pte Ltd.

- 6.4.15 AirHop Communications, Inc.

- 6.4.16 Parallel Wireless, Inc.

- 6.4.17 Tupl, Inc.

- 6.4.18 Rakuten Symphony Inc.

- 6.4.19 Capgemini SE (Engineering and RAN Analytics)

- 6.4.20 HCL Technologies Limited

- 6.4.21 Amdocs Limited

- 6.4.22 VMware, Inc. (Service Management and Analytics)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment