PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062469

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062469

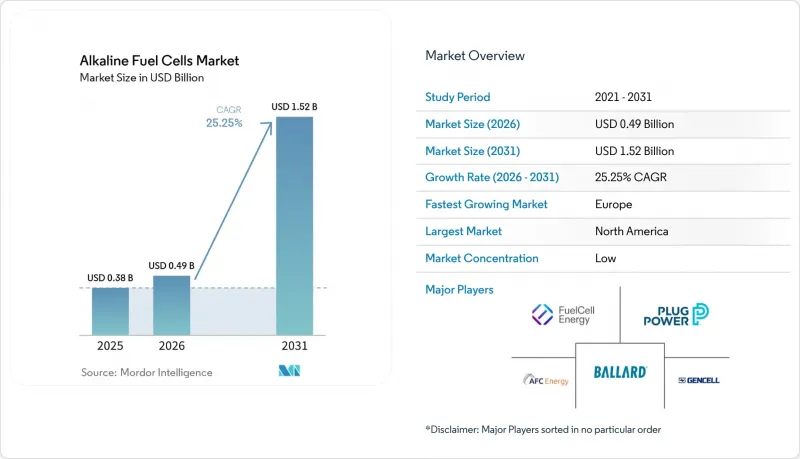

Alkaline Fuel Cells - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the alkaline fuel cells market size was valued at USD 0.38 billion in 2025 and is estimated to grow from USD 0.49 billion in 2026 to reach USD 1.52 billion by 2031, at a CAGR of 25.25% during the forecast period (2026-2031).

This report is Segmented by Type (Static Alkaline Fuel Cells and Mobile/Portable Alkaline Fuel Cells), Power Output (Up To 5 KW, 5 To 50 KW, and More), Application (Military and Defense, Spacecraft and Launch Systems, Backup and Remote Power, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Alkaline Fuel Cells Market Trends and Insights

Declining Electrolyzer Costs Drive Commercial Viability

Widespread scale-up brings alkaline electrolyzer capex to USD 389.5 per kW for sub-20 MW plants and USD 82.8 per kW for larger units, narrowing hydrogen's cost gap with fossil fuels. Nickel-based electrodes avoid platinum group metals, trimming bill-of-materials risk and pushing stack life beyond 80,000 h. Targeted R&D support, such as the U.S. Department of Energy's USD 5 million grant to Avium, continues to improve catalyst efficiency and longevity. Similar EU initiatives funnel funding toward next-generation alkaline technology, hastening the rollout of 40 GW of renewable hydrogen electrolyzers by 2030. These developments amplify near-term bankability and underpin the alkaline fuel cells market's aggressive growth path.

Growing Military Demand for Silent Power Systems

Defense establishments are accelerating procurement to replace noisy diesel generators with silent, high-energy-density hydrogen solutions. The U.S. Army's first hydrogen nanogrid at White Sands Missile Range validates 24/7 off-grid surveillance power and establishes a blueprint for broader base deployment. Soldier-portable targets call for over 1,000 Wh/kg energy densities at 0.1-3 kW, readily achievable with nickel-based alkaline stacks dispensing with precious metals. European forces mirror this trend, evidenced by Bundeswehr orders for off-grid units. Resultant near-term demand adds meaningful volume to the alkaline fuel cells market and de-risks manufacturers' scale-up plans.

CO2-Induced Electrolyte Poisoning Limits Deployment Flexibility

Potassium hydroxide electrolytes react with atmospheric CO2 to form carbonate salts, lowering ionic conductivity and cutting efficiency over time. High-purity hydrogen and scrubbing hardware add cost and complexity, discouraging deployment in CO2-rich industrial settings. Mitigation through membrane innovations is promising yet remains nascent, constraining near-term addressable volume.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Green Ammonia Bunkering Needs

- Stranded-Renewable Integration at Remote Mines

- Short Stack Life Compared with PEM Technology

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Static units captured 63.7% of 2025 revenue as telecom, microgrid, and industrial users valued low cost per kilowatt and multi-day autonomy. Verizon's national cell-tower program illustrates how diesel displacement creates recurring demand for hydrogen cartridges and service spares. Portable and mobile systems, although smaller, are advancing at 27.3% CAGR as militaries procure silent power below 5 kW. A 2025 U.S. Special Operations Command order for 500 units highlights rising tactical adoption.

Lighter composite vessels halve hydrogen weight, and integrated pumps shrink balance-of-plant footprints, enabling 1-3 kW packs under 20 kg that deliver 48-72 h runtime. Commercial users, film crews, and emergency responders value low noise and rapid refueling. Static installations will still command the bulk of the alkaline fuel cells market through 2031 because large-scale backup outspends portable volumes, yet mobile growth signals diversification beyond infrastructure.

Geography Analysis

North America generated 37.4% of 2025 revenue, buoyed by USD 3 kg-1 hydrogen production credits and Department of Defense contracts. Gulf Coast hubs leverage repurposed gas pipelines, while Canada's remote mines substitute diesel at USD 2 L-1 parity. Mexico lags but may piggyback on cross-border hydrogen trade as U.S. production scales.

Europe is the fastest-growing region at 26.6% CAGR to 2031, powered by REPowerEU, the EUR 9 billion German hydrogen budget, and port-side ammonia cracking for logistics hubs. The Renewable Energy Directive III sets binding RFNBO quotas that secure long-term offtake, stabilizing the alkaline fuel cells market. Nordic hydropower offers low-carbon hydrogen at competitive cost, driving early adoption in datacenters and ferry fleets.

Asia-Pacific growth is uneven. Japan and South Korea subsidize residential fuel cells, yet alkaline chemistries stay focused on backup duty. Australia and Chile replicate Canadian mine microgrids, while Middle East ports explore AFC auxiliary units tied to solar-linked ammonia exports. South America's Chilean roadmap targets 25 GW of electrolyzers by 2030, implying downstream fuel-cell balancing demand.

- AFC Energy plc

- GenCell Ltd.

- Elcogen AS

- FuelCell Energy Inc.

- Plug Power Inc.

- Ballard Power Systems

- Ceres Power Holdings

- PHMatter LLC

- Apollo Energy Systems

- Next Hydrogen Solutions

- EvolOH Inc.

- Zhangjiagang Horizon Fuel Cell

- Nedstack Fuel Cell Technology

- Intelligent Energy Ltd.

- AlkaMem Ltd.

- Doosan Fuel Cell

- Siemens Energy AG

- Toshiba Energy Systems

- SFC Energy AG

- Johnson Matthey plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Declining electrolyzer costs

- 4.1.2 Growing military demand for silent power

- 4.1.3 Rise of green ammonia bunkering needs

- 4.1.4 Stranded-renewable integration at remote mines

- 4.2 Market Restraints

- 4.2.1 CO2-induced electrolyte poisoning

- 4.2.2 Short stack life vs PEMFC

- 4.2.3 Nickel price volatility impact on electrode costs

- 4.3 Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Static Alkaline Fuel Cells

- 5.1.2 Mobile/Portable Alkaline Fuel Cells

- 5.2 By Power Output

- 5.2.1 Up to 5 kW

- 5.2.2 5 to 50 kW

- 5.2.3 Above 50 kW

- 5.3 By Application

- 5.3.1 Military and Defense

- 5.3.2 Spacecraft and Launch Systems

- 5.3.3 Backup and Remote Power

- 5.3.4 Portable Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AFC Energy plc

- 6.4.2 GenCell Ltd.

- 6.4.3 Elcogen AS

- 6.4.4 FuelCell Energy Inc.

- 6.4.5 Plug Power Inc.

- 6.4.6 Ballard Power Systems

- 6.4.7 Ceres Power Holdings

- 6.4.8 PHMatter LLC

- 6.4.9 Apollo Energy Systems

- 6.4.10 Next Hydrogen Solutions

- 6.4.11 EvolOH Inc.

- 6.4.12 Zhangjiagang Horizon Fuel Cell

- 6.4.13 Nedstack Fuel Cell Technology

- 6.4.14 Intelligent Energy Ltd.

- 6.4.15 AlkaMem Ltd.

- 6.4.16 Doosan Fuel Cell

- 6.4.17 Siemens Energy AG

- 6.4.18 Toshiba Energy Systems

- 6.4.19 SFC Energy AG

- 6.4.20 Johnson Matthey plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment