PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062473

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062473

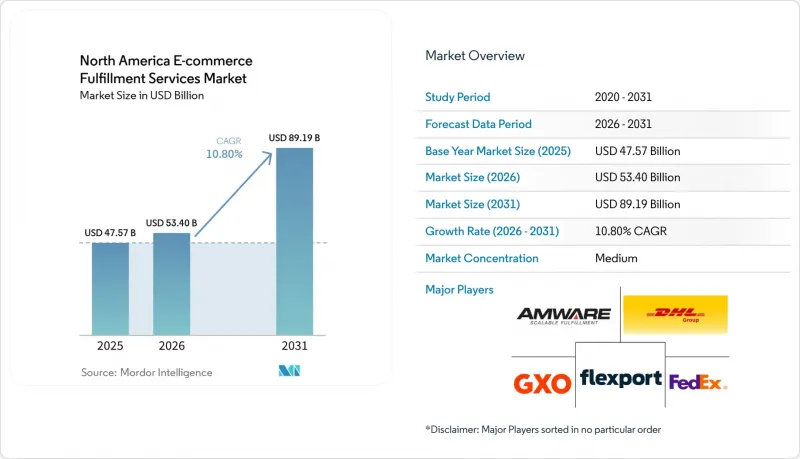

North America E-commerce Fulfillment Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america e-commerce fulfillment services market size is projected to grow from USD 47.57 billion in 2025 to USD 53.4 billion in 2026, and then to USD 89.19 billion by 2031, registering a 10.8% CAGR between 2026 and 2031.

Robust demand stems from social-commerce monetization, subscription-box standardization, and omni-channel orchestration that together redefine how brands position inventory and serve shoppers. This report is Segmented by Service Type (Warehousing and Storage, and More), by Fulfillment Model (In-House, Third-Party, and More), by Sales Channel (Direct-To-Consumer, and More), by Enterprise Size (SMEs, Large Enterprises), by End-Use Industry (Foods and Beverages, and More), and by Country (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America E-commerce Fulfillment Services Market Trends and Insights

Social-Commerce Boom Spawning Micro-Batch DTC Fulfillment Demand

Micro-batch product drops on TikTok Shop and Instagram Checkout generate 500-2,000 orders in only a few hours, so fulfillment partners must allocate labor dynamically and maintain real-time inventory views to protect campaign momentum. Speed now outweighs volume, rewarding providers that can toggle between high-throughput waves and specialty work cells inside the same facility. Direct connections between warehouse software and social-commerce APIs shorten confirmation cycles and feed accurate status data back into influencer streams. Facilities that master this cadence enjoy premium fees for rapid pick-to-ship service even at low batch sizes, cementing micro-batch fulfillment as a long-term differentiator.

Subscription-Box Economy Creating Predictable Recurring Volumes

Subscription shipments, accounted for USD 22.7 billion, give operators 30-90 day volume visibility, letting them pre-position inventory and negotiate carrier tiers with certainty. Retention levels of 70-85% keep month-to-month volume swings below 10%, far steadier than mainstream e-commerce. Specialized lines handle kitting and personalization without sacrificing cadence, saving 15-20% on labor versus traditional wave picking. These economics spur purpose-built subscription facilities that trade peak-season flexibility for recurring flow optimization, carving a defensible niche.

Packaging-Waste Legislation Driving Up Eco-Material Spend

Packaging waste legislation is significantly increasing fulfillment costs due to new EPR (Extended Producer Responsibility) rules that tie fees to packaging type and weight. These regulations are pushing operators toward costlier materials, such as paper or compostable mailers, while also requiring detailed compliance reporting. Providers must either absorb these rising material and administrative expenses or pass them on to clients, with smaller operators being disproportionately affected due to their lack of purchasing scale and compliance resources. Coastal and cross-border networks face additional hurdles, contending with climate mandates and Canadian EPR requirements.

Other drivers and restraints analyzed in the detailed report include:

- Federal and State Tax Credits Accelerating Cold-Chain FC Build-Outs

- Returns-Analytics Platforms Turning Reverse Logistics into Profit Centers

- SKU Proliferation Inflating Inventory Carrying and Slotting Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shipping services represented 42.74% of the North America e-commerce fulfillment services market size in 2025, highlighting the decisive weight of final-mile performance on shopper loyalty. Bundling of warehousing, kitting, and shipping is forecast to record a 13.83% CAGR as brands favor unified dashboards over multiple vendor interfaces.

Integrated contracts reduce data silos, give a single escalation path, and support network-wide KPIs that appeal to omnichannel retailers. Providers with proprietary cloud platforms can upsell analytics-based improvements and lock in multi-year renewals, shifting competition from per-parcel pricing to outcome guarantees.

Third-party fulfillment kept 60.56% of the North America e-commerce fulfillment services market share in 2025 by offering variable cost and instant scale. Dropshipping, however, is projecting a 21.98% CAGR because tariff reforms eliminated de minimis relief and penalized overseas direct imports.

Brands lean on the United States-based dropship inventories to preserve fast delivery while avoiding punitive duties, creating room for 3PLs that aggregate inventory for hundreds of micro-brands. Hybrid models combine owned DCs for core SKUs with third-party dropship for long-tail items, spreading fixed costs and maintaining breadth without capital lockup.

List of Companies Covered in this Report:

- Amware Fulfillment

- DHL Group

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Flexport

- Flowspace

- GoBolt

- GXO Logistics

- Ingram Micro Commerce

- Manifest.eco

- Quiet Platforms (Gap Inc.)

- Radial Inc.

- Red Stag Fulfillment

- Selery Fulfillment

- ShipBob

- Shipfusion

- ShipMonk

- ShipNetwork

- Shopify Fulfillment Network

- Xpdel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Social-Commerce Boom Spawning Micro-Batch DTC Fulfillment Demand

- 4.2.2 Subscription-Box Economy Creating Predictable Recurring Volumes

- 4.2.3 Federal and State Tax Credits Accelerating Cold-Chain FC Build-Outs

- 4.2.4 Returns-Analytics Platforms Turning Reverse Logistics into Profit Centers

- 4.2.5 Omni-Channel BOPIS and Ship-from-Store Orchestration Lifting FC Throughput

- 4.2.6 Autonomous Mobile Robots (AMRs) Slashing Pick-Time and Labor Reliance

- 4.3 Market Restraints

- 4.3.1 Packaging-Waste Legislation Driving up Eco-Material Spend

- 4.3.2 SKU Proliferation Inflating Inventory Carrying and Slotting Complexity

- 4.3.3 Rising Cyber-Attacks on WMS/APIs Disrupting Order Flows

- 4.3.4 Cross-Border Customs Frictions Slowing Canada-United States Parcel Velocity

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Value / Supply-Chain Analysis

- 4.6 Technological Innovations in the Industry

- 4.7 Government Regulations and Policies

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Warehousing and Storage Fulfilment Services

- 5.1.2 Bundling Fulfilment Services

- 5.1.3 Shipping Fulfilment Services

- 5.1.4 Other Niche / Value-added Services

- 5.2 By Fulfilment Model

- 5.2.1 In-house Fulfilment

- 5.2.2 Third-Party Fulfilment (3PL)

- 5.2.3 Dropshipping

- 5.2.4 Hybrid Fulfilment

- 5.3 By Sales Channel

- 5.3.1 Direct-to-Consumer (D2C)

- 5.3.2 Business-to-Consumer (B2C Marketplace)

- 5.3.3 Business-to-Business (B2B)

- 5.4 By Enterprise Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By End-Use Industry

- 5.5.1 Foods and Beverages

- 5.5.2 Personal and Household Care

- 5.5.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.5.4 Furniture and Home Decor

- 5.5.5 Electronics and Household Appliances

- 5.5.6 Other Products

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Amware Fulfillment

- 6.4.2 DHL Group

- 6.4.3 FedEx

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 Flexport

- 6.4.6 Flowspace

- 6.4.7 GoBolt

- 6.4.8 GXO Logistics

- 6.4.9 Ingram Micro Commerce

- 6.4.10 Manifest.eco

- 6.4.11 Quiet Platforms (Gap Inc.)

- 6.4.12 Radial Inc.

- 6.4.13 Red Stag Fulfillment

- 6.4.14 Selery Fulfillment

- 6.4.15 ShipBob

- 6.4.16 Shipfusion

- 6.4.17 ShipMonk

- 6.4.18 ShipNetwork

- 6.4.19 Shopify Fulfillment Network

- 6.4.20 Xpdel

7 Market Opportunities and Future Outlook