PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062479

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062479

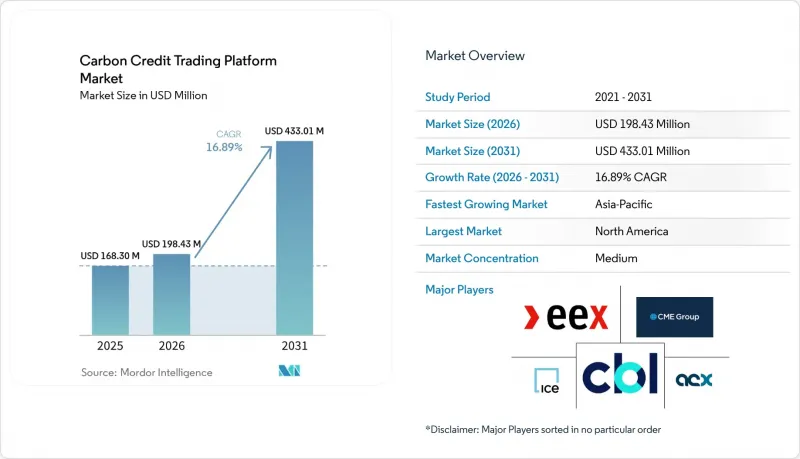

Carbon Credit Trading Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the carbon credit trading platform market size is expected to grow from USD 168.30 million in 2025 to USD 198.43 million in 2026 and is forecast to reach USD 433.01 million by 2031 at 16.89% CAGR over 2026-2031.

This report is Segmented by Type (Voluntary, Compliance), Application (Renewable Energy, Reforestation/Afforestation, Carbon Capture and Storage, Other Applications), End-User (Corporates, Governments, Individuals), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Carbon Credit Trading Platform Market Trends and Insights

Escalating Corporate Net-Zero Commitments

Microsoft doubled its 2024 offtake by contracting 45 million tCO2e in 2025 across 21 suppliers, including a 2.85 million-ton soil-carbon deal with Indigo Ag priced at USD 60-80 per ton over 12 years . Similar multi-year structures adopted by Salesforce and other Fortune 500 firms create a predictable order flow that platforms can bundle into standardized futures, differentiating high-integrity removals from avoidance credits. Science-Based Targets Initiative guidance now accepts only removals for neutralization, forcing platforms to embed granular credit tagging and automated retirement. Long-dated contracts also improve project bankability, crowding capital into engineered solutions such as direct air capture. This steady procurement pipeline lifts visibility for the carbon credit trading platform market.

Expanding Compliance Carbon Pricing Schemes

China will add steel, cement, and aluminum to its ETS by 2027, bringing 1,500 entities and 3 billion tCO2e under absolute caps. Japan's GX-ETS went live in 2026, South Korea began K-ETS Phase 4, and India's pilot scheme is underway, forming a pan-Asian pricing corridor that platforms must stitch together. ASEAN members signed a Common Carbon Framework to harmonize accounting, while Indonesia considers a bilateral linkage with China's ETS. These developments lift compliance liquidity, narrow regional arbitrage, and stimulate cross-listed products. Standard-setting bodies such as the Integrity Council for the Voluntary Carbon Market are quickly becoming prerequisites for listing, raising quality and integration requirements.

High Price Volatility of Carbon Credits

Spot avoidance offsets crashed below USD 5 per ton in 2024 after REDD+ integrity probes, then rebounded in 2025 as differentiated pricing emerged . CORSIA-eligible supply remains tight, keeping prices above USD 15, while EU ETS allowances swung between EUR 70 and EUR 115 in 2025. Platforms struggle to seed deep futures markets because standardized contracts are still nascent and market-maker incentives are low. Buyers with multi-year neutrality goals therefore face hedging gaps, dampening near-term adoption and tempering growth in the carbon credit trading platform market.

Other drivers and restraints analyzed in the detailed report include:

- Increased Investor Demand for ESG Products

- Technological Advancements in Digital MRV & Blockchain

- Rising Scrutiny of Additionality & Permanence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compliance venues generated 77.8% of the carbon credit trading platform market share in 2025, buoyed by the EU ETS, China's national ETS, and North American cap-and-trade programs. The EU's Market Stability Reserve withdrew 275 million allowances in 2024, while maritime inclusion from 2026 adds another 90 million tCO2e obligation. California, RGGI, and South Korea collectively cap over 2 billion tons, underpinning recurring auction settlement traffic. Voluntary carbon market platforms are projected to experience significant growth through 2031, driven by corporate buyers' increasing focus on high-integrity carbon removal solutions. Article 6 bilateral linkages and selective CORSIA eligibility blur lines between regimes, demanding unified settlement rails. Tokenized voluntary credits provide new liquidity, though oracle and regulatory hurdles dampen capital markets participation.

Geography Analysis

North America controlled 36.2% of 2025 revenue, led by California's Cap-and-Trade and a Washington-Quebec draft linkage designed to narrow allowance price gaps. Canada's federal backstop hits CAD 170 (USD 125) in 2030, catalyzing forestry offsets, while Mexico reviews its USD 3 tax to align with USMCA.

Asia-Pacific is the fastest-growing region, forecast at 22.3% CAGR to 2031. China's ETS will cover heavy industry by 2027 and could trade up to 11 billion tCO2e by 2030. Southeast Asia recorded 284 projects issuing 171.5 million tCO2e by April 2025, 73% from nature-based solutions. Japan, South Korea, and India add momentum, while EU CBAM pressures exporters to adopt internal pricing, funneling credits onto regional platforms.

Europe remains the regulatory bellwether. EU ETS auctions generated EUR 38.8 billion (USD 45.15 billion) in 2024, and maritime emissions add fresh demand from 2026. The U.K. negotiates potential relinking, Brazil's voluntary REDD+ projects feed global supply, and Gulf states explore sector-specific schemes, signaling expanding geographic diversity for the carbon credit trading platform market.

- Xpansiv

- AirCarbon Exchange (ACX)

- Climate Impact X

- CME Group Inc.

- Intercontinental Exchange (ICE)

- European Energy Exchange (EEX)

- Carbon Trade Exchange (CTX)

- Nasdaq

- Toucan

- Verra Registry

- Gold Standard

- ClearBlue Markets

- South Pole

- Flowcarbon

- Patch

- Regreener

- Carbonplace

- Thallo

- Cloverly

- IncubEx

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Corporate Net-Zero Commitments

- 4.2.2 Expanding Compliance Carbon Pricing Schemes

- 4.2.3 Increased Investor Demand for ESG Products

- 4.2.4 Technological Advancements in Digital MRV & Blockchain

- 4.2.5 Integration of Carbon Credits into Consumer Loyalty Platforms

- 4.2.6 Tokenization of Nature-Based Assets Enabling Micro-Transactions

- 4.3 Market Restraints

- 4.3.1 High Price Volatility of Carbon Credits

- 4.3.2 Lack of Global Standardization & Fragmented Regulations

- 4.3.3 Rising Scrutiny of Additionality & Permanence by Rating Agencies

- 4.3.4 Limited On-Chain Liquidity for Large Block Trades

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Voluntary Carbon Market Platforms

- 5.1.2 Compliance Carbon Market Platforms

- 5.2 By Application

- 5.2.1 Renewable Energy

- 5.2.2 Reforestation/Afforestation

- 5.2.3 Carbon Capture and Storage

- 5.2.4 Other Applications

- 5.3 By End-User

- 5.3.1 Corporates

- 5.3.2 Governments

- 5.3.3 Individuals

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Xpansiv

- 6.4.2 AirCarbon Exchange (ACX)

- 6.4.3 Climate Impact X

- 6.4.4 CME Group Inc.

- 6.4.5 Intercontinental Exchange (ICE)

- 6.4.6 European Energy Exchange (EEX)

- 6.4.7 Carbon Trade Exchange (CTX)

- 6.4.8 Nasdaq

- 6.4.9 Toucan

- 6.4.10 Verra Registry

- 6.4.11 Gold Standard

- 6.4.12 ClearBlue Markets

- 6.4.13 South Pole

- 6.4.14 Flowcarbon

- 6.4.15 Patch

- 6.4.16 Regreener

- 6.4.17 Carbonplace

- 6.4.18 Thallo

- 6.4.19 Cloverly

- 6.4.20 IncubEx

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment