PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063239

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063239

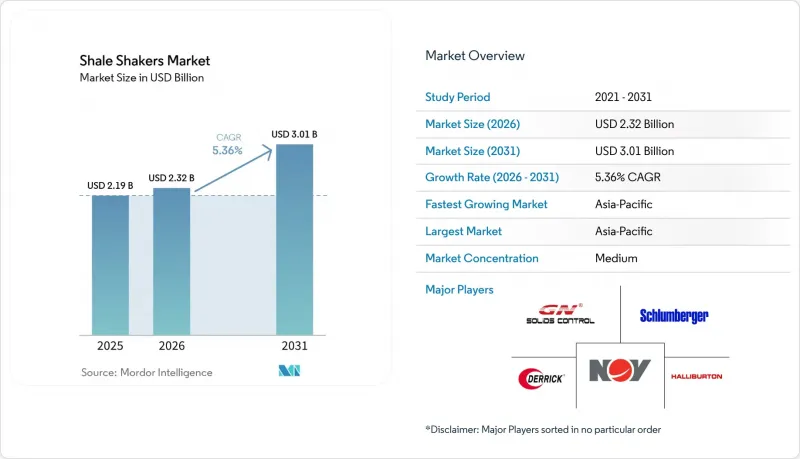

Shale Shakers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the shale shakers market size is projected to be USD 2.19 billion in 2025, USD 2.32 billion in 2026, and reach USD 3.01 billion by 2031, growing at a CAGR of 5.36% from 2026 to 2031.

This report is Segmented by Product Type (Linear Motion, and More), Technology (Single Deck, Double Deck, Triple Deck), Drive System (Electrically Driven, Belt Driven), Installation (Newly Installed, Retrofitted), Application (Coal Cleaning, and More), and Geography (North America, Europe, Asia Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Shale Shakers Market Trends and Insights

Surging Horizontal and Directional Shale Drilling Activity

Haynesville gas-directed drilling touched 64 rigs in February 2026 as LNG export expansions and data-center power demand boosted gas targets by 1.2 billion cubic feet per day for 2026 and 1.6 billion cubic feet per day for 2027 . Each horizontal well generates up to 2,000 barrels of drilling fluid that must pass across shale shakers before reuse. Longer laterals averaging 10,000-12,000 feet raise solids loading by 40%, forcing operators to shift from single-deck to triple-deck equipment to maintain 800 gallons-per-minute circulation. U.S. pad-drilling expertise is migrating to Argentina's Vaca Muerta and Saudi Arabia's Jafurah, where portable high-throughput decks process 28 liters per second at 7.5 G-force. Autonomous g-force control that modulates vibration amplitude based on downhole telemetry is reducing screen blinding by 20% and extending mesh life to 55 hours, lowering consumable cost by USD 8,000 per well. The confluence of higher well counts, longer laterals, and automation adds 1.5 % to the CAGR.

Rising Offshore Ultra-Deepwater Wells With High-G Mud Programs

Chevron's Anchor project came on-stream in 2024 at 20,000 psi wellhead pressure, relying on synthetic-based muds that impose 6.5 G loads on decks . Conventional linear-motion units struggle to remove sub-10-micron barite without losing fluid, prompting uptake of balanced elliptical shakers that safeguard 200-mesh screens while achieving 80% solids removal. ADNOC Drilling ordered two jack-up rigs and three island rigs in 2025, all specified with AI-enabled triple-deck shakers designed for 18-pound-per-gallon mud. Arabian Drilling reactivated three rigs the same year, each fitted with triple-deck units to handle high-pressure reservoirs. Growing deepwater campaigns in Brazil and West Africa will translate this practice globally, contributing 0.8 % to long-term growth.

Crude-Price Volatility Curbing New Rig CAPEX

West Texas Intermediate averaged USD 62 per barrel in early 2026, prompting North American independents to trim drilling budgets and rely on 40% productivity gains to meet output targets. Fewer greenfield rigs translate to lower demand for newly installed shakers, even though retrofit work partially offsets the dip. Operators defer purchases until sustained prices climb above USD 70, creating a 0.9 percentage-point drag on CAGR through 2028.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Cuttings-Discharge Regulations

- Rig Digital-Twin Adoption Enabling Predictive Shaker Maintenance

- High Ownership Cost Versus Shaker-Less Vacuum Filtration Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Linear-motion designs generated 68.6% of 2025 revenue and will grow at 5.6% annually through 2031. The segment benefits from aggressive unidirectional vibration of 0.25 inches at up to 4 G that propels sticky Haynesville gumbo across the screen. Field trials showed that NOV's Brandt Alpha line delivered 37% waste reduction and saved USD 45,000 per pad in the Midland Basin. Balanced elliptical motion is favored offshore to protect fine screens against 6.5 G mud programs. Circular designs persist in coal cleaning where simplicity matters.

The shale shakers market for linear-motion units is projected to grow steadily through 2031, driven by their extensive use in conventional drilling and high-volume solids control operations. The introduction of autonomous G-force control systems is increasing screen life from approximately 40 hours to around 55 hours, enabling operators to lower consumable costs by nearly USD 8,000 per well. Adherence to API RP 13C standards at D100 cut points of 75-150 microns continues to enhance procurement preferences in Middle Eastern drilling projects, solidifying the segment's strong role in overall shale shaker demand.

Single-deck units remained most numerous in 2025, with 54.2% installs due to low upfront cost. Triple-deck platforms, however, post the fastest 6.3% CAGR because they integrate coarse, intermediate, and fine screening inside one frame, erasing the need for separate desanders and desilters.Brightway's design trims footprint by 40% and halves rig-up time.

Triple-deck shale shaker systems are projected to experience significant growth through 2031, driven by operators' focus on adhering to stringent North Sea zero-discharge regulations, which mandate residual oil content below 1%. The integration of digital-twin sensors across multiple decks enhances operational data collection, facilitating machine-learning-based predictions of bearing wear and improving overall equipment uptime. While single-deck units remain prevalent in coal and mining applications, triple-deck configurations are increasingly favored for high-specification drilling rigs in North America.

Geography Analysis

North America controlled 40.1% of the shale shakers market revenue in 2025 and is projected to grow at 6.2% annually to 2031. Haynesville rig counts rose to 64 by February 2026, and Permian totals held near 255 even during price softness. Comstock Resources plans 43 Haynesville wells in 2026, each specifying high-throughput triple-deck units. Tightening Colorado and Alberta noise codes are driving VFD retrofits that align with digital-twin uptime programs at Precision Drilling, reducing downtime by 30%.

The Middle East shows the strongest spending momentum. ADNOC placed more than USD 1.9 billion in rig orders during 2025 that mandate AI-enabled solids control, while Saudi operators keep capacity at 13 million barrels per day. Triple-deck shakers with PMAC motors and API RP 13C mesh are now standard in new Saudi and UAE fleets. Europe's North Sea, constrained by OSPAR zero-discharge rules, adopts closed-loop systems with vacuum dewatering; residual oil levels under 1% are now routine on Norwegian Continental Shelf wells.

Asia-Pacific's growth is steadier. Chinese coal washing maintains demand for cost-focused shakers from GN Solids Control, yet national renewable targets temper long-term volumes. India's deeper Krishna-Godavari wells require higher throughput, but overall rig counts keep the region at one-third the North American size. South America, led by Brazil's pre-salt and Argentina's shale, is adopting North American pad-drilling methods that rely on portable equipment rated 28 liters per second at 7.5 G, although currency risks delay some orders.

- Derrick Equipment Company

- NOV-BRANDT

- Halliburton

- Schlumberger

- GN Solids Control

- Baker Hughes

- Elgin Separation Solutions

- KEMTRON Technologies

- M-I SWACO

- Aipu Solids Control

- Tri-Flo International

- TR Solids Control

- H-Screening Separation

- Shale Tech Solutions

- Kem-Terra

- DC Solid Control

- ShengJia Machinery

- Derrick Fine Mesh

- KOSUN Machinery

- DFE

- Southwest Petroleum University Tech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging horizontal & directional shale drilling activity

- 4.2.2 Rising offshore ultra-deepwater wells with high-G mud programs

- 4.2.3 Stringent cuttings-discharge regulations (e.g., North Sea OSPAR)

- 4.2.4 Rig digital-twin adoption enabling predictive shaker maintenance

- 4.2.5 Adoption of autonomous g-force control to optimise ROP

- 4.2.6 Lithium-rich geothermal wells requiring ultra-fine cuttings control

- 4.3 Market Restraints

- 4.3.1 Crude-price volatility curbing new rig CAPEX

- 4.3.2 High ownership cost vs. shaker-less vacuum filtration alternatives

- 4.3.3 API compliant mesh supply bottlenecks due to rare-earth alloys

- 4.3.4 ESG scrutiny on vibration-induced deck noise at well sites

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Linear Motion Shale Shakers

- 5.1.2 Balanced Elliptical Motion Shale Shakers

- 5.1.3 Circular Motion Shale Shakers

- 5.2 By Technology

- 5.2.1 Single Deck

- 5.2.2 Double Deck

- 5.2.3 Triple Deck

- 5.3 By Drive System

- 5.3.1 Electrically Driven

- 5.3.2 Belt Driven

- 5.4 By Installation

- 5.4.1 Newly Installed

- 5.4.2 Retrofitted

- 5.5 By Application

- 5.5.1 Coal Cleaning

- 5.5.2 Oil and Gas Drilling

- 5.5.3 Mining

- 5.5.4 Chemical and Petrochemical

- 5.5.5 Plastics

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Derrick Equipment Company

- 6.4.2 NOV-BRANDT

- 6.4.3 Halliburton

- 6.4.4 Schlumberger

- 6.4.5 GN Solids Control

- 6.4.6 Baker Hughes

- 6.4.7 Elgin Separation Solutions

- 6.4.8 KEMTRON Technologies

- 6.4.9 M-I SWACO

- 6.4.10 Aipu Solids Control

- 6.4.11 Tri-Flo International

- 6.4.12 TR Solids Control

- 6.4.13 H-Screening Separation

- 6.4.14 Shale Tech Solutions

- 6.4.15 Kem-Terra

- 6.4.16 DC Solid Control

- 6.4.17 ShengJia Machinery

- 6.4.18 Derrick Fine Mesh

- 6.4.19 KOSUN Machinery

- 6.4.20 DFE

- 6.4.21 Southwest Petroleum University Tech

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment