PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063261

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063261

Clean Hydrogen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

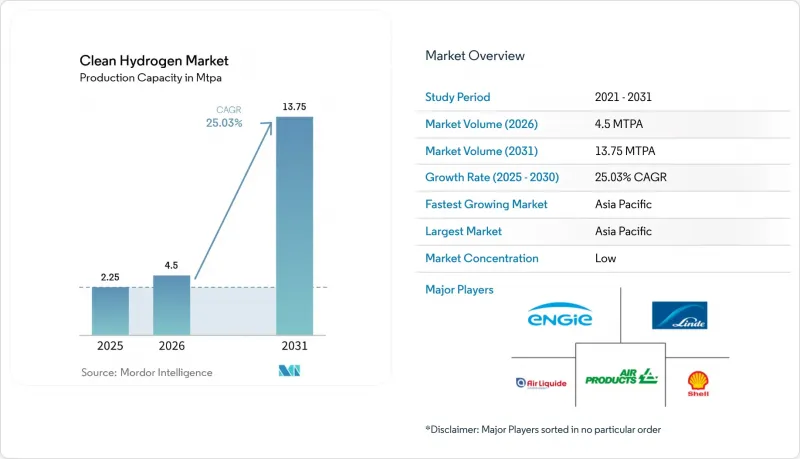

According to Mordor Intelligence, the clean hydrogen market size in terms of production capacity is expected to grow from 2.25 MTPA in 2025 to 4.5 MTPA in 2026 and is forecast to reach 13.75 MTPA by 2031 at 25.03% CAGR over 2026-2031.

This report is Segmented by Production Method (Green Hydrogen, Blue Hydrogen, Turquoise Hydrogen, Others), Electrolyzer Technology (Alkaline, PEM, and More), Delivery Form (Compressed Gas, Liquid Hydrogen, and More), Application (Transportation, Industrial, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Clean Hydrogen Market Trends and Insights

Soaring electrolyzer manufacturing over-capacity drives price collapse post-2026

Global nameplate electrolyzer capacity hit 61-63 GW per year in 2025, but only 2.15 GW was operating, creating an oversupply that forced European alkaline prices down to USD 2,407 per kilowatt and PEM to USD 2,547per kilowatt. Chinese vendors control more than half of the installed factory capacity and are exporting modules below cost to maintain their share, impairing Western manufacturers' margins. As hardware deflates, the unsubsidized levelized cost of green hydrogen is projected to fall toward USD 1.50-2.50 per kilogram in high-solar regions by 2030, overtaking blue hydrogen ranges burdened by escalating carbon-capture charges. The price war is accelerating final-investment decisions across the Middle East and India, two locations with abundant low-priced renewable electricity. However, plummeting module prices are squeezing working-capital lines for smaller OEMs, raising the prospect of sector consolidation over the next two years.

IRA-style production tax credits replicated in EU, India, Brazil

The U.S. Inflation Reduction Act's 45V credit of up to USD 3 per kilogram for low-carbon hydrogen has become a global benchmark that Europe's Hydrogen Bank, India's SIGHT scheme, and Brazil's pending incentive framework now mirror. These subsidies establish predictable revenue floors, permitting developers to secure non-recourse debt at lower spreads. India alone earmarked USD 2.4 billion for electrolysis manufacturing and production incentives, triggering a 1 MTPA green-ammonia FID by AM Green. Yet an accelerated sunset clause in the One Big, Beautiful Bill Act, which requires U.S. projects to start construction before January 1, 2028, prompted cancellations exceeding 4.9 MTPA in 2025, underscoring persistent policy risk.

2030-onwards renewable-power curtailment penalties (grid fees)

Germany curtailed 8.2 TWh of green power in 2024 and is introducing time-of-use tariffs that charge electrolyzers USD 5.8-17.4/MWh during surplus periods, undercutting assumptions of zero-cost energy. Similar dynamic-fee pilots are underway in Spain and Denmark. Because alkaline electrolyzers need 5-15 minutes to ramp, they cannot absorb volatility as quickly as lithium-ion storage, prompting regulators to favor batteries for grid balancing. EU rules also force hourly matching between renewable output and hydrogen production, limiting developers' ability to arbitrage cheap imports across bidding zones. From 2030, grid penalties could add USD 0.20-0.50/kg to hydrogen costs, eroding competitiveness versus blue hydrogen in gas-rich regions.

Other drivers and restraints analyzed in the detailed report include:

- Rise of green-premium procurement mandates by steel and ammonia buyers

- Development of H2 pipeline corridors in EU, U.S. Gulf and Middle East

- CCS cost inflation undermines blue-H2 competitiveness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blue hydrogen retained 68.5% of the clean hydrogen market share in 2025, underscoring the early-mover advantage of reforming natural gas paired with carbon capture. Yet the green pathway is on a faster cadence, expanding at 34.6% CAGR through 2031 as falling electrolyzer costs compress the delivered price gap to less than USD 0.20 per kilogram in high-solar regions. That swing reduces the blue premium that once placed steam-reforming projects ahead on project finance models, especially where government incentives for captured carbon have begun to taper. Developers, therefore, continue to break ground on gigawatt-scale electrolysis clusters, such as the 219,000-tonne-per-year NEOM complex, which will anchor large export volumes into Asia.

From 2026 onward, the clean hydrogen market size attached to green projects eclipses blue in announced capacity, even though blue still dominates volumes in operation. CCS cost escalation, running from USD 50-100 per tonne in 2025 toward USD 80-150 per tonne by 2030, erodes blue's price edge, while renewable energy additions, land-leasing reforms, and tax credits speed up electrolysis pipelines. Turquoise hydrogen and biomass gasification has low share of the clean hydrogen market size because of unproven carbon monetization and logistics barriers. Unless CCS price curves flatten, policy risk is expected to dilute further blue project pipelines, opening room for green to become the reference pathway in procurement tenders.

Alkaline systems captured 58.9% of the clean hydrogen market size in 2025, benefiting from lower capital intensity and decades of deployment in the chlor-alkali industry. European module quotations slipped below USD 2,436 per kilowatt during 2025 as Chinese suppliers triggered a price war, widening their reach in export tenders. The PEM segment, however, is closing the gap, helped by iridium-loading reductions from 2-3 grams per kilowatt in 2020 to as low as 0.3-0.5 grams per kilowatt in 2025, cutting catalyst bills by more than 70%. Faster ramp rates and partial-load flexibility, reaching 10% of nameplate capacity in sub-second response, make PEM the preferred option for co-located wind-solar hybrids.

Solid-oxide electrolysis commands a smaller market share, yet pilot runs have logged 72% electrical efficiency and aim for stack-level efficiencies above 85% once industrial waste heat is harvested. That translates into a potential USD 0.30-0.80 per kilogram saving in markets where power costs exceed USD 40 per megawatt-hour, positioning SOEC for steel and ammonia complexes. Meanwhile, anion-exchange membrane prototypes promise PEM-like dynamics without noble metals, but lifetime validation past 40,000 hours is still lacking. Overall, the technology mix is tilting from cost-driven alkaline dominance toward a more balanced profile in which PEM and, later, SOEC carve out applications tied to flexible renewables and high-grade heat integration.

Geography Analysis

Asia-Pacific led with 43.7% of 2025 volumes and should post the highest regional CAGR at 27.4% through 2031. China alone commissioned 25 of the 59 global projects that came online in 2025, including Sinopec's 20,000-tonne-per-year Kuqa electrolyzer complex. India's National Green Hydrogen Mission, backed by USD 2.05 billion in incentives, has seeded more than 1 MTPA of committed capacity across ammonia and mobility pilots. Japan is building import infrastructure that targets 3 MTPA by 2030 and 20 MTPA by 2050, signalling a structural pull on regional exports. Across ASEAN, Indonesia and Vietnam eye low-cost hydropower sites, though execution hinges on port permitting and bankable offtake deals.

Europe accounted for a significant share of the 2025 output but faces challenges due to increasing renewable curtailment penalties and strict temporal matching regulations. Germany curtailed 8.2 TWh of green power in 2024 and is rolling out dynamic grid fees that add USD 0.20-0.50 per kilogram to hydrogen costs. Still, the continent is knitting a pipeline backbone: the 3,300 km SoutH2 Corridor and an 11,600 km first-phase Hydrogen Backbone by 2030. Major clusters in the Netherlands and Spain pair offshore-wind PPAs with 200-250 MW electrolyzers, anchoring refinery supply and export ambitions.

In North America, the U.S. Gulf Coast benefits from 1,000 miles of existing hydrogen pipelines and USD 1.2 billion in hub grants, but the accelerated 45V sunset forces projects to reach FID before 2028, triggering more than 4.9 MTPA of cancellations in 2025. Saudi Arabia's NEOM complex leverages solar resources to deliver green ammonia at USD 1.50-2.50 per kilogram, advancing the region as an export powerhouse. Brazil expects to finalize incentives in 2026 and focus on ammonia export corridors, while South Africa's platinum and iridium mines supply critical PEM catalysts, raising geopolitical stakes for material security.

- Air Liquide

- Linde plc

- Air Products

- Shell

- BP

- Engie

- Orsted

- Plug Power

- Nel ASA

- ITM Power

- Siemens Energy

- Thyssenkrupp Nucera

- Cummins

- Topsoe

- Kawasaki Heavy

- Hyundai Motor Group

- Toyota

- Mitsubishi Power

- Posco Future M

- ADNOC

- ACWA Power

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring electrolyser manufacturing over-capacity drives price collapse post-2026

- 4.2.2 IRA-style production tax credits replicated in EU, India, Brazil

- 4.2.3 Rise of "green-premium" procurement mandates by steel & ammonia buyers

- 4.2.4 Development of H2 pipeline corridors in EU, US Gulf & Middle East

- 4.2.5 Corporate PPAs bundling renewable power + H2 offtake

- 4.2.6 Break-through in solid-oxide electrolysis efficiency >85 % (lab-to-pilot)

- 4.3 Market Restraints

- 4.3.1 2030-onwards renewable power curtailment penalties (grid fees)

- 4.3.2 CCS cost inflation undermines blue-H2 competitiveness

- 4.3.3 Delay in global H2 certification interoperability

- 4.3.4 Geopolitical risk around critical minerals for PEM stacks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Policy Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Production Method

- 5.1.1 Green Hydrogen

- 5.1.2 Blue Hydrogen

- 5.1.3 Turquoise (Pyrolysis) Hydrogen

- 5.1.4 Others

- 5.2 By Electrolyzer Technology

- 5.2.1 Alkaline

- 5.2.2 PEM

- 5.2.3 Solid-Oxide

- 5.2.4 Anion-Exchange

- 5.3 By Delivery Form

- 5.3.1 Compressed Gas

- 5.3.2 Liquid Hydrogen

- 5.3.3 Ammonia

- 5.3.4 LOHC

- 5.4 By Application

- 5.4.1 Transportation (FCEV, Rail, Marine, Aviation)

- 5.4.2 Industrial (Ammonia Production, Methanol Production, Steelmaking, etc)

- 5.4.3 Power Generation

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Air Liquide

- 6.4.2 Linde plc

- 6.4.3 Air Products

- 6.4.4 Shell

- 6.4.5 BP

- 6.4.6 Engie

- 6.4.7 Orsted

- 6.4.8 Plug Power

- 6.4.9 Nel ASA

- 6.4.10 ITM Power

- 6.4.11 Siemens Energy

- 6.4.12 Thyssenkrupp Nucera

- 6.4.13 Cummins

- 6.4.14 Topsoe

- 6.4.15 Kawasaki Heavy

- 6.4.16 Hyundai Motor Group

- 6.4.17 Toyota

- 6.4.18 Mitsubishi Power

- 6.4.19 Posco Future M

- 6.4.20 ADNOC

- 6.4.21 ACWA Power

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment