PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063277

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063277

Automotive Communication Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

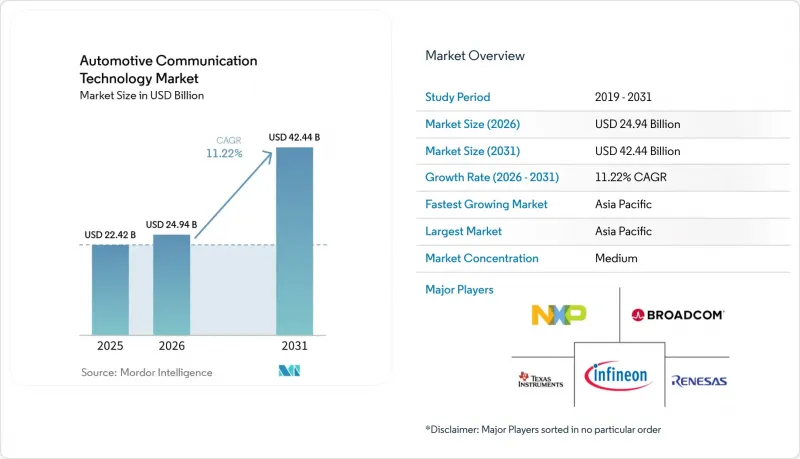

According to Mordor Intelligence, the automotive communication technology market size is expected to grow from USD 22.42 billion in 2025 to USD 24.94 billion in 2026 and is forecast to reach USD 42.44 billion by 2031 at an 11.22% CAGR over 2026-2031.

This report is Segmented by Bus Module (Local Interconnect Network (LIN), Controller Area Network (CAN), and More), Application (Powertrain, Body Control and Comfort, and More), Communication Type (Vehicle-To-Everything (V2X) and More), Vehicle Type, Propulsion Type, Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Communication Technology Market Trends and Insights

Rising Integration of Advanced Driver-Assistance Systems (ADAS)

Cameras, radar, and lidar arrays are scaling rapidly, and the data they generate exceeds what legacy buses can transport within safety-critical latency windows. Centralized domain controllers now fuse perception inputs in real time, pushing the automotive communication technology market toward Ethernet backbones that support time-sensitive networking. Global New Car Assessment protocols increasingly award points for automated steering features that require microsecond-level determinism, embedding communication performance directly into crash-test outcomes. Component makers reply with system-on-chip transceivers that combine CAN-XL, 10BASE-T1S, and hardware security accelerators on a single die. As ADAS becomes standard even in entry-level trims, bandwidth demand expands faster than average vehicle selling prices, making network efficiency pivotal to OEM margins.

Emergence of Zonal E/E Architectures Requiring Ethernet Backbones

Zonal designs collapse dozens of distributed electronic control units into a handful of regionally placed compute nodes. This re-layout shortens harnesses, simplifies power distribution, and concentrates cybersecurity defenses at a few network ingress points. Premium OEMs in Europe and North America have validated early zonal prototypes that reduce wiring mass by roughly one-third, improving energy efficiency in battery-electric vehicles. The architectural shift dovetails with the adoption of multi-gigabit Ethernet, as a single twisted pair can now carry both deterministic control traffic and infotainment streams. Suppliers that deliver switch silicon with built-in functional safety and time-aware shaping win design slots across multiple vehicle lines, catalyzing consolidation inside the automotive communication technology market.

High Cost and Complexity of Validating High-Speed Networks

Proving that a mixed-protocol vehicle network remains safe under electromagnetic stress and cyberattack involves time-consuming lab campaigns. OEMs must purchase specialized error-injection benches and retrain validation engineers unfamiliar with Ethernet determinism. Regulatory frameworks such as UN Regulation 155 add continuous threat-monitoring requirements, extending test scopes well past those of earlier CAN-centric programs. Smaller automakers face disproportionate cost burdens, which delay feature introductions and temporarily restrain volume growth in the automotive communication technology market. Collaborative validation hubs are emerging to share equipment loads, but best-practice harmonization remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Software-Defined Vehicles and OTA Communication

- Adoption of Time-Sensitive Networking (TSN) for Deterministic Automotive Ethernet

- Limited Supply of Automotive-Grade Multi-Gig PHY Semiconductors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Controller Area Network retained the largest 41.22% of the automotive communication technology market share in 2025, a testament to its entrenched presence in body and legacy powertrain domains. Automotive Ethernet is forecast to record the fastest CAGR of 12.84% through 2031, underscoring its role as the spine of next-generation zone controllers. Developers now integrate CAN-XL alongside 10BASE-T1S so that gateways can translate critical messages during staged migrations toward full Ethernet. This hybrid approach safeguards platform continuity and lets OEMs roll out advanced features without wholesale rewiring. Hardware vendors that supply mixed-protocol switches are therefore indispensable allies for cost-optimized platform roadmaps.

The coexistence of Ethernet and CAN reshapes supplier ecosystems inside the automotive communication technology market. Tier-1 system integrators must demonstrate determinism by combining time-aware shaping on Ethernet links with gateway buffering for CAN traffic. Test-equipment makers respond by bundling frame-preemption probes and CAN error-injection modules into single consoles, reducing laboratory complexity. Cybersecurity auditors also adjust: a zonal network permits firewalling at fewer ingress points, simplifying compliance with UN Regulation 155 yet raising the stakes for each gateway's resilience.

Powertrain communication commanded a 36.08% of the automotive communication technology market share in 2025, but safety and advanced driver-assistance systems are projected to lead growth with a 13.15% CAGR. This inversion springs from mandates for emergency steering and lane-keeping that require deterministic sensor fusion. Ethernet backbones with TSN scheduling ensure that perception data reaches actuation logic within microsecond windows, elevating communication performance to life-critical status. Suppliers race to embed TSN hardware blocks into microcontrollers to secure design wins ahead of regulation-driven cut-over dates. The resulting innovation loop positions ADAS networking as the bellwether for broader electronic-architecture change.

Convergence between external V2X feeds and on-board sensor suites is reshaping software stacks in the automotive communication technology market. Domain controllers once dedicated to camera fusion now parse certificate chains and threat telemetry from roadside units, blending cybersecurity with perception. Local road agencies pilot green-light priority schemes that rely on guaranteed packet-delivery windows, reinforcing demand for deterministic networks. As a corollary, powertrain engineers adopt Ethernet to synchronize regenerative braking and thermal subsystems with ADAS inputs, minimizing energy loss in electric vehicles.

Geography Analysis

Asia-Pacific commanded a 47.14% of the automotive communication technology market share in 2025 and is expected to expand at a 12.06% CAGR through 2031, propelled by China's large-scale vehicle-road-cloud pilots and South Korea's integration of cooperative intelligent transport systems into national crash tests. China's mandatory GB 44495 rule requires certificate-based V2X security and pushes OEMs toward Ethernet backbones, creating a vast domestic pipeline of opportunities. Japan's ministry-backed pilots feed technical feedback into procurement standards, accelerating supplier readiness. South Korea's dual-mode V2X platform eases transition pains by bridging cellular and DSRC vehicles. India's premium models begin to specify 100BASE-T1, foreshadowing gradual mainstream diffusion.

Europe and North America adopt a more coordinated, but slower, rollout under the umbrella of UN Regulations 155 and 156, which embed cybersecurity and software-update management into type-approval checklists. The FCC's decision to clear the 5.9 GHz band for cellular V2X removed spectrum uncertainty, permitting OEMs to finalize single-mode radio roadmaps. Germany's supplier base exerts outsized influence on IEEE working groups, injecting European latency and safety perspectives into global Ethernet standards. The United Kingdom follows UN regulations despite regulatory divergence elsewhere, preserving cross-channel parts interchangeability. North American test corridors, such as Michigan's open-road labs, provide real-world data that shorten validation cycles.

Emerging regions adopt imported electrical architectures rather than crafting bespoke standards, saving validation costs but deferring the implementation of localized feature sets. Brazil's assembly plants build on EU-spec platforms that already contain Ethernet gateways, while the United Arab Emirates mandates V2X only for premium limousine fleets. South African export hubs are integrating Ethernet to serve European destination markets, even though local buyers still favor basic CAN. Russian carmakers maintain CAN-FD compatibility to ensure eventual reintegration with Western supply chains. Across all non-core geographies, the automotive communication technology market grows via technology trickle-down rather than headline-grabbing pilot programs.

- NXP Semiconductors N.V.

- Broadcom Inc.

- Texas Instruments Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Qualcomm Incorporated

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Aptiv plc

- HARMAN International

- Vector Informatik GmbH

- Molex LLC (Koch Industries)

- TE Connectivity plc

- ON Semiconductor Corporation

- Analog Devices, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Integration of Advanced Driver-Assistance Systems (ADAS)

- 4.2.2 Increasing Demand for High-Bandwidth Infotainment

- 4.2.3 Emergence of Zonal E/E Architectures Requiring Ethernet Backbones

- 4.2.4 OEM Shift Toward Software-Defined Vehicles and OTA Communication

- 4.2.5 Stringent Emission and Safety Regulations Boosting Electronic Content

- 4.2.6 Adoption of Time-Sensitive Networking (TSN) for Deterministic Automotive Ethernet

- 4.3 Market Restraints

- 4.3.1 High Cost and Complexity of Validating High-Speed Networks

- 4.3.2 Limited Supply of Automotive-Grade Multi-Gig PHY Semiconductors

- 4.3.3 Cyber-Security Vulnerabilities in V2X Protocols

- 4.3.4 Legacy CAN/LIN and New Ethernet Interoperability Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Bus Module

- 5.1.1 Local Interconnect Network (LIN)

- 5.1.2 Controller Area Network (CAN)

- 5.1.3 FlexRay

- 5.1.4 Media-Oriented Systems Transport (MOST)

- 5.1.5 Automotive Ethernet

- 5.2 By Application

- 5.2.1 Powertrain

- 5.2.2 Body Control and Comfort

- 5.2.3 Infotainment and Communication

- 5.2.4 Safety and ADAS

- 5.3 By Communication Type

- 5.3.1 Vehicle-to-Vehicle (V2V)

- 5.3.2 Vehicle-to-Infrastructure (V2I)

- 5.3.3 Vehicle-to-Everything (V2X)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Propulsion Type

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Battery Electric Vehicle (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.5.5 Fuel-Cell Electric Vehicle (FCEV)

- 5.6 By Distribution Channel

- 5.6.1 Original Equipment Manufacturer (OEM)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 Spain

- 5.7.3.4 Italy

- 5.7.3.5 France

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 NXP Semiconductors N.V.

- 6.4.2 Broadcom Inc.

- 6.4.3 Texas Instruments Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 Robert Bosch GmbH

- 6.4.7 Continental AG

- 6.4.8 Denso Corporation

- 6.4.9 Qualcomm Incorporated

- 6.4.10 STMicroelectronics N.V.

- 6.4.11 Microchip Technology Inc.

- 6.4.12 Aptiv plc

- 6.4.13 HARMAN International

- 6.4.14 Vector Informatik GmbH

- 6.4.15 Molex LLC (Koch Industries)

- 6.4.16 TE Connectivity plc

- 6.4.17 ON Semiconductor Corporation

- 6.4.18 Analog Devices, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment