PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063292

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063292

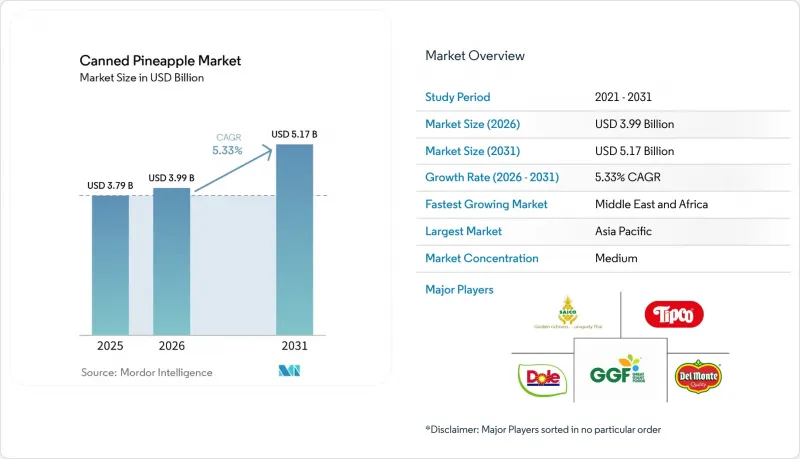

Canned Pineapple - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global canned pineapple market is anticipated to grow from USD 3.79 billion in 2025 to USD 3.99 billion in 2026, reaching USD 5.17 billion by 2031, with a CAGR of 5.33% during the forecast period from 2026 to 2031.

This report is Segmented by Product Form (Slices, Chunks, Tidbits, Crushed, Spears and Whole), Packaging Type (Cans, Cups and Jars, Others), Distribution Channel (Foodservice and Retail), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Both Value (USD) and Volume (Tons).

Global Canned Pineapple Market Trends and Insights

Demand for convenient and ready-to-eat fruit products

The increasing demand for convenient and ready-to-eat fruit products is driving the growth of the canned pineapple market. Consumers are prioritizing food options that require minimal preparation while offering extended shelf life, easy storage, and immediate consumption convenience. Canned pineapple aligns with these preferences by providing pre-processed, peeled, and ready-to-eat fruit products, which save preparation time and help reduce food waste. Factors such as busy lifestyles, urbanization, and a growing preference for quick meal solutions are further encouraging the adoption of packaged fruit products that can be easily integrated into daily diets. Moreover, canned pineapple ensures year-round availability and consistent quality, unaffected by seasonal variations, making it a reliable and accessible fruit option. The rising popularity of convenient pantry staples, combined with the demand for portable and easy-to-store food products, continues to support the global consumption of canned pineapple.

Consumer preference for long shelf-life food products

Increasing consumer preference for long shelf-life food products is a key factor driving the global canned pineapple market. Packaged food items that can be stored for extended periods without significant quality loss are gaining popularity, particularly due to the growing demand for convenient pantry staples and emergency food storage options. Canned pineapple provides extended usability, minimizes spoilage risk, and ensures year-round availability, making it an appealing choice for households seeking reliable fruit products with minimal storage challenges. According to Food Standards Australia New Zealand (FSANZ), canned foods with a shelf life exceeding two years do not require date marking . As long as the can remains intact, these products retain their long shelf life even at room temperature, underscoring the preservation benefits of canned food products.

Concerns regarding added sugar and preservatives

Concerns about added sugar and preservatives are significantly restraining the growth of the global canned pineapple market, as consumers increasingly prioritize healthier and more natural food options. Canned fruit products are often perceived as containing excessive sugar syrups, artificial preservatives, and processed ingredients, which can deter health-conscious consumers. Rising awareness of the health risks associated with high sugar consumption, such as obesity, diabetes, and other lifestyle-related conditions, further discourages the consumption of sweetened canned fruit products. The World Health Organization recommends that free sugars account for less than 10% of total daily energy intake for individuals consuming approximately 2,000 calories per day to maintain a healthy body weight. This growing emphasis on reducing sugar intake is driving consumers toward fresh fruits and minimally processed food alternatives, which are viewed as healthier and more natural options.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in canning and food preservation technologies

- Product innovations such as organic, no-added-sugar, and sustainably packaged

- High competition from frozen, dried, and fresh pineapple alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The slices segment accounted for a 46.81% value share of the global canned pineapple market in 2025, driven by strong consumer preference, convenience, visual appeal, and consistent product quality. Pineapple slices are popular due to their ability to retain the natural shape, texture, and recognizable appearance of the fruit, making them more appealing compared to crushed or chunk formats. Consumers increasingly favor fruit products that combine convenience with a fresh-like eating experience. Slices meet this demand through their ready-to-consume nature and ease of serving. Additionally, the segment benefits from the rising demand for portion-controlled fruit products that are easy to store and consume without further preparation.

The chunks segment is expected to be the fastest-growing category in the market, with a projected CAGR of 5.42% through 2031. This growth is attributed to increasing consumer preference for convenient, bite-sized fruit formats that offer versatility, ease of consumption, and a natural eating experience. Pineapple chunks are gaining popularity as they provide a balanced combination of texture, sweetness, and convenience. Their compact and uniform shape enhances ease of handling and portion control, appealing to modern consumers seeking practical and time-saving food options.

Geography Analysis

The Asia-Pacific region accounted for 33.01% of the global canned pineapple market value in 2025, underscoring its position as a major production hub and a rapidly growing consumption market. The region benefits from tropical climatic conditions that facilitate large-scale pineapple cultivation, ensuring a stable supply of raw materials for canning operations. Countries in Asia-Pacific have established advanced pineapple processing and preservation capabilities, enhancing supply chain efficiency and export competitiveness. According to the Food and Agriculture Organization (FAO), the Philippines, one of the largest global producers of pineapples, harvested approximately 2.9 million metric tons in 2024, demonstrating the region's agricultural strength in pineapple production .

The Middle East and Africa region is expected to achieve the highest growth in the global canned pineapple market, with a projected CAGR of 6.98% through 2031. This growth is driven by increasing consumer demand for convenient, long shelf-life food products and rising awareness of fruit-based nutrition and healthy eating habits. Rapid urbanization and changing dietary patterns are fostering greater adoption of packaged fruit products that provide convenience and year-round availability. Additionally, shifting lifestyles and a growing preference for tropical fruit flavors are boosting the consumption of canned pineapple products. Expanding food distribution networks, exposure to international food trends, and rising demand for imported processed fruit products are further accelerating market growth in the region.

North America and Europe together represent the largest combined value pool for branded and premium canned pineapple products. This is supported by strong consumer preference for high-quality, convenient, and sustainably packaged fruit offerings. Consumers in these regions increasingly seek premium canned fruit products that emphasize natural ingredients, clean-label formulations, organic positioning, and superior product quality. The market is further driven by demand for convenient pantry staples that cater to busy lifestyles while offering nutritional value and tropical flavor appeal. Robust retail infrastructure, high penetration of branded packaged foods, and a growing willingness among consumers to pay for premium fruit products continue to support market value growth in both regions.

- Great Giant Pineapple (Sunpride)

- Dole plc

- Del Monte International GmbH

- Thai Pineapple Canning Industry (TPC)

- Tipco Foods PCL

- Princes Group

- Rhodes Food Group

- Goya Foods

- Pineapple India

- Siam Pineapple Ltd.

- Nakorn Food Co., Ltd.

- Siam Agro-Food Industry PCL (SAICO)

- Jutai Foods Group

- Malee Group PCL

- The Kraft Heinz Company

- Hagimex JSC

- Nakorn Food Co., Ltd

- Saico Co., Ltd

- Princes Group

- Siam Pineapple Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for convenient and ready-to-eat fruit products

- 4.2.2 Consumer preference for long shelf-life food products

- 4.2.3 Advancements in canning and food preservation technologies

- 4.2.4 Product innovations such as organic, no-added-sugar, and sustainably packaged

- 4.2.5 Rising consumer inclination toward healthy snacking

- 4.2.6 Increasing demand for year-round availability of tropical fruits

- 4.3 Market Restraints

- 4.3.1 Concerns regarding added sugar and preservatives

- 4.3.2 High competition from frozen, dried, and fresh pineapple alternatives

- 4.3.3 Stringent food safety and labeling regulations

- 4.3.4 Risk of supply chain disruptions affecting sourcing

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Supply-Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Form

- 5.1.1 Slices

- 5.1.2 Chunks

- 5.1.3 Tidbits

- 5.1.4 Crushed

- 5.1.5 Spears and Whole

- 5.2 By Packaging Type

- 5.2.1 Cans

- 5.2.2 Cups and Jars

- 5.2.3 Others

- 5.3 By Distribution Channel

- 5.3.1 Foodservice

- 5.3.2 Retail

- 5.3.2.1 Supermarkets/Hypermarkets

- 5.3.2.2 Convenience/Grocery Stores

- 5.3.2.3 Online Retail Stores

- 5.3.2.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Great Giant Pineapple (Sunpride)

- 6.4.2 Dole plc

- 6.4.3 Del Monte International GmbH

- 6.4.4 Thai Pineapple Canning Industry (TPC)

- 6.4.5 Tipco Foods PCL

- 6.4.6 Princes Group

- 6.4.7 Rhodes Food Group

- 6.4.8 Goya Foods

- 6.4.9 Pineapple India

- 6.4.10 Siam Pineapple Ltd.

- 6.4.11 Nakorn Food Co., Ltd.

- 6.4.12 Siam Agro-Food Industry PCL (SAICO)

- 6.4.13 Jutai Foods Group

- 6.4.14 Malee Group PCL

- 6.4.15 The Kraft Heinz Company

- 6.4.16 Hagimex JSC

- 6.4.17 Nakorn Food Co., Ltd

- 6.4.18 Saico Co., Ltd

- 6.4.19 Princes Group

- 6.4.20 Siam Pineapple Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK