PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063394

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063394

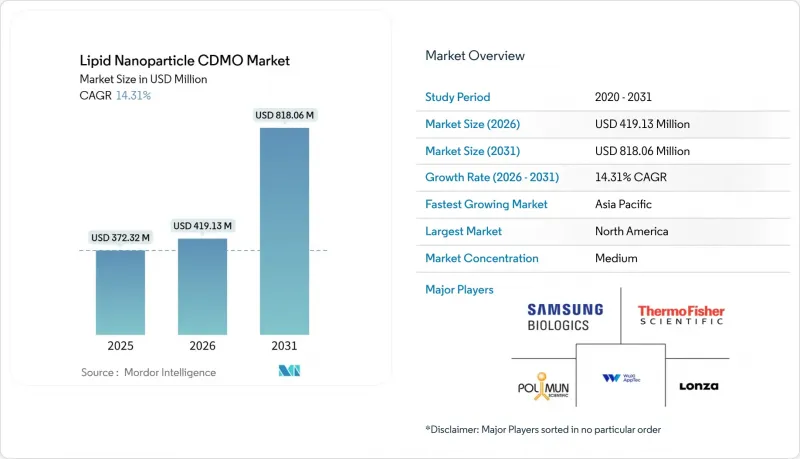

Lipid Nanoparticle CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the lipid nanoparticle cDMO market size was valued at USD 372.32 million in 2025 and is estimated to grow from USD 419.13 million in 2026 to reach USD 818.06 million by 2031, at a CAGR of 14.31% during the forecast period (2026-2031).

This report is Segmented by Service Type (Development & Process Development, LNP Formulation & Encapsulation and More), Application (Infectious Disease Vaccines and More), Scale of Operation(Preclinical, and More), End User (Large Pharma, and More), Technology (Microfluidic Mixing Platforms and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Lipid Nanoparticle CDMO Market Trends and Insights

Pipeline Expansion in mRNA Vaccines and Therapeutics

Dozens of late-stage oncology trials, including Moderna's mRNA-4157 and BioNTech's BNT122, are generating persistent demand for lipid ratio tuning, encapsulation-efficiency optimization, and particle-size control. Personalized vaccine workflows require CDMOs to compress manufacturing cycles from eight weeks to four, reinforcing multi-year service contracts. Rare-disease programs such as mRNA-3927 for propionic acidemia validate the platform's versatility and extend the service horizon beyond seasonal vaccines. Regulatory familiarity with mRNA constructs, supported by FDA analytical guidance issued in 2024, shortens review timelines and emboldens sponsors to advance diversified pipelines . The broadened indication mix lengthens engagement periods and elevates the strategic value of CDMOs with integrated development-to-commercial capabilities.

Outsourcing of Complex LNP Formulation and Fill-Finish

Pharma innovators now view specialist CDMOs as partners for capabilities that are uneconomical to replicate internally. Lonza expanded its Stein and Geleen sites to bundle lipid synthesis through aseptic vial filling under one quality system. Analytical method development alone can exceed USD 10 million in capital outlay per lab, pushing small biotechs now growing at 14.75% CAGR toward external partnerships. Lyophilization expertise further differentiates suppliers, with Precision NanoSystems validating GenVoy-ILM for room-temperature storage in 2025. Continuous processing magnifies this outsourcing imperative because real-time analytics demand cross-functional talent pools that few sponsors maintain in-house.

LNP Intellectual Property Litigation and Licensing Complexity

Arbutus and Genevant sued Moderna across 30 jurisdictions in 2025, creating uncertainty over royalty stacking and freedom-to-operate for licensees. Although the EPO revoked EP 2279254 in 2026, overlapping patents on ionizable lipids still complicate contracting and extend negotiations by up to six months. Smaller sponsors bear higher risk premiums, dampening near-term demand growth within the lipid nanoparticle CDMO market.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed Capacity Investments in Lipids and LNP

- Scalable Microfluidic and Single-Use Platforms

- GMP-Grade Lipid and Component Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Development and Process Development accounted for 35.9% of 2025 revenue and will post the fastest 15.18% CAGR to 2031, underscoring the strategic value of formulation screening and microfluidic parameter tuning. These studies cost USD 2 million to USD 5 million per program and typically precede multi-batch clinical campaigns. cGMP drug-product manufacturing remains the largest absolute pool as approved vaccines and therapeutics command contracts of USD 50 million to USD 200 million, yet its growth rate lags because revenues arrive episodically.

Analytical and quality control services are a rising high-margin niche because regulators expect orthogonal characterization via dynamic light scattering, cryo-EM, and reverse-phase HPLC. Fill-finish and lyophilization capabilities have become premium differentiators after GenVoy-ILM proved room-temperature stability in 2025. Integrated CDMOs that bundle these steps under performance-based contracts are winning share across the lipid nanoparticle CDMO market.

Oncology therapeutics retained a 41.39% revenue share in 2025, reflecting personalized neoantigen vaccines that require bespoke mRNA sequences and rapid turnaround. Each patient-specific batch compresses timelines from eight weeks to four and drives ongoing demand for flexible capacity. Infectious-disease vaccines still anchor government stockpiles but no longer dominate revenues.

Rare, genetic, and metabolic disorders will expand fastest at 14.86% CAGR through 2031, supported by orphan-drug incentives and promising interim data from programs such as mRNA-3927. Other exploratory areas, including cardiometabolic and protein-replacement therapies, remain early-stage yet represent upside for CDMOs that develop tissue-targeted LNP chemistries.

Geography Analysis

North America held 46.75% of 2025 revenue, supported by Thermo Fisher's USD 650 million Greenville expansion and Evonik's BARDA-funded lipid center in Indiana. Dense biotech clusters in Boston and San Francisco sustain early-stage pipeline flow, while regulatory familiarity with mRNA expedites approvals.

Europe accounted for roughly one-quarter of 2025 revenue. Germany's Rhineland corridor links CordenPharma's lipid synthesis, Rentschler's formulation, and Evonik's fill-finish capabilities, offering sponsors EU-GMP compliance without complex cross-border logistics . The United Kingdom's GBP 520 million biomanufacturing fund signals intent to reclaim post-Brexit competitiveness, though divergent regulations add documentation burdens.

Asia-Pacific is projected to grow fastest at 15.48% CAGR through 2031. Samsung Biologics' Songdo facility, Moderna's Melbourne build, and Chinese partnerships between Walvax, CSPC, and WuXi Biologics underscore regional momentum. India's Gennova advanced GEMCOVAC-19 toward approval, showcasing ambitions for indigenous mRNA capacity. WHO's technology-transfer hub extended to 15 countries by 2025, but uneven regulatory capacity limits immediate volume.

- AGC Biologics

- CordenPharma

- Curia

- Eurogentec

- Evonik Health Care

- Fujifilm Toyama Chemical

- Lonza Group

- PCI Pharma Services

- Polymun Scientific

- Porton Advanced

- Recipharm

- Rentschler Biopharma

- Samsung Group

- ST Pharm

- Thermo Fisher Scientific

- TriLink BioTechnologies

- Wacker Biotech

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pipeline Expansion in MRNA Vaccines and Therapeutics

- 4.2.2 Outsourcing of Complex LNP Formulation, Analytics, And Fill-Finish

- 4.2.3 Government-Backed Capacity Investments in Lipids And LNP

- 4.2.4 Scalable Microfluidic and Single-Use LNP Manufacturing Platforms

- 4.2.5 Decentralized/Continuous MRNA-LNP Manufacturing Hubs

- 4.2.6 Lyophilized/Thermostable LNP Formulations Reduce Cold-Chain Burden

- 4.3 Market Restraints

- 4.3.1 LNP IP Litigation and Licensing Complexity

- 4.3.2 GMP-Grade Lipid and Critical Component Supply Constraints

- 4.3.3 Solvent Handling/E&L And Sustainability Constraints In LNP Processes

- 4.3.4 Specialized Talent and Pharma 4.0 Adoption Gaps

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Development & Process Development

- 5.1.2 LNP Formulation & Encapsulation

- 5.1.3 Analytical & Quality Control

- 5.1.4 cGMP Drug Product Manufacturing

- 5.1.5 Fill-Finish & Lyophilization

- 5.2 By Application

- 5.2.1 Infectious Disease Vaccines

- 5.2.2 Oncology Therapeutics

- 5.2.3 Rare/Genetic & Metabolic Disorders

- 5.2.4 Other Therapeutics

- 5.3 By Scale of Operation

- 5.3.1 Preclinical

- 5.3.2 Clinical

- 5.3.3 Commercial

- 5.4 By End User

- 5.4.1 Large Pharma

- 5.4.2 Small/Mid Biotech

- 5.4.3 Government/Academic

- 5.5 By Technology/Process

- 5.5.1 Microfluidic Mixing Platforms

- 5.5.2 Impingement/T-mixing

- 5.5.3 Continuous/Modular LNP Production

- 5.5.4 Alternative Nonviral Nanoparticles

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AGC Biologics

- 6.3.2 CordenPharma

- 6.3.3 Curia

- 6.3.4 Eurogentec

- 6.3.5 Evonik Health Care

- 6.3.6 Fujifilm Toyama Chemical

- 6.3.7 Lonza

- 6.3.8 PCI Pharma Services

- 6.3.9 Polymun Scientific

- 6.3.10 Porton Advanced

- 6.3.11 Recipharm

- 6.3.12 Rentschler Biopharma

- 6.3.13 Samsung Biologics

- 6.3.14 ST Pharm

- 6.3.15 Thermo Fisher Scientific

- 6.3.16 TriLink BioTechnologies

- 6.3.17 Wacker Biotech

- 6.3.18 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment