PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063445

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063445

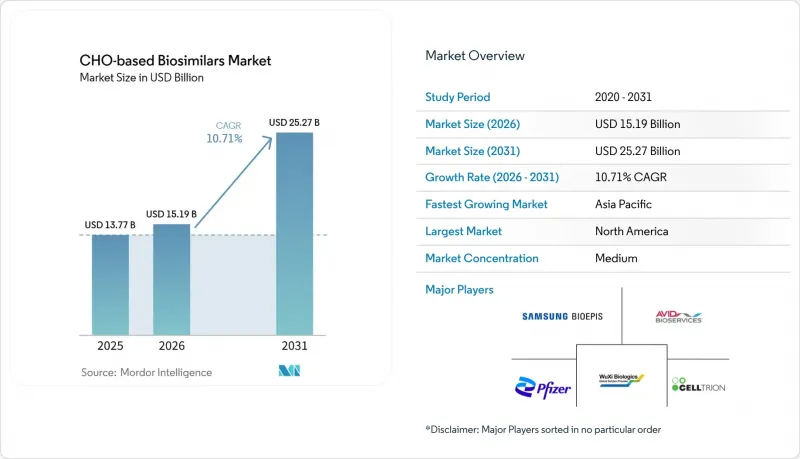

CHO-based Biosimilars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cHO-based biosimilars market size is expected to grow from USD 13.77 billion in 2025 to USD 15.19 billion in 2026 and is forecast to reach USD 25.27 billion by 2031 at 10.71% CAGR over 2026-2031.

This report is Segmented by Products & Services {Products (Monoclonal Antibodies, Fc-Fusion Proteins, Glycoprotein Hormones, C5 Inhibitors, and More), Services & Platform}, Clinical Indication (Oncology, Autoimmune & Inflammatory, Ophthalmology, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global CHO-based Biosimilars Market Trends and Insights

Accelerating Loss of Exclusivity for High-Value Biologics

Blockbusters with annual sales of USD 200 billion to USD 400 billion will lose protection by 2030, with Keytruda, Stelara, and denosumab prominent among them . Many of these molecules carry complex glycosylation patterns that require high-fidelity CHO platforms, which discourage less-capitalized players but reward early movers who can quickly validate comparability. Premium pricing often holds during the first 18 months after launch, but late entrants face steep margin compression. The dynamic is splitting the CHO-based biosimilars market into a tier of scale-driven incumbents and a cluster of niche specialists. As a result, capacity reservation and early regulatory engagement are now more decisive than simply aligning with patent windows. Biosimilar uptake in immunology and insulin classes reached a modest penetration within 5 years of launch, compared with high adoption in oncology and ophthalmology, underscoring the persistence of formulary inertia in outpatient settings. This bifurcation suggests that regulatory interchangeability designations, while symbolically important, matter less than payer willingness to restructure formularies and absorb short-term disruption costs.

FDA / EMA Streamlining of Biosimilar Approval Pathways

By the end of 2025, the FDA had authorized 90 biosimilars across 20 reference molecules, achieving a 70% commercialization rate. Guidance released in September 2025 simplified glycosylation profiling using lectin microarrays, significantly reducing analytical risk . In Europe, the EMA's interchangeability position statement spurred national substitution policies, accelerating adoption in France, Germany, and the Netherlands. Harmonized requirements have shortened clinical development timelines, which benefits resource-rich sponsors that can run concurrent global filings. Smaller firms are increasingly pairing with CDMOs to bridge knowledge gaps and amortize compliance costs across portfolios.

US PBM Rebate/Formulary Dynamics Delay Uptake in Pharmacy-Benefit Classes

Although payer consortia have accelerated adoption in oncology and ophthalmology, immunology, and insulin still see only 25% penetration five years post-launch due to entrenched rebate contracts that blunt net price advantages. Patient assistance programs further insulate originators, limiting near-term upside for CHO-based biosimilars in outpatient settings. Ongoing scrutiny by regulators and employers may pressure PBMs to adjust, but the timeline remains uncertain.

Other drivers and restraints analyzed in the detailed report include:

- Payer Cost-Containment and Tendering Expand Access and Uptake

- EU Scientific Interchangeability and Adoption Mechanisms

- Biosimilar "Void" for Many Upcoming LoEs Due to Technical Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Products contributed 60.35% of 2025 revenue. Monoclonal antibodies alone represented a significant share of global revenue in 2024, while Fc-fusion proteins and glycoprotein hormones trailed by wide margins . Continuous-processing facilities from Celltrion and Samsung Bioepis aim to keep per-gram COGS below USD 80, positioning integrated players to withstand price erosion.

Services and platforms are expected to register a 12.65% CAGR through 2031, as emerging biotechs outsource to CDMOs. WuXi Biologics' UITM platform achieved 18 g/L at 2,000 L GMP scale, illustrating how asset-light pathways help small sponsors sidestep heavy capital outlays. The arrangement also channels incremental volume into Asia-Pacific facilities, reinforcing the region's role as a cost-optimized manufacturing hub in the CHO-based biosimilars market.

Geography Analysis

North America commanded a 42.15% share in 2025, supported by 90 FDA approvals and aggressive payer steering that drove significant Humira biosimilar uptake over 12 months. Growth is expected to plateau in saturated classes, yet upcoming LoEs for Keytruda and other oncology agents will spark new surges.

Europe combines lower absolute revenue with policy leadership; tendering delivered price drops in the United Kingdom, France, and Germany, saving health systems more than EUR 10 billion since 2020. Implementation of automatic substitution varies by country, compelling manufacturers to localize pricing and contracting strategies.

Asia-Pacific is forecast to post a 12.34% CAGR to 2031, underpinned by China's 87 cumulative approvals by year-end 2024 and Japan's premium pricing for first-to-market products. India and South Korea extend regional production advantages, with Samsung Bioepis targeting 571,000 L capacity to anchor global supply. Markets in the Middle East, Africa, and South America remain nascent but show gradual progress through pilot tenders and local regulatory reforms, ultimately broadening the footprint of the CHO-based biosimilars market.

- Abzena

- Aragen life Sciences

- Avid Bioservices

- Celltrion

- CHO Plus

- Enzene Biosciences

- Evotec

- ExcellGene

- Henlius

- Olon France

- Organon

- Patheon Pharma Services

- Peak Proteins

- Pfizer

- Samsung Bioepis

- Thermo Fisher Scientific

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Loss of Exclusivity for High-Value Biologics

- 4.2.2 FDA/EMA Streamlining of Biosimilar Approval Pathways

- 4.2.3 Payer Cost-Containment and Tendering Expand Access and Uptake

- 4.2.4 EU Scientific Interchangeability and National Adoption Mechanisms

- 4.2.5 CHO Process Intensification/Continuous Bioprocessing Drives 40-80% COGS Reductions

- 4.2.6 Precision Glycoengineering/Advanced Analytics Reduce Comparability Risk/Costs

- 4.3 Market Restraints

- 4.3.1 US PBM Rebate/Formulary Dynamics Delay Uptake in Pharmacy-Benefit Classes

- 4.3.2 Biosimilar "Void" For Many Upcoming LoEs

- 4.3.3 Price-Erosion/Tender Concentration Risks Sustainability and Shortages

- 4.3.4 CHO Glycosylation/CQA Control Complexity Raises Development/Manufacturing Risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Products & Services

- 5.1.1 Products

- 5.1.1.1 Monoclonal antibodies (mAbs)

- 5.1.1.2 Fc-fusion proteins

- 5.1.1.3 Glycoprotein hormones (e.g., EPO, FSH)

- 5.1.1.4 C5 inhibitors (eculizumab)

- 5.1.1.5 RANKL inhibitors (denosumab)

- 5.1.1.6 Anti-VEGF fusion proteins (aflibercept)

- 5.1.2 Services & Platform

- 5.1.1 Products

- 5.2 By Clinical Indication

- 5.2.1 Oncology

- 5.2.2 Autoimmune & Inflammatory

- 5.2.3 Ophthalmology (retina)

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abzena

- 6.3.2 Aragen life Sciences

- 6.3.3 Avid Bioservices

- 6.3.4 Celltrion

- 6.3.5 CHO Plus

- 6.3.6 Enzene Biosciences

- 6.3.7 Evotec

- 6.3.8 ExcellGene

- 6.3.9 Henlius

- 6.3.10 Olon France

- 6.3.11 Organon

- 6.3.12 Patheon Pharma Services

- 6.3.13 Peak Proteins

- 6.3.14 Pfizer Inc.

- 6.3.15 Samsung Bioepis

- 6.3.16 Thermo Fisher Scientific

- 6.3.17 Wuxi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment