PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063456

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063456

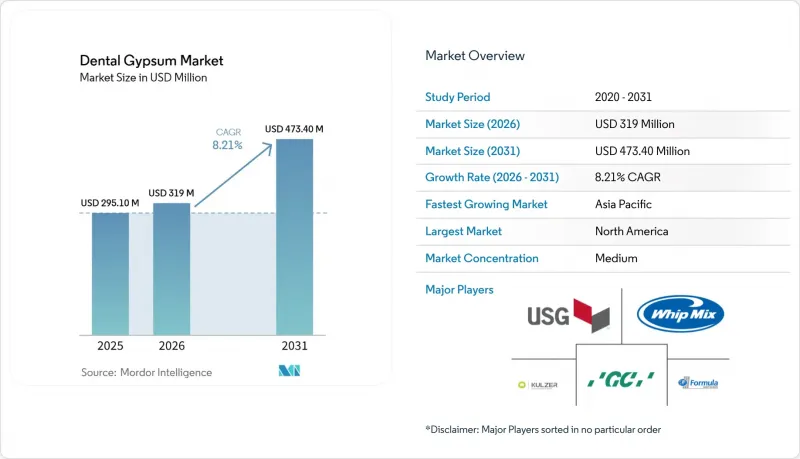

Dental Gypsum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the dental gypsum market size is projected to expand from USD 295.10 million in 2025 and USD 319 million in 2026 to USD 473.40 million by 2031, registering a CAGR of 8.21% between 2026 to 2031.

This report is Segmented by Product Type (Type I, Type II, Type III, and More), Application (Study/Diagnostic Models, Working Casts & Dies, and More), End User (Dental Laboratories, Dental Clinics, Hospitals & Academic/Teaching Institutes), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Dental Gypsum Market Trends and Insights

Rising Prosthodontic Case Volumes

The aging population in North America and Western Europe is driving demand for crowns, bridges, and complete dentures, lifting restorative revenues at a 6.1% trajectory to 2032 . Even as digital dentures trim chairside visits by almost one-third, laboratories still pour Type III bases to stabilize flasks during polymerization and occlusal remounting. Clinical studies confirm that gypsum master casts detect CAD/CAM milling artifacts invisible on-screen, safeguarding marginal integrity. Because a USD 2 gypsum pour averts a USD 3,000 remake, clinicians retain the material in their quality-control protocol. Consequently, prosthodontics is expected to add more than 14 million additional pours annually by 2031, underpinning steady expansion of the dental gypsum market.

Expansion of Dental Laboratories and Outsourcing

ISO-standard tolerance convergence now lets a die poured in Shenzhen seat a crown milled in Chicago with the same 50-micrometer margin fidelity. This regulatory parity catalyzed a shift of over 65% of North American CAD/CAM crown-and-bridge work to APAC super-labs, concentrating procurement and dropping delivered Type III costs below USD 0.50 per cast. Indian dental-tourism clinics, treating half a million foreign patients in 2024, own in-house labs that favor gypsum for treatment planning guides, adding another growth channel. Automated mixing silos and vacuum conditioning cut set-time variation, encouraging high-volume labs to sign multi-year contracts that secure raw gypsum at mine-gate pricing. These dynamics collectively lift long-term demand for the dental gypsum market and heighten supplier competition on service, not chemistry.

Rapid Adoption of Intraoral Scanners Enabling Model-Free or Printed Workflows

Scanner penetration reached 44% of general dentists and 45% of orthodontists by 2024, letting clinicians mill single-unit crowns or order aligners without physical impressions. Powder-free optics cut full-arch capture to 90 seconds, while chairside CAD/CAM systems present same-day placement in a single visit. Each digital case eliminates 200-300 grams of Type III stone, eroding incidental demand. Capital expense still curbs uptake in smaller or rural practices, but in top urban ZIP codes, usage already exceeds 60%, creating a near-term drag on the dental gypsum market.

Other drivers and restraints analyzed in the detailed report include:

- Orthodontic Treatment Growth, Especially in Asia-Pacific

- ISO 6873 Standardization Enabling Cross-Market Adoption

- Shift to 3-D-Printed Models Displacing Poured Stone in Labs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type IV captured an 8.67% CAGR outlook as implant verification and full-arch restorations require compressive strengths past 5,000 psi, sustaining premium pricing within the dental gypsum market size. Type III retained 39.63% dental gypsum market share in 2025 because high-throughput study models still favor its balance of cost and 0.15% expansion consistency. Laboratories producing more than 200 daily casts report that automated vacuum mixers trim porosity, cutting die adjustments by 12% and saving technician hours. Type II remains niche for articulator mounting, while Type I is largely obsolete outside specialized edentulous impressions. Emerging Type V stones, topping 7,000 psi, service zirconia substructures but face limited uptake due to longer set-times that hinder same-day workflows.

ISO 6873 alignment lets suppliers ship identical formulations worldwide, fostering cross-border price convergence and turning logistics efficiency into a core differentiator. Whip Mix's Silky-Rock achieves 0.09% linear expansion and separates in five minutes, an advantage for labs racing against surge volumes of aligner checks. Kulzer's Die-Stone offers pre-weighed satchels that reduce mixing errors to below 1 g, a driver of adoption among small clinics venturing into in-office milling. As competitive intensity rises, vendors bundle automated dispensers and dust-free packaging, cementing long-term penetration of Type IV within the broader dental gypsum market.

Geography Analysis

North America generated 38.13% of the 2025 value, anchored by more than 7,000 certified laboratories and widespread insurance coverage for crowns and implants. OSHA respirable-silica regulation, however, is inflating ventilation and monitoring costs, nudging some independent labs to outsource model production offshore or adopt silica-free formulations. The dental gypsum market size in the region is therefore expanding more slowly than the global average, even though procedural demand remains robust.

Asia-Pacific is forecast for an 8.41% CAGR through 2031, the fastest worldwide. Chinese super-labs process two-thirds of North American CAD/CAM cases, buoyed by ISO-aligned quality assurances that reduce remakes to under 2%. India's inbound dental-tourism clinics poured more than 1.2 million diagnostic casts in 2025 alone, reinforcing material pull. South Korean and Japanese orthodontic hubs maintain gypsum verification even with high scanner adoption, reflecting cultural emphasis on precision. Collectively, these drivers are tilting procurement gravity toward the region, intensifying supplier competition inside the dental gypsum market.

Europe shows stable, aging-driven demand but faces landfill bans on mixed gypsum that escalate disposal fees to USD 150 per ton in Germany and France. Many labs respond by shifting low-risk study models to printed resins, freeing gypsum budgets for high precision Type IV and Type V applications. The Middle East and Africa, while smaller, are opening new teaching hospitals that mandate ISO-certified materials, offering long-tail growth. South America's public oral-health programs and university networks sustain a modest but dependable call for study models, rounding out the global footprint of the dental gypsum market.

- BEGO

- Benco Dental

- Dentona AG

- Ernst Hinrichs Dental GmbH

- ETI Empire Direct

- Garreco LLC

- GC Corporation

- Henry Schein

- Heraeus Kulzer

- Ivoclar

- LASCOD S.p.A.

- Milton Bridge

- Saint-Gobain Formula GmbH

- SHERA Werkstoff-Technologie GmbH

- SILADENT Dr. Bohme & Schops

- USG

- Whip Mix Corporation

- YETI Dentalprodukte

- Yoshino Gypsum

- Zhermack SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prosthodontic Case Volumes

- 4.2.2 Expansion Of Dental Laboratories and Outsourcing

- 4.2.3 Orthodontic Treatment Growth, Especially In APAC

- 4.2.4 ISO 6873 Standardization Supports Quality and Cross-Market Adoption

- 4.2.5 Implant Model and Verification Workflows Still Favor High-Strength Die Stones

- 4.2.6 Cost/Time Advantage Of Gypsum For Select High-Throughput Study Models Vs 3-D Printed

- 4.3 Market Restraints

- 4.3.1 Rapid Adoption of Intraoral Scanners Enabling Model-Free or Printed Workflows

- 4.3.2 Shift To 3D-Printed Models Displacing Poured Stone in Labs

- 4.3.3 OSHA/NIOSH Silica Exposure Compliance Burden in Labs

- 4.3.4 Gypsum Disposal Constraints (H2S Risk) Raising Handling Costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Type I

- 5.1.2 Type II

- 5.1.3 Type III

- 5.1.4 Type IV

- 5.1.5 Type V

- 5.2 By Application

- 5.2.1 Study/diagnostic models

- 5.2.2 Working casts & dies

- 5.2.3 Implant models & verification jigs

- 5.2.4 Orthodontic models

- 5.2.5 Articulator mounting

- 5.2.6 Denture flasking/base pours

- 5.3 By End User

- 5.3.1 Dental Laboratories

- 5.3.2 Dental Clinics

- 5.3.3 Hospitals & Academic/Teaching Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 BEGO

- 6.3.2 Benco Dental

- 6.3.3 Dentona AG

- 6.3.4 Ernst Hinrichs Dental GmbH

- 6.3.5 ETI Empire Direct

- 6.3.6 Garreco LLC

- 6.3.7 GC Corporation

- 6.3.8 Henry Schein

- 6.3.9 Heraeus Kulzer

- 6.3.10 Ivoclar

- 6.3.11 LASCOD S.p.A.

- 6.3.12 Milton Bridge

- 6.3.13 Saint-Gobain Formula GmbH

- 6.3.14 SHERA Werkstoff-Technologie GmbH

- 6.3.15 SILADENT Dr. Bohme & Schops

- 6.3.16 USG

- 6.3.17 Whip Mix Corporation

- 6.3.18 YETI Dentalprodukte

- 6.3.19 Yoshino Gypsum

- 6.3.20 Zhermack SpA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment