PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063461

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063461

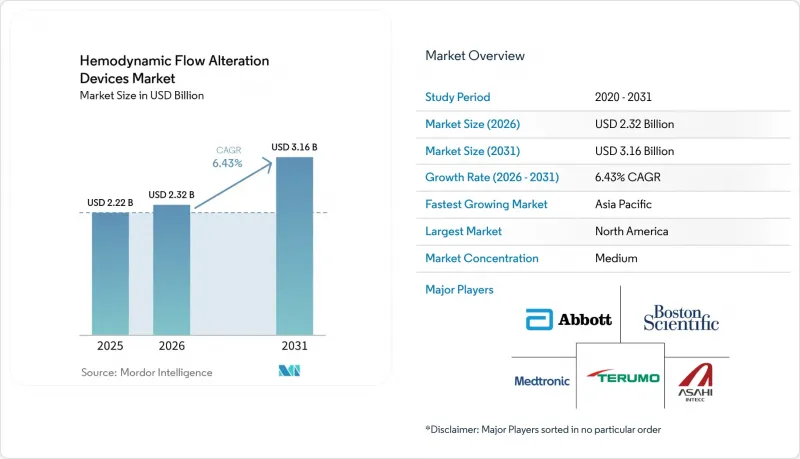

Hemodynamic Flow Alteration Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hemodynamic flow alteration devices market size is expected to increase from USD 2.22 billion in 2025 to USD 2.32 billion in 2026 and reach USD 3.16 billion by 2031, growing at a CAGR of 6.43% over 2026-2031.

This report is Segmented by Device Type (Embolic Protection Devices [Distal Filter, Proximal Occlusion, Others], Chronic Total Occlusion Devices [Guidewires, Others], and Others), Application (Coronary Interventions, Structural Heart, and Others), End User (Hospitals & Clinics, Ascs, and Others), and Geography (North America and More). Market Forecasts are Provided in Terms of Value (USD).

Global Hemodynamic Flow Alteration Devices Market Trends and Insights

Rising Interventional Procedure Volumes in PCI, CAS, and TAVR

Technical success for chronic total occlusion percutaneous coronary intervention in contemporary European expert centers reached 89.1%, with low major adverse cardiac and cerebrovascular event rates, which shows how operator experience and standardized algorithms are improving outcomes in the hemodynamic flow alteration devices market. British Cardiovascular Intervention Society guidance sets minimum procedural volumes per center and per operator to maintain proficiency, aligning training and credentialing with safer and more efficient practice.

Intravascular imaging has been associated with materially lower failure and reintervention compared with angiography alone in CTO cohorts, which is helping to standardize imaging-guided approaches in high-complexity lesions. Carotid artery stenting demand is reinforced by transcarotid artery revascularization utilization in stroke prevention programs, where an FDA-cleared platform is now part of a larger vascular portfolio following a strategic acquisition, which is embedding carotid solutions more deeply in U.S. hospital contracting.

The convergence of growing CTO PCI, carotid interventions, and transcatheter valve procedures is broadening the procedural base that depends on protection and crossing tools across the hemodynamic flow alteration devices market. As high-volume centers disseminate best practices and proctor peers, adoption in mid-volume settings is expected to rise in measured steps, further expanding addressable volumes for suppliers in the hemodynamic flow alteration devices market.

North American Leadership and Expanding Reimbursement Supporting Adoption

Payment levels for endovascular valve replacement with or without major complications established a baseline for hospital reimbursement that private plans often reference, which supports continued program investment in devices and imaging that complement these procedures in the hemodynamic flow alteration devices market. National fee-for-service Medicare spending on ambulatory surgical center services increased with more ASCs operating and more procedures per beneficiary, which underscores a system-level shift to outpatient settings where protection and crossing tools are feasible within facility capabilities. CMS continued to update and clarify hospital outpatient and ASC payment rules and codes, including changes executed through quarterly program transmittals, which influence the timing and economic rationale for migrating eligible cases to outpatient environments. National coding and billing manuals also set expectations for special services and device-related reporting, which helps standardize administrative workflows and can reduce friction in the hemodynamic flow alteration devices market as hospitals and ASCs operationalize new procedure combinations.

Clinical societies and registries provide performance tracking and help define best practices that are adopted across U.S. networks, reinforcing procurement continuity for devices that align with evidence-backed protocols. As coverage criteria and site-of-service rules evolve under Medicare guidance, device makers that design for outpatient efficiency and compatible coding pathways are positioned to gain share in the hemodynamic flow alteration devices market.

Device Costs and Reimbursement Variability Constrain Usage

Intravascular ultrasound use in CTO interventions varied widely across European centers, reflecting national reimbursement heterogeneity and access constraints, and leaving meaningful room for increased adoption even in advanced programs within the hemodynamic flow alteration devices market. Authors of contemporary CTO algorithms have also noted that procedural time, resource intensity, and modest professional payment can discourage routine attempts at more complex lesions in mid-volume centers, which slows diffusion outside of expert hubs. National outpatient and ASC payment rules continue to evolve through CMS program updates and transmittals, which may change site-of-service incentives and affect how providers budget for advanced imaging and crossing tools.

The scale and direction of these payment updates interact with capital budgets, staffing models, and device contracting, creating variation in adoption within and across markets in the hemodynamic flow alteration devices market. Manufacturers adapt through clinical education, value analyses, and portfolio options, but variability in local coverage and purchasing power still slows the pace of standardization. Over time, convergence in policy and continued clinical evidence can narrow these gaps and support steadier adoption.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in CTO Crossing and Re-Entry Systems Raising Success Rates

- Aging Populations and PAD/Diabetes Burden Increasing Occlusion Cases

- Product Safety Notices and Recalls Increase Caution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Embolic Protection Devices accounted for 42.3% of device-type revenue in 2025, with carotid interventions driving steady use of distal filters, and with transcatheter workflows incorporating tailored approaches to debris capture across anatomies in the hemodynamic flow alteration devices market. EPDs accounted for a 42.3% share of the hemodynamic flow alteration devices market size in 2025, and physicians have reassessed routine use in valve procedures after randomized trial data showed no significant reduction in stroke with routine cerebral embolic protection during TAVR, which is encouraging more selective deployment for higher-risk patients.

As a result, suppliers are investing in clearer indication guidance and refined device designs rather than blanket-use positioning in the hemodynamic flow alteration devices market. At the same time, professional society reporting and registry infrastructure maintain attention on stroke endpoints, which anchors physician decision making around evidence and safety. Ongoing procedural growth in carotid and select structural settings sustains a base of EPD usage, while the precision-indication pattern is reshaping purchasing norms within integrated vascular programs across the hemodynamic flow alteration devices market.

Chronic Total Occlusion devices are projected to be the fastest-growing device category at a 7.94% CAGR, supported by imaging-guided strategies that have been linked with lower failure and reintervention compared with angiography alone, which underpins more routine imaging in difficult occlusions. Registry data covering thousands of procedures across expert operators reported high overall technical success near 90% with low event rates, helping codify the role of specialized guidewires, microcatheters, re-entry systems, and plaque-modification options in reproducible workflows in the hemodynamic flow alteration devices industry. Escalation patterns that start with polymer-coated wires and finish with hydrophilic wires were prominent. At the same time, dual-lumen microcatheters enabled parallel-wire techniques and retrograde navigation in selected anatomies, which supports the value of comprehensive crossing portfolios. Guiding catheter extensions also improved support during antegrade dissection and re-entry maneuvers, boosting efficiency in long or calcified segments. Contemporary analyses have described shifts toward intravascular lithotripsy for heavy calcium in some settings, reflecting perceived advantages in safety endpoints, while rotational systems remain staples in specific lesion subsets. Together, these developments signal durable momentum for CTO portfolios within the hemodynamic flow alteration devices market.

Geography Analysis

North America held 42.3% of the hemodynamic flow alteration devices market share in 2025, supported by reimbursement baselines for endovascular valve procedures and coding clarity for cerebral protection that help align hospital financial planning with device adoption. For example, payment values under MS-DRG 266 and 267 created reference points for program budgeting in structural heart care, while add-on coding clarified physician reporting for protection in TAVR when used. Acquisitions that add carotid platforms into major portfolios have widened access to transcarotid solutions and integrated them into hospital contracting structures across stroke-prevention pathways. National guidance on procedural volumes and training continues to support concentration of complex coronary work in higher-volume settings, which sustains imaging and crossing utilization in referral centers. These dynamics underpin steady demand for protection and CTO toolkits across a mature provider base in the hemodynamic flow alteration devices market.

Asia-Pacific is projected to post the fastest regional growth at a 9.57% CAGR through 2031, with China's expanding TAVR programs illustrating a clear learning-curve effect and safety gains as experience increases in the Hemodynamic Flow Alteration Devices market. National registry-level data reported more than twelve thousand TAVR procedures across hundreds of hospitals, with in-hospital mortality falling as centers accumulated cases, and with higher surgical valve volumes associated with lower TAVR mortality. Regional case mix also includes a high burden of metabolic disease, and CTO cohorts in South Asia show concentrated risk profiles with diabetes and hypertension that necessitate revascularization in complex anatomies. Japan's emphasis on intravascular imaging and operator training supports higher imaging adoption during complex PCI than in many European settings, which reinforces procedural quality and device penetration in advanced labs. With tertiary networks scaling capacity and training, adoption of CTO and protection portfolios continues to expand across the hemodynamic flow alteration devices market in Asia-Pacific.

Europe, the Middle East and Africa, and South America show mixed but improving readiness, as leading centers align with volume and training standards and as hospitals weigh expanded outpatient delivery models within local coverage frameworks in the hemodynamic flow alteration devices market. National clinical audits and professional society guidance help unify practice and maintain focus on outcomes, which encourages consistent imaging and crossing protocols in complex coronary cases. Currency volatility and import tariffs in some markets affect pricing and procurement timetables, which adds friction to standardized adoption but does not alter long-run clinical need. Government safety notices and regulatory expectations across the EU and other regions also shape deployment decisions and training priorities around embolization and protection devices. As health systems consolidate experience and clarify local coding, a broader base of providers is positioned to adopt the hemodynamic flow alteration devices market toolkits in a measured and sustainable way.

- Abbott Laboratories

- Asahi Intecc

- Avinger

- Beckton Dickinson

- Boston Scientific

- Contego Medical, Inc.

- Cook Group

- Cordis

- Emblok Embolic Protection System

- Emboline, Inc.

- Filterlex

- InspireMD

- Medtronic

- Merit Medical Systems

- Silk Road Medical

- SoundBite Medical

- Teleflex

- Terumo

- Venus Medtech

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Interventional Procedure Volumes In PCI, CAS, And TAVR

- 4.2.2 North American Leadership And Expanding Reimbursement Supporting Adoption

- 4.2.3 Advancements In CTO Crossing And Re-Entry Systems Raising Success Rates

- 4.2.4 Aging Populations And Pad/Diabetes Burden Increasing Occlusion Cases

- 4.2.5 Shift To Outpatient Cath Labs And Ascs Accelerating Demand For Protection And Crossing Tools

- 4.2.6 Portfolio Bundling And Recent Acquisitions (E.G., TCAR) Speeding Integrated Adoption

- 4.3 Market Restraints

- 4.3.1 Neutral Pimary Endpoint In Protected Tavr Dampens Routine CEP Uptake

- 4.3.2 Device Costs And Reimbursement Variability Constrain Usage

- 4.3.3 Product Safety Notices And Recalls Increase Caution

- 4.3.4 Steep Learning Curve And Longer Procedure Times Limit CTO Device Diffusion Beyond Referral Centers

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Embolic Protection Devices (EPD)

- 5.1.1.1 Distal Filter Systems

- 5.1.1.2 Proximal Occlusion Systems

- 5.1.1.3 Distal Occlusion Systems

- 5.1.1.4 Cerebral EPD for TAVR

- 5.1.2 Chronic Total Occlusion (CTO) Devices

- 5.1.2.1 CTO Guidewires

- 5.1.2.2 Microcatheters

- 5.1.2.3 Crossing Catheters

- 5.1.2.4 Re-entry Systems

- 5.1.2.5 Laser/Atherectomy & Powered Crossing

- 5.1.3 Others (Flow Diverters, Venous Stents)

- 5.1.1 Embolic Protection Devices (EPD)

- 5.2 By Application

- 5.2.1 Coronary Interventions

- 5.2.2 Structural Heart Protection

- 5.2.3 Carotid Artery Stenting

- 5.2.4 Peripheral Arterial Interventions

- 5.2.5 Others (Neurovascular Interventions, Renal & Visceral Artery Interventions, etc.)

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Ambulatory Surgical Centers (ASCs)

- 5.3.3 Outpatient/Independent Cath Labs

- 5.3.4 Specialty Cardiac Centers

- 5.3.5 Others ( Research Institutes & Clinical Trial Centers, Academic Institutes)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 ASAHI INTECC CO., LTD.

- 6.3.3 Avinger

- 6.3.4 BD

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Contego Medical, Inc.

- 6.3.7 Cook

- 6.3.8 Cordis

- 6.3.9 Emblok Embolic Protection System

- 6.3.10 Emboline, Inc.

- 6.3.11 Filterlex

- 6.3.12 InspireMD

- 6.3.13 Medtronic

- 6.3.14 Merit Medical Systems

- 6.3.15 Silk Road Medical

- 6.3.16 SoundBite Medical

- 6.3.17 Teleflex Incorporated

- 6.3.18 Terumo Corporation

- 6.3.19 Venus Medtech (Hangzhou) Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment