PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063465

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063465

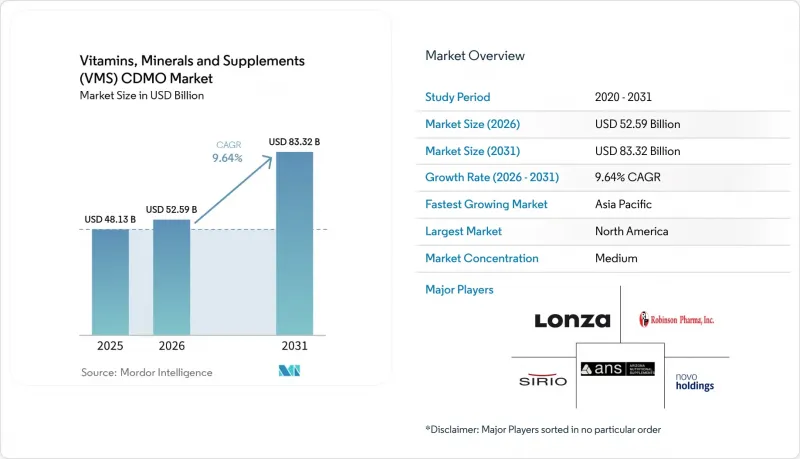

Vitamins, Minerals And Supplements (VMS) CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the vitamins, minerals and supplements cDMO market size was valued at USD 48.13 billion in 2025 and is estimated to grow from USD 52.59 billion in 2026 to reach USD 83.32 billion by 2031, at a CAGR of 9.64% during the forecast period (2026-2031).

This report is Segmented by Dosage Form (Tablets, Capsules, Softgels, and More), Product Type (Dietary Supplements and More), Service Type (Product Development and Formulation, Manufacturing and Packaging, and More), End-User (Pharmaceutical & Biopharma Companies, Nutraceutical Companies, and More), and Geography (North America and More). Market Forecasts are in Value (USD).

Global Vitamins, Minerals And Supplements (VMS) CDMO Market Trends and Insights

Rising Consumer Health Awareness and Preventive Healthcare

Consumers are allocating discretionary income to supplements positioned for immune, cognitive, and metabolic support, decoupling preventive spending from traditional prescription budgets. The CDC recorded that 58.1% of adults in the United States used supplements in 2024, up from 52.3% in 2020. Demand now favors CDMOs that can create condition-specific blends backed by robust analytical data rather than generic multivitamins. In response, leading facilities have installed high-performance liquid chromatography and mass spectrometry labs to validate potency and purity. The Vitamins, Minerals, and Supplements CDMO market benefits when partners also house in-house regulatory teams capable of navigating the FDA structure/function claim guidance. As public sentiment shifts from reactive treatment to proactive supplementation, CDMOs that offer bioavailability optimization secure premium pricing and more extended contracts.

Growing Outsourcing Trend Among Brands

Pharmaceutical and consumer-health companies are liquidating manufacturing assets to focus on brand equity and digital distribution, mirroring trends seen in biologics. Outsourcing lets marketers launch seasonal SKUs without bearing the fixed cost of idle capacity. CDMOs able to run small batches with rapid line changeovers can charge 15-20% price premiums and thus expand margin. However, the same dependence creates allocation risk during production peaks, a factor pushing brands toward long-term supply agreements. The relentless outsourcing wave is one of the strongest structurally positive forces for the Vitamins, Minerals, and Supplements CDMO market.

Volatile Raw-material Prices & Ingredient Shortages

Vitamin and mineral commodity markets experienced severe disruptions in recent years, with DSM-Firmenich flagging shortages of vitamin B12 and vitamin D3 in Q3 and Q4 due to production outages at Chinese fermentation plants and regulatory crackdowns on environmental compliance. CDMOs lack the purchasing power of vertically integrated pharmaceutical companies, forcing them to hold 90-day inventory buffers that tie up working capital and compress margins. Botanical extracts face additional volatility: turmeric prices surged 0.86% in 2024 following monsoon failures in India, and ashwagandha shortages emerged as demand from sports-nutrition brands outstripped cultivation capacity. The issue is compounded by geopolitical risk; the majority of global vitamin C production originates in China, creating a single-source dependency that leaves CDMOs vulnerable to export restrictions or trade tariffs. Brands are responding by demanding dual-sourcing clauses in CDMO contracts, but smaller manufacturers lack the supplier relationships to comply with them.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Gummy, Liquid & Other Experiential Formats

- Aging Population & Chronic-Disease Specific VMS Demand

- High Capex for Multi-format Production Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, tablets accounted for 40.09% of revenue, giving them the largest share of the Vitamins, Minerals, and Supplements CDMO market. Cost efficiency and proven high-speed packaging up to 500 bottles per minute anchor their continued relevance. Yet tablets face perception headwinds among younger users who link pills to illness. Softgels answer that challenge by improving the bioavailability of fat-soluble vitamins and omega-3 oils, and they are projected to register a 12.02% CAGR through 2031, the fastest among forms.

Softgel production involves ISO 7 clean rooms and costly encapsulators, barriers that keep competition low and margins higher. Chewable softgels, which blend oil-based payloads with a gummy-like mouthfeel, are now targeting pediatric omega-3 segments. Acceptance of self-emulsifying systems under FDA GRAS has further widened the application scope. These dynamics collectively underpin the expanding role of softgels within the broader Vitamins, Minerals, and Supplements CDMO market.

Dietary supplements accounted for 39.26% of sales in 2025, underscoring their core role in the Vitamins, Minerals, and Supplements CDMO market. However, sports nutrition is forecast to grow at a 12.89% CAGR, driven by rising interest in protein isolates, collagen peptides, and BCAAs. The category's demographics now range from competitive athletes to seniors combating muscle loss.

Plant-based proteins, such as pea, rice, and hemp, garner share on allergen and sustainability grounds but pose flavor-masking and amino-acid-profile challenges. CDMOs with flavor-engineering capabilities gain an edge. Beauty-from-within offerings that merge hydrolyzed collagen with vitamin C and hyaluronic acid form a premium sub-niche. Functional foods and beverages round out consumer-friendly formats, turning everyday consumption occasions into supplementation points and magnifying demand across the Vitamins, Minerals, and Supplements CDMO market.

Geography Analysis

North America had the most significant regional footprint in 2025, anchored by the United States, where structure/function claims can appear on labels without pre-market approval. Certified facilities enjoy pricing power because retailers increasingly mandate third-party verification. Canada mirrors this dynamic, albeit at a smaller scale, and Mexican maquiladora hubs add flexible capacity for rapid replenishment. Between stringent oversight and mature retail channels, the region supplies a stable cash flow base for the wider Vitamins, Minerals, and Supplements CDMO market.

Asia-Pacific delivers the fastest incremental revenue growth, benefiting from policy incentives such as India's Production Linked Incentive scheme and China's upgraded GB standards. Regional heavyweights, including Sirio Pharma, continue to add vegetarian capsule lines for export customers. Rapid urbanization fuels e-commerce penetration, making standardized supplements more accessible to first-time buyers. The blend of volume growth and rising regulatory expectations positions the area as the chief growth engine for the Vitamins, Minerals, and Supplements CDMO market.

Europe remains fragmented. Germany exemplifies a pharmacy-centric sales model, France leans toward organic plant-based products, and the United Kingdom's post-Brexit divergence adds compliance complexity. Southern nations such as Italy and Spain focus on Mediterranean-aligned nutrients, such as omega-3s and polyphenols. Outside the tri-continental core, Brazil's e-commerce boom and GCC nations' free-zone incentives create smaller but notable pockets of demand, each carving a place in the global Vitamins, Minerals, and Supplements CDMO market landscape.

- Aenova Holding GmbH

- Arizona Nutritional Supplements

- Bactolac Pharmaceutical, Inc.

- Best Formulations Inc.

- Captek Softgel International

- GMP Laboratories of America, Inc.

- Herbalife Intl. of America

- Integrated BioPharma, Inc.

- International Vitamin Corporation (IVC)

- Ion Labs, Inc.

- Lief Labs

- Lonza Group

- Novo Holdings A/S (Catalent Inc.)

- NutraScience Labs

- Robinson Pharma Inc.

- Sirio Pharma Co., Ltd.

- Soft Gel Technologies

- Trividia Manufacturing Solutions Inc.

- Vitaquest International LLC

- Vit-Best Nutrition

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Consumer Health Awareness and Preventive Healthcare

- 4.2.2 Growing Outsourcing Trend Among Brands

- 4.2.3 Rapid adoption of gummy, liquid & other experiential formats

- 4.2.4 Aging Population & Chronic-disease Specific VMS Demand

- 4.2.5 Regulatory Tightening Driving Outsourcing to Certified CDMOs

- 4.2.6 Innovation and Advanced Capabilities

- 4.3 Market Restraints

- 4.3.1 Volatile Raw-material Prices & Ingredient Shortages

- 4.3.2 High Capex for Multi-format Production Lines

- 4.3.3 Heightened Scrutiny of Label Claims & Novel Ingredients

- 4.3.4 Intellectual Property and Confidentiality Concern

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Dosage Form

- 5.1.1 Tablets

- 5.1.2 Capsules

- 5.1.3 Softgels

- 5.1.4 Gummies

- 5.1.5 Powders

- 5.1.6 Liquids & Shots

- 5.1.7 Others

- 5.2 By Product Type

- 5.2.1 Dietary Supplements (Vitamins, Minerals, Herbals)

- 5.2.2 Functional Foods

- 5.2.3 Functional Beverages

- 5.2.4 Sports Nutrition

- 5.2.5 Beauty / Collagen Supplements

- 5.2.6 Others

- 5.3 By Service Type

- 5.3.1 Product Development & Formulation

- 5.3.2 Manufacturing & Packaging

- 5.3.3 Quality Control & Analytical Testing

- 5.3.4 Regulatory & Compliance Services

- 5.3.5 Logistics & Fulfilment

- 5.4 By End-user

- 5.4.1 Pharmaceutical & Biopharma Companies

- 5.4.2 Nutraceutical Companies

- 5.4.3 Consumer Health & Wellness Brands

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aenova Holding GmbH

- 6.3.2 Arizona Nutritional Supplements

- 6.3.3 Bactolac Pharmaceutical, Inc.

- 6.3.4 Best Formulations Inc.

- 6.3.5 Captek Softgel International

- 6.3.6 GMP Laboratories of America, Inc.

- 6.3.7 Herbalife Intl. of America

- 6.3.8 Integrated BioPharma, Inc.

- 6.3.9 International Vitamin Corporation (IVC)

- 6.3.10 Ion Labs, Inc.

- 6.3.11 Lief Labs

- 6.3.12 Lonza Group AG

- 6.3.13 Novo Holdings A/S (Catalent Inc.)

- 6.3.14 NutraScience Labs

- 6.3.15 Robinson Pharma Inc.

- 6.3.16 Sirio Pharma Co., Ltd.

- 6.3.17 Soft Gel Technologies, Inc.

- 6.3.18 Trividia Manufacturing Solutions Inc.

- 6.3.19 Vitaquest International LLC

- 6.3.20 Vit-Best Nutrition

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment