PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063470

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063470

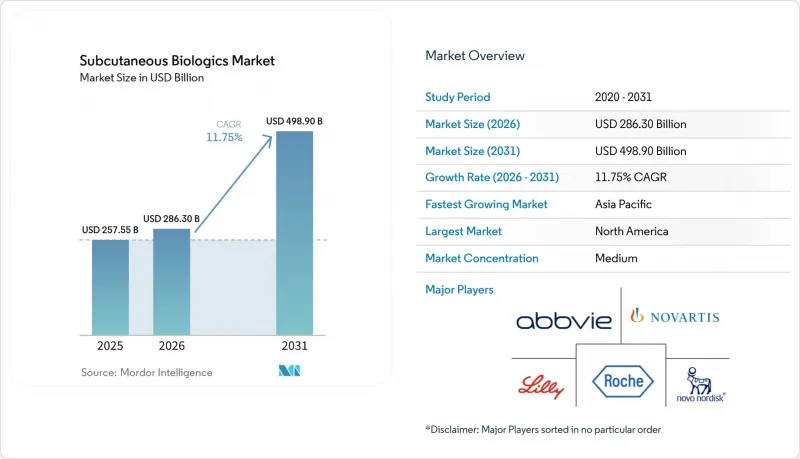

Subcutaneous Biologics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the subcutaneous biologics market size is expected to grow from USD 257.55 billion in 2025 to USD 286.30 billion in 2026 and is forecast to reach USD 498.90 billion by 2031 at 11.75% CAGR over 2026-2031.

This report is Segmented by Molecule Class (mAbs, Peptides/Proteins, Immunoglobulins, Oligonucleotides, Others), Delivery System (Prefilled Syringes, Autoinjectors, Wearables, Vials, Cartridges), Therapy Area (Metabolic, Autoimmune, Oncology, Neurology, Respiratory, Rare Diseases), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are in Value (USD).

Global Subcutaneous Biologics Market Trends and Insights

GLP-1 Expansion in Obesity and T2D Accelerates SC Biologics Demand

Dual and triple agonists are achieving weight-loss results previously reserved for bariatric surgery, which is shifting payer calculus toward earlier pharmacologic intervention. Novo Nordisk's amycretin delivered 22% mean weight reduction at 36 weeks, outpacing semaglutide and moving into Phase III in 2026 . Generic liraglutide introductions in late 2024 and mid-2025 lowered entry prices and opened cost-sensitive markets. Canadian semaglutide generics expected in early 2026 will further broaden access through provincial formularies. Pipeline combinations such as CagriSema are designed to fine-tune satiety and glycemic control, sustaining demand for high-concentration pens. Even with an oral semaglutide filing under FDA review, adherence data suggest high-dose obesity regimens will continue to favor injection. Collectively, these dynamics elevate pen and autoinjector volumes, reinforcing the growth trajectory of the subcutaneous biologics market.

Shift to At-Home Self-Administration Reduces Site-of-Care Costs

Patient-reported outcomes from the IMscin002 study showed that 70.7% preferred subcutaneous delivery because it liberates time and eliminates cannulation discomfort . The FDA's December 2024 approval of subcutaneous nivolumab cut chair time from 60 minutes to 5 minutes, while mosunetuzumab's December 2025 nod compressed delivery of a bispecific antibody to 1 minute. Regional U.S. payers responded in 2025 by paying 90-95% of the IV rate when patients inject at home. European oncology units cite similar efficiencies, pushing hospitals to redeploy infusion nurses to more complex procedures. As convenience and cost incentives align, the subcutaneous biologics market gains volume across oncology, immunology, and metabolic lines.

Supply Constraints for GLP-1s and Injection Components

Although Wegovy and Mounjaro shortages were resolved by February 2025, downstream constraints in glass barrels, plungers, and wearable electronics linger. Stevanato pledged EUR 400 million to raise syringe output significantly by 2027, and Gerresheimer added 200 million units of annual capacity in Serbia. West Pharmaceutical invested USD 150 million in high-speed autoinjector lines in Ireland and the United States. Nonetheless, lead times for custom wearable injectors hover at 18-24 months, slowing launches of next-generation formulations. These bottlenecks temporarily limit how fast the subcutaneous biologics market can scale, despite underlying demand.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Approvals of SC Versions of Prior IV Biologics

- Biosimilar Entry Drives Volume Expansion in Self-Injected Immunology

- Payer Controls and Price Pressure on Specialty Drugs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oligonucleotides siRNA and antisense constructs form the fastest-growing slice of the subcutaneous biologics market, advancing at a 13.45% CAGR to 2031 as refined lipid-nanoparticle carriers, and GalNAc conjugates improve tissue penetration and temper injection-site reactions. Peptides and proteins still controlled 54.01% of 2025 revenue, helped by Novo Nordisk's amycretin, which delivered 22% mean weight loss at 36 weeks, and by generic liraglutide launches that widened access across Medicaid and provincial formularies.

Monoclonal antibodies remain the second-largest class as subcutaneous checkpoint inhibitors-nivolumab SC (FDA, December 2024) and pembrolizumab SC (EMA, November 2025)-shrink administration windows to 1-5 minutes, freeing infusion capacity. Immunoglobulin replacement therapies are unlocking new volume as 20-mL wearable pumps condense the four- to six-site regimens common in primary immunodeficiency management.

Geography Analysis

Asia-Pacific posts a 13.14% CAGR outlook, driven by China's 2024-2025 subcutaneous biosimilar wave, Japan's broadened GLP-1 reimbursement, and South Korea's export-oriented biosimilar giants. India's fill-finish expansion and Australia's PBS coverage gains further widen regional access, though affordability gaps persist outside urban centers.

North America still accounted for 51.09% of the subcutaneous biologics market share in 2025 as IRA price negotiations paradoxically fueled biosimilar volume growth and as payers reimbursed at-home injections at near-IV parity. Europe ranks second; EMA's sub-one-minute pembrolizumab approval and hospital capacity constraints speed adoption, while Southern European tenders push biosimilar penetration in immunology lines by 2025. GCC investment and Latin American public-health initiatives support nascent uptake elsewhere, though macro volatility moderates growth in Argentina and parts of Sub-Saharan Africa.

- Abbvie

- Amgen

- AstraZeneca

- Biocon Biologics

- Celltrion Holdings Co., Ltd.

- CSL Behring GmbH

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Grifols

- Johnson & Johnson

- Merck

- Novartis

- Regeneron Pharmaceuticals

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GLP-1 Expansion in Obesity and T2D Accelerates SC Biologics Demand

- 4.2.2 Shift To At-Home Self-Administration Reduces Site-Of-Care Costs

- 4.2.3 Rapid Approvals of SC Versions of Prior IV Biologics (Oncology/Immunology)

- 4.2.4 Biosimilar Entry Drives Volume Expansion in Self-Injected Immunology

- 4.2.5 High-Volume/Viscous SC Delivery Via Wearables Unlocks Larger Doses

- 4.2.6 Connected Autoinjectors Improve Adherence and Persistence

- 4.3 Market Restraints

- 4.3.1 Supply Constraints For GLP-1s And Injection Components

- 4.3.2 Payer Controls and Price Pressure on Specialty Drugs

- 4.3.3 Tissue Tolerability Limits for High-Volume/Viscosity SC Injections

- 4.3.4 Sustainability Pressure on Single-Use Injectors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Molecule Class

- 5.1.1 Monoclonal antibodies (mAbs)

- 5.1.2 Peptides/proteins (incl. GLP-1s, insulin analogs)

- 5.1.3 Immunoglobulins (SCIG)

- 5.1.4 Cytokines/interferons

- 5.1.5 Oligonucleotides (siRNA/ASO)

- 5.1.6 Enzymes/hormones and others specified

- 5.2 By Delivery System

- 5.2.1 Prefilled syringes

- 5.2.2 Autoinjector pens

- 5.2.3 On-body/wearable injectors

- 5.2.4 Vial-and-syringe

- 5.2.5 Prefilled cartridges for pens

- 5.3 By Therapy Area

- 5.3.1 Metabolics

- 5.3.2 Autoimmune & inflammatory

- 5.3.3 Oncology & hematology

- 5.3.4 Neurology

- 5.3.5 Respiratory & allergy

- 5.3.6 Rare diseases & immunodeficiencies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of MEA

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc

- 6.3.2 Amgen, Inc

- 6.3.3 AstraZeneca Plc

- 6.3.4 Biocon Biologics

- 6.3.5 Celltrion Holdings Co., Ltd.

- 6.3.6 CSL Behring GmbH

- 6.3.7 Eli Lilly & Company

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 GlaxoSmithKline

- 6.3.10 Grifols, S.A.

- 6.3.11 Johnson & Johnson

- 6.3.12 Merck & Co., Inc

- 6.3.13 Novartis AG

- 6.3.14 Regeneron Pharmaceuticals

- 6.3.15 Sanofi

- 6.3.16 Takeda Pharmaceutical Company Limited

- 6.3.17 Teva Pharmaceutical Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment