PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063502

Lactate Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

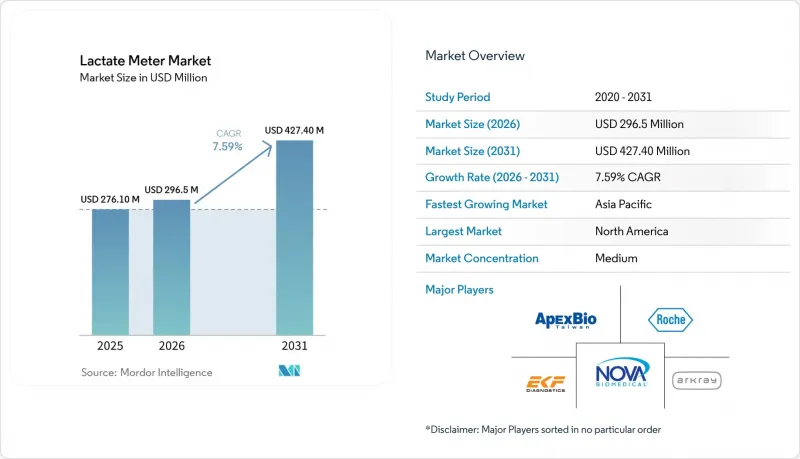

According to Mordor Intelligence, the lactate meter market size is projected to be USD 276.10 million in 2025, USD 296.5 million in 2026, and reach USD 427.40 million by 2031, growing at a CAGR of 7.59% from 2026 to 2031.

This report is Segmented by Product Type (Handheld Meters, and Benchtop/Tabletop Analyzers), by Power Source (Battery-Operated, Chargeable/Rechargeable), by Technology (Electrochemical Sensors, Optical Sensors, and More), by Application (Medical Intervention, and More), by End-User (Hospitals & Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Lactate Meter Market Trends and Insights

Rapid Shift Toward Handheld and Connected POC Devices

Emergency departments have standardized handheld meters to compress lactate turnaround time from 30-45 minutes to under 2 minutes, supporting the Surviving Sepsis Campaign hour-1 bundle. Direct integration with electronic medical records eliminates transcription errors and automates lactate-clearance trending. Battery-operated designs dominate because they bypass shared charging logistics that complicate shift handover. The FDA's CLIA-waiver pathway accelerates market entry by limiting performance criteria to a coefficient of variation below 10%. Cloud connectivity remains polarizing as hospitals weigh cybersecurity exposure against predictive-maintenance benefits, yet vendors continue to embed Bluetooth modules to future-proof devices. The shift has raised consumable demand because each handheld strip is single-use, linking hardware adoption directly to recurring revenue.

Growing Adoption by Elite & Amateur Sports Programs

Lactate-threshold testing migrated from Olympic training centers to NCAA programs and amateur cycling clubs when meter pricing fell below USD 300 and strip costs dropped under USD 2. Elite soccer academies in Spain and Germany now conduct weekly tests to individualize interval workloads, noting that fixed heart-rate zones misclassify 30% of athletes due to genetic variability. Wearable sweat-lactate pilots run in South Korea and the European Union, reflecting athlete demand for non-invasive options. Sports institutes increasingly favor multi-parameter platforms that also capture glucose and hemoglobin to consolidate diagnostics budgets. Because no ISO standard governs sports lactate devices, vendors bypass lengthy clinical-validation studies, accelerating time-to-market but raising performance variability.

High Per-Test Consumable Cost in Low-Resource Settings

Strip prices between USD 2 and USD 8 exceed daily health-spending limits in 47 low-income countries, forcing clinicians to ration tests. Multi-analyte devices aim to amortize costs but raise capital requirements. Paper-based prototypes promise sub-USD 1 pricing yet lack WHO prequalification, and distributor mark-ups in East Africa push retail prices even higher. Rationing undermines early sepsis detection, limiting the lactate meter market in public-sector facilities.

Other drivers and restraints analyzed in the detailed report include:

- ICU Protocols Mandating Lactate Tracking for Sepsis Bundles

- Reimbursement Expansion for Emergency Lactate Testing (US & EU)

- Regulatory Uncertainty Over Non-Invasive Measurement Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Handheld devices secured 63.50% of the lactate meter market share in 2025 and will climb at a 7.80% CAGR through 2031, bolstered by emergency workflows favoring sub-2-minute turnaround times. Benchtop analyzers serve central laboratories that process up to 500 daily samples and integrate with LIS under HL7 messaging. Despite higher throughput and optical detection that mitigates enzyme drift, their capital cost and 18-month service contracts deter small hospitals. Handheld units prevail in sports monitoring and veterinary practice because coaches and vets conduct field-side testing without power outlets. Benchtop analyzers remain indispensable in pharmaceutical QC labs, validating micro-fluidic chips against reference assays. Regulatory advantages amplify the handheld edge; CLIA-waived status exempts operators from proficiency testing if meters stay below 10% coefficient of variation.

Battery-operated meters controlled 78.60% of 2025 revenue and will grow at 8.00% CAGR as EDs and rural clinics value disposable alkaline cells that eliminate recharging infrastructure. Rechargeable platforms appeal to European sports institutes seeking sustainability alignment with the EU Green Deal. Lithium-ion units support 300-500 cycles but cost USD 100-150 more than battery models, extending payback periods. Infection-control protocols in U.S. hospitals discourage shared chargers, reinforcing disposable preference. Asia-Pacific field clinics adopt solar-assisted chargers, yet battery sales continue to outpace rechargeable shipments. Component shortages in lithium supply chains could erode rechargeables' cost advantage, further cementing battery dominance in the lactate meter market.

Geography Analysis

Asia-Pacific's 8.03% forecast CAGR signals a structural pivot in the lactate meter market as public-health programs extend POC diagnostics beyond tertiary hospitals into county-level facilities. China alone intends to outfit more than 3,000 county hospitals with handheld meters by 2030 under Healthy China 2030, a policy that embeds lactate testing into early sepsis recognition for rural populations. India's Ayushman Bharat transformation funds 150,000 health-and-wellness centers, each budgeted for essential diagnostics including lactate strips creating volume orders that improve price elasticity. South Korea and Japan accelerate wearable sensor trials facilitated by robust telecom infrastructure, positioning the region for rapid non-invasive adoption once regulatory clarity emerges.

North America retains technology leadership due to entrenched 510(k) clearances, established reimbursement, and hospital EMR integration. United States. emergency medical services equip ambulances with handheld meters, adding pre-hospital demand that Europe is only beginning to replicate. Canadian provinces subsidize POC lactate in remote Indigenous communities, widening rural access. Mexico's private-hospital groups import battery-operated meters from U.S. vendors, but public-sector uptake remains limited by strip costs.

Europe's mature reimbursement anchors steady replacement cycles rather than explosive growth. Germany's DRG incentives reward hospitals that shorten ICU stays via rapid lactate-clearance tracking, boosting POC throughput. France and Spain focus on connected-device cybersecurity compliance under GDPR, delaying cloud launches but encouraging local data-residency solutions. The United Kingdom leverages NHS England's sepsis pathway to justify trust-level procurement of handheld meters, although budget constraints enforce competitive tendering that squeezes strip pricing.

- Roche

- EKF Diagnostics Holdings PLC

- Nova Biomedical

- Arkray

- Sensa Core Medical Instrumentation Pvt. Ltd.

- ApexBio

- BST Bio Sensor Technology

- TaiDoc Technology

- Analox Instruments Ltd

- Xylem Inc.

- PKvitality

- TECOM Analytical Systems

- VivaChek Biotech

- Woodley Equipment Company

- Jorgensen Laboratories

- Abbott Laboratories

- Danaher

- Yellow Springs Instrument (YSI)

- Cosmed

- Bionime

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Shift Toward Handheld and Connected POC Devices

- 4.2.2 Growing Adoption by Elite & Amateur Sports Programs

- 4.2.3 ICU Protocols Mandating Lactate Tracking for Sepsis Bundles

- 4.2.4 Reimbursement Expansion for Emergency Lactate Testing (US & EU)

- 4.2.5 Wearable Sweat-Lactate Sensors Entering Pilot Deployments

- 4.2.6 Pharma R&D Using Micro-Fluidic Lactate Chips for Cell-Culture

- 4.3 Market Restraints

- 4.3.1 High Per-Test Consumable Cost in Low-Resource Settings

- 4.3.2 Regulatory Uncertainty Over Non-Invasive Measurement Accuracy

- 4.3.3 Data-Privacy Hurdles for Cloud-Connected Meters In EU

- 4.3.4 Supply-Chain Exposure to Specialty Enzymes & Membranes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Handheld Meters

- 5.1.2 Benchtop/Tabletop Analyzers

- 5.2 By Power Source

- 5.2.1 Battery-operated

- 5.2.2 Chargeable/Rechargeable

- 5.3 By Technology

- 5.3.1 Electrochemical Sensors

- 5.3.2 Optical Sensors

- 5.3.3 Biosensors

- 5.3.4 Other Technology

- 5.4 By Application

- 5.4.1 Medical Intervention

- 5.4.2 Sports Performance Monitoring

- 5.4.3 Veterinary

- 5.4.4 Other Applications

- 5.5 By End-user

- 5.5.1 Hospitals & Clinics

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Sports Institutes & Teams

- 5.5.4 Other End-User

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 F. Hoffmann-La Roche AG

- 6.3.2 EKF Diagnostics Holdings PLC

- 6.3.3 Nova Biomedical

- 6.3.4 Arkray, Inc.

- 6.3.5 Sensa Core Medical Instrumentation Pvt. Ltd.

- 6.3.6 ApexBio

- 6.3.7 BST Bio Sensor Technology

- 6.3.8 TaiDoc Technology Corporation

- 6.3.9 Analox Instruments Ltd

- 6.3.10 Xylem Inc.

- 6.3.11 PKvitality

- 6.3.12 TECOM Analytical Systems

- 6.3.13 VivaChek Biotech

- 6.3.14 Woodley Equipment Company

- 6.3.15 Jorgensen Laboratories

- 6.3.16 Abbott Laboratories

- 6.3.17 Danaher Corporation

- 6.3.18 Yellow Springs Instrument (YSI)

- 6.3.19 COSMED srl

- 6.3.20 Bionime Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment