PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063514

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063514

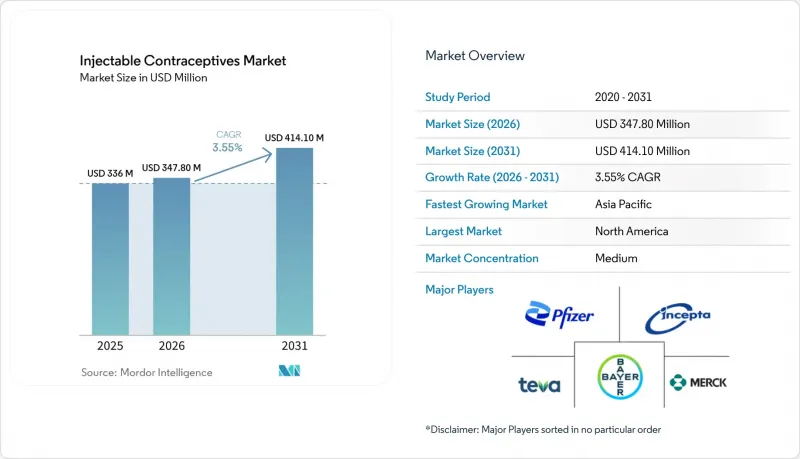

Injectable Contraceptives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the injectable contraceptives market size is projected to expand from USD 336 million in 2025 and USD 347.80 million in 2026 to USD 414.10 million by 2031, registering a CAGR of 3.55% between 2026 to 2031.

This report is Segmented by Hormonal Composition (Combined Formulation, and Progestin-Only), Dosage Schedule (Monthly, 3-Month, 6-Month Long-Acting), Distribution Channel (Hospital & Specialty-Clinic Pharmacies, Retail Pharmacies & Drug Stores and More), End User (Women 15-24, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Injectable Contraceptives Market Trends and Insights

Rising Unmet Need for Long-Acting Reversible Contraception in LMICs

Low- and middle-income countries account for the majority of the 218 million women with unmet contraceptive need, yet depot injectables make up only a modest portion of the method mix in these markets, leaving a sizable demand gap that procurement agencies are beginning to close through larger framework agreements. PATH documented 1.7 million self-injection visits across 14 countries between 2020 and 2024, achieving 65-72% continuation at 12 months, well above the 55-60% typical for clinic-administered injections. Eliminating long travel and wait times helps women avoid losing up to two days of agricultural wages per visit, reinforcing the economic case for self-injection programs . Supply disruptions in Nigeria illustrated how stock-outs quickly translate to discontinuation and unintended pregnancies, adding urgency to diversifying suppliers. Manufacturers holding WHO prequalification are best placed to scale because 70% of LMIC volumes flow through UN channels rather than commercial trade.

Favorable Government Family-Planning Initiatives & Donor Funding

Family-planning budgets in 69 FP2030 focus countries climbed 57% between 2019 and 2024, underpinning procurement stability even as U.S. bilateral funding fell 41% in early 2025. Domestic allocations rose significantly in the Democratic Republic of Congo, Zambia, and Zimbabwe during 2025, signaling a pivot toward self-reliance that reduces donor exposure. UNFPA's 2026-2030 plan dedicates 35% of its commodity basket to injectables and implants versus 28% previously, directing incremental spend toward depot formulations. Countries with stronger fiscal capacity, such as India and South Africa, maintain notable annual volume growth, whereas donor-heavy markets like Niger remain flat until alternate funding emerges. Suppliers diversified across public and private channels stand to capture outsized gains as funding sources rebalance.

Side-Effect Profile Driving Discontinuation Rates

Up to 70% of depot users experience irregular bleeding, and the FDA has required a bone-density warning since 2004, creating a perception hurdle among adolescents who are otherwise ideal candidates. A 2024 French review linked long-term use to meningioma, prompting new contraindications and sparking social-media amplification that drives a 35-40% first-year drop-out. Although bone density rebounds within three years of stopping, the black-box labeling remains a deterrent. Manufacturers are testing dual-mechanism agents designed to reduce bleeding, but no option will reach the market before 2028, keeping the restraint in place in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Higher Adherence & Cost-Effectiveness Versus Daily Oral Pills

- Sub-Cutaneous Products Enabling Task-Shifting to Community Health Workers

- Competition from Implants & Intra-Uterine Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Progestin-only injectables are expanding their lead over combined estrogen-progestin alternatives, building on the 69.32% share they commanded in 2025. Their appeal comes from breastfeeding compatibility, broad use across age groups, and the absence of estrogen-linked risks that limit combined products to roughly one-third of women of reproductive age. The 2025 update to WHO's Medical Eligibility Criteria classified progestin-only methods as Category 1 for lactating women and for users with cardiovascular risk, while combined injectables received Category 3-4 ratings for women older than 35 who smoke, those with hypertension, or anyone with a history of venous thromboembolism. This guidance now channels about the majority of new adopters toward depot medroxyprogesterone acetate and similar formulations, especially in low- and middle-income countries where cardiovascular screening is scarce.

Combined formulations hold the remaining share and cater mainly to younger, non-smoking women who value predictable bleeding over the amenorrhea that affects more than half of progestin-only users within a year. Their growth outlook is constrained by rising obesity and population aging, factors that prompt groups such as the American College of Obstetricians and Gynecologists to steer women with a body-mass index above 35 kg/m2 away from estrogen-containing methods because of clotting risk.

Three-month depots held 49.54% share in 2025 thanks to the legacy of DMPA, yet payer push-back over visit costs fuels interest in extended intervals that halve clinic traffic. A single family-planning encounter costs public systems USD 15-25, so six-month injectables cut annual service expenditure by roughly 20-25%, appealing especially to under-funded programs.

The six-month pipeline is forecast to grow at 5.54% CAGR, contingent on timely Phase III success and WHO prequalification by 2028. Monthly injectables, once favored for mimicking natural cycles, are receding at -1 to -1.5% CAGR because self-administered three-month depots already deliver similar bleeding patterns without clinic visits. The injectable contraceptives market size could shift toward a barbell distribution, with self-injected quarterly doses on one end and six-month provider-administered shots on the other, squeezing mid-frequency formats. Pricing strategies will matter: if manufacturers peg six-month wholesale prices at less than double three-month vials, payers may transition rapidly to longer intervals for cost savings. Regulators have already updated labeling guidance to accommodate extended intervals, clearing a path for commercialization once efficacy thresholds are met.

Geography Analysis

North America generated 42.43% of global value in 2025, buoyed by reimbursement and high per-capita spending, but growth is expected to soften as market saturation meets competition from five-year implants. Social-media safety debates further temper new-user acquisition even as telemedicine channels expand prescription volume. The injectable contraceptives market size in the region may plateau if switching outpaces new initiations, despite rising self-administration adoption.

Asia-Pacific is forecast to lead growth at 5.76% CAGR on the back of policy reforms that authorize auxiliary nurse midwives to give depots, effectively trebling provider density in rural India and Indonesia. Population momentum and urban income gains also lift private-sector uptake, while donor programs focus on hard-to-reach provinces across the Philippines and Vietnam. By 2031, the region could close half the dollar-value gap with North America, reflecting both volume and mix shifts in the injectable contraceptives market.

Europe captures a significant share but trends sideways because of low fertility rates and high contraceptive prevalence that offer limited headroom for expansion. The Middle East and Africa hold a notable share yet promise a high CAGR, provided donor-funded procurement remains intact. South America, at modest share, is projected to advance as regulatory barriers to telemedicine ease and community health worker programs proliferate, particularly in Brazil and Uruguay.

- Abbvie

- Bayer

- Cipla

- Dongkook Pharmaceutical Co., Ltd.

- Eve Pharmaceuticals

- Famy Care Ltd.

- Gedeon Richter Plc

- HLL Lifecare

- Incepta Pharmaceuticals Ltd.

- Johnson & Johnson

- Lupin

- Merck

- Organon

- Pfizer

- Sandoz Group

- Serum Institute of India Pvt Ltd.

- Shanghai HPGC Huayao Pharma Co.

- Teva Pharmaceutical Industries

- TherapeuticsMD

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Unmet Need for Long-Acting Reversible Contraception in LMICs

- 4.2.2 Favorable Government Family-Planning Initiatives & Donor Funding

- 4.2.3 Higher Adherence & Cost-Effectiveness Versus Daily Oral Pills

- 4.2.4 Sub-Cutaneous Products Enabling Task-Shifting to Community Health Workers

- 4.2.5 Pipeline Of Heat-Stable Depot Injectables for Ambient Distribution

- 4.2.6 Telemedicine-Driven Prescription Fulfillment for Self-Injection

- 4.3 Market Restraints

- 4.3.1 Side-Effect Profile Driving Discontinuation Rates

- 4.3.2 Competition From Implants & Intra-Uterine Devices

- 4.3.3 API Shortages Disrupting Medroxyprogesterone Supply Chain

- 4.3.4 Social-Media Misinformation on Hormonal Safety

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Hormonal Composition

- 5.1.1 Combined Formulation

- 5.1.2 Progestin-Only

- 5.2 By Dosage Schedule

- 5.2.1 Monthly Injectable

- 5.2.2 3-Month Injectable

- 5.2.3 6-Month Long-Acting Injectable

- 5.3 By Distribution Channel

- 5.3.1 Hospital & Specialty-Clinic Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Platforms

- 5.3.4 NGO & Public-Health Facilities

- 5.4 By End User

- 5.4.1 Women 15-24 Years

- 5.4.2 Women 25-34 Years

- 5.4.3 Women 35-44 Years

- 5.4.4 Women 45+ Years

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Bayer AG

- 6.3.3 Cipla Limited

- 6.3.4 Dongkook Pharmaceutical Co., Ltd.

- 6.3.5 Eve Pharmaceuticals

- 6.3.6 Famy Care Ltd.

- 6.3.7 Gedeon Richter Plc

- 6.3.8 HLL Lifecare Limited

- 6.3.9 Incepta Pharmaceuticals Ltd.

- 6.3.10 Johnson & Johnson

- 6.3.11 Lupin Pharmaceuticals Inc.

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Organon & Co.

- 6.3.14 Pfizer Inc.

- 6.3.15 Sandoz International GmbH

- 6.3.16 Serum Institute of India Pvt Ltd.

- 6.3.17 Shanghai HPGC Huayao Pharma Co.

- 6.3.18 Teva Pharmaceutical Industries Ltd.

- 6.3.19 TherapeuticsMD Inc.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment