PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063531

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063531

Reproductive Toxicity Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

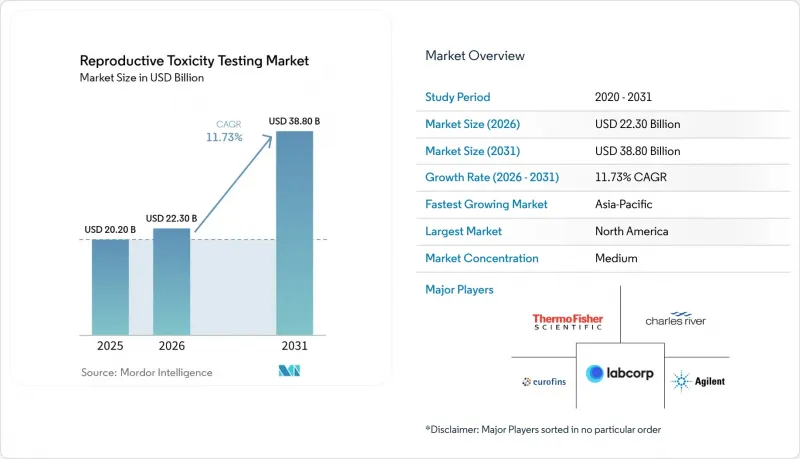

According to Mordor Intelligence, the reproductive toxicity testing market size is projected to be USD 20.20 billion in 2025, USD 22.30 billion in 2026, and reach USD 38.80 billion by 2031, growing at a CAGR of 11.73% from 2026 to 2031.

This report is Segmented by Product (Consumables, Assays, Equipment, and Instruments), Testing Type (In Vivo, in Vitro, in Silico & Computational), Technology (Cell Culture, High-Throughput, Toxicogenomics), End-User (Pharmaceuticals & Biopharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Reproductive Toxicity Testing Market Trends and Insights

Regulatory Bodies Align with ICH S5(R3) & OECD TG Expansions

ICH S5(R3) enables sponsors to customize study designs according to drug class and indication, minimizing redundant animal testing while maintaining human safety margins. OECD's Test Guideline 443 (EOGRTS) has replaced the two-generation model, reducing animal use by approximately 40% and incorporating optional cohorts for developmental neuro- and immunotoxicity assessments. A 2023 review identified under-dosing issues in 20% of EOGRTS submissions, sparking renewed discussions on dose selection among industry stakeholders and regulators. In 2025, the United Kingdom expanded OECD TG 408 to include thyroid and lipid markers, aligning routine 90-day studies more closely with endocrine disruptor screening.

Growing Biopharma Pipelines Fueling Demand for DART Packages

In 2024, the U.S. FDA approved 55 new molecular entities, primarily targeting oncology, rare diseases, and metabolic conditions, all requiring customized DART packages. GLP-1 receptor agonists, initially developed for diabetes, are now being explored for cardiovascular and renal protection, increasing the number of candidates undergoing preclinical reproductive evaluations. The rise in biosimilar submissions has necessitated the demonstration of equivalence on reproductive endpoints, adding to the workload for EOGRTS and embryo-fetal development (EFD) studies. The BIOSECURE Act, enacted in December 2025, restricted federal contracts with companies associated with specific Chinese biotechnology vendors, causing relocation delays of 12 to 18 months for smaller sponsors and increasing the demand for compliant CRO services in India and Eastern Europe.

Limited Regulatory Validation of Complex Organ-On-Chip Systems

Organ-on-chip platforms showcase capabilities such as placental transfer, follicle maturation, and spermatogenesis within controlled microfluidic environments. However, regulatory agencies have not yet issued formal qualification opinions for these systems. IAMPS is addressing reproducibility challenges through inter-laboratory ring trials and the development of reference-compound libraries. Nonetheless, inconsistencies in cell sourcing, extracellular matrices, and flow parameters continue to impede consensus adoption across the industry.

Other drivers and restraints analyzed in the detailed report include:

- Global Push for 3Rs/Animal-Testing Bans Boosting NAM Adoption

- Expansion of CRO Capacity in APAC & Eastern Europe

- High Cost & Long Timelines of OECD TG 443/EOGRTS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, consumables dominated the reproductive toxicity testing market, capturing 57.80% of global revenues. Every in vitro run drives consistent demand for proprietary reagents, stem-cell lines, and assay kits, ensuring reliable cash flows for suppliers. Highlighting the industry's shift towards standardized platforms, Charles River's ReproTracker kit facilitates swift developmental-toxicity screenings in human stem cells. Additionally, with China's endocrine-endpoint rules set to take effect in February 2026, there's a surge in demand for reagents, particularly thyroid-hormone assays and anogenital-distance measurement kits.

In 2025, while in vivo studies held a 53.80% share of the reproductive toxicity testing market, in vitro methods are rapidly gaining ground. Regulators now endorse validated stem-cell and organoid assays, allowing early hazard identification in development programs. This acceptance diminishes the necessity for comprehensive EOGRTS packages, especially for lower-risk chemicals. Techniques like high-content imaging and multiplexed biomarker readouts in 384-well formats enable sponsors to evaluate hundreds of candidates in the time it traditionally took for one in vivo cohort.

While studies on embryo-fetal and pre-/postnatal development remain essential where required, sponsors are increasingly prioritizing candidate evaluations using computational toxicology and NAM screens. This strategic approach not only aligns with the 3Rs objectives but also minimizes late-stage attrition, promoting a balanced split in the reproductive toxicity testing market between animal and non-animal methods.

Geography Analysis

North America remains the largest hub for CRO infrastructure and regulatory expertise. The United States hosts key players such as Charles River, Labcorp, and Inotiv, along with several mid-tier providers, all reporting high utilization rates for DART suites. While sponsors explore cost-saving opportunities abroad, consistent NIH funding and updated FDA guidance continue to drive domestic demand. The United States maintains its leadership in methodological innovation through the rapid adoption of NAMs and early integration of AI-driven study designs.

Europe follows closely but faces challenges due to regulatory complexities. ECHA's stringent requirements for EOGRTS dossiers on industrial chemicals conflict with bans on cosmetics testing, requiring sponsors to navigate waivers on a case-by-case basis. The United Kingdom's post-Brexit "Replacing Animals in Science" roadmap signals a gradual shift toward NAMs, while Germany and France focus on harmonizing best practices for dose selection. Research clusters in Basel, Cambridge, and the Scandinavian corridor provide a steady flow of contracts for regional CROs.

Asia-Pacific is the fastest-growing region. China's alignment with OECD protocols and India's expanding GLP ecosystem attract global pharmaceutical and agrochemical companies. Local governments offer tax incentives for laboratory construction, and academic institutions channel graduates into toxicology careers, partially addressing the shortage of pathologists. Investments in high-throughput automation and data science teams position regional CROs to capture a larger share of the global reproductive toxicity testing market over the next five years.

- Agilent Technologies

- BioIVT

- BioReliance Corp. (Merck KGaA)

- Catalent

- Charles River

- Cyprotex Ltd. (Evotec AG)

- Danaher Corp. (Beckman Coulter Life Sciences)

- Eurofins

- Gentronix Ltd.

- ICON

- Inotiv Inc.

- InSphero

- Intertek Group

- Laboratory Corp. of America Holdings (Labcorp)

- Mimetas BV

- SGS

- Thermo Fisher Scientific

- WuXi AppTec Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Alignment with ICH S5(R3) & OECD TG Expansions

- 4.2.2 Rising Biopharma Pipelines Demanding DART Packages

- 4.2.3 Global 3Rs/Animal-Testing Bans Accelerating NAM Uptake

- 4.2.4 CRO Capacity Expansion in APAC & Eastern Europe

- 4.2.5 AI-Driven Virtual-Cell Models Lowering Screening Costs

- 4.2.6 Growing Use of Human Biomonitoring to Trigger Testing

- 4.3 Market Restraints

- 4.3.1 Limited Regulatory Validation of Complex Organ-On-Chip Systems

- 4.3.2 High Cost & Long Timelines of OECD TG 443/EOGRTS

- 4.3.3 Shortage Of Trained DART Pathologists Globally

- 4.3.4 Data-Ownership Hurdles for Federated Learning Platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Consumables

- 5.1.2 Assays

- 5.1.3 Equipment and Instruments

- 5.2 By Testing Type

- 5.2.1 In Vivo Reproductive Toxicity Testing

- 5.2.1.1 Fertility & Early Embryonic Development (FEED)

- 5.2.1.2 Embryo-Fetal Development (EFD)

- 5.2.1.3 Pre- & Postnatal Development (PPND)

- 5.2.1.4 Extended One-Generation Study (EOGRTS)

- 5.2.1.5 Specialized In Vivo Endocrine Assays

- 5.2.2 In Vitro Reproductive Toxicity Testing

- 5.2.2.1 Cell-based Assays

- 5.2.2.2 Embryonic Stem-Cell Test (EST)

- 5.2.2.3 Rodent Whole-Embryo Culture (WEC)

- 5.2.2.4 3D Organoids & Microphysiological Systems

- 5.2.2.5 High-Throughput Screening Panels

- 5.2.3 In Silico & Computational Testing

- 5.2.3.1 QSAR Models

- 5.2.3.2 AI-Driven Virtual-Cell Models

- 5.2.3.3 PBPK Modelling

- 5.2.1 In Vivo Reproductive Toxicity Testing

- 5.3 By Technology

- 5.3.1 Cell culture technology

- 5.3.2 High-throughput technology

- 5.3.3 Toxicogenomics

- 5.4 By End-User

- 5.4.1 Pharmaceuticals & Biopharmaceuticals

- 5.4.2 Medical Devices & Combination Products

- 5.4.3 Chemicals & Agrochemicals

- 5.4.4 Cosmetics & Personal Care

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 BioIVT LLC

- 6.3.3 BioReliance Corp. (Merck KGaA)

- 6.3.4 Catalent Inc.

- 6.3.5 Charles River Laboratories International Inc.

- 6.3.6 Cyprotex Ltd. (Evotec AG)

- 6.3.7 Danaher Corp. (Beckman Coulter Life Sciences)

- 6.3.8 Eurofins Scientific SE

- 6.3.9 Gentronix Ltd.

- 6.3.10 ICON plc

- 6.3.11 Inotiv Inc.

- 6.3.12 InSphero AG

- 6.3.13 Intertek Group plc

- 6.3.14 Laboratory Corp. of America Holdings (Labcorp)

- 6.3.15 Mimetas BV

- 6.3.16 SGS SA

- 6.3.17 Thermo Fisher Scientific Inc.

- 6.3.18 WuXi AppTec Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment