PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063540

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063540

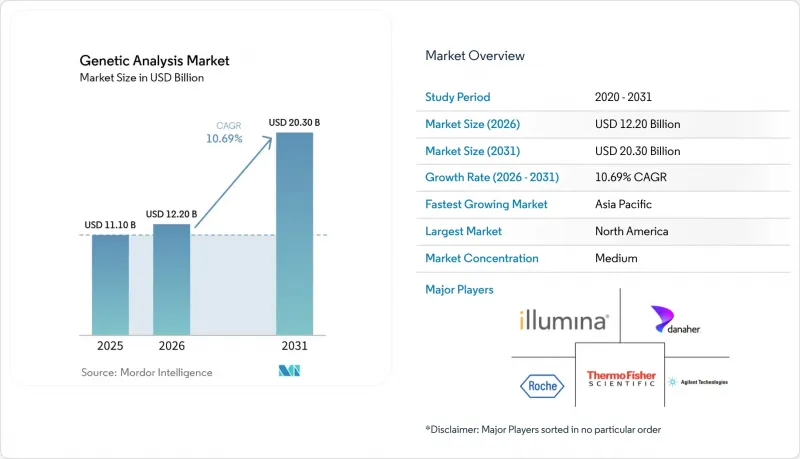

Genetic Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the genetic analysis market size is expected to increase from USD 11.10 billion in 2025 to USD 12.20 billion in 2026 and reach USD 20.30 billion by 2031, growing at a CAGR of 10.69% over 2026-2031.

This report is Segmented by Product & Service (Instruments & Systems, Consumables & Reagents, and More), Technology (PCR/QPCR, NGS Short-Read, Long-Read Sequencing, and More), Application (Clinical Diagnostics, Pharmacogenomics, and More), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, APAC, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Genetic Analysis Market Trends and Insights

Declining Sequencing Costs Compress Cost-per-Genome

Whole-genome sequencing prices have dropped 96% since 2013, reaching USD 200-600 per sample in 2025, and Pacific Biosciences' planned SPRQ-Nx platform aims to push costs below USD 300 in late 2026. As large newborn and adult studies in the United Kingdom, India, and China ramp up, vendors are pivoting from a hardware-sale mindset to recurring-reagent and software subscriptions, evidenced by Pacific Biosciences reporting 55% consumables growth in Q4 2025. Emerging-market projects such as GenomeIndia illustrate that lower per-genome costs open doors for population diversity studies. The result is a deeper installed base and recurring revenue streams that stabilize the genetic analysis market.

Expanding Clinical Reimbursement and CDx Approvals

CMS set a USD 2,989.55 payment for Illumina's TruSight Oncology Comprehensive, effective January 2026, while Medicare also covered NeoGenomics' 500-gene liquid biopsy in March 2026. Private insurers such as UnitedHealthcare updated policies accordingly, catalyzing laboratory investment in higher-throughput sequencers. FDA approvals for Guardant 360 CDx and other large panels are teaching payers that broader tests reduce costly repeat biopsies. The trend escalates volumes flowing through the genetic analysis market and underpins demand for automated workflow solutions.

Data Privacy and Cross-Border Transfer Constraints

The European Health Data Space, operational through 2027, forces vendors to host data on EU-resident clouds and meet strict consent requirements, inflating compliance costs and favoring capital-rich players. Smaller labs may consolidate or exit, tempering pace but not direction of growth for the genetic analysis market.

Other drivers and restraints analyzed in the detailed report include:

- National Genomics Programs Integrating WGS into Care

- AI-Enabled Variant Interpretation Accelerates Insights

- High Capital Investment Requirements for Laboratory Infrastructure and Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recurring reagent kits generated 58.9% of 2025 revenue, anchoring the genetic analysis market size at the laboratory bench. Instrument upgrades to long-read and spatial platforms support a 12.4% CAGR, and bundled software subscriptions are lifting average account value. Integrated ecosystems that lock in reagents, software, and service underpin vendor pricing power.

Instruments & systems are entering a replacement phase as labs shift to higher throughput and multiomics workflows. Revenue clustering around consumables allows vendors to weather capital-spending cycles, keeping the genetic analysis market on a steady growth track.

Short-read NGS held 32.2% of the genetic analysis market share in 2025, but long-read sequencing is forecast to be the fastest segment with 14.0% CAGR through 2031. Clinical need for phasing and structural-variant clarity is bringing Pacific Biosciences and Oxford Nanopore into oncology and rare-disease labs. Meanwhile, digital PCR is expanding in gene-therapy QC. The technology mix is fragmenting, requiring informatics layers that can harmonize heterogeneous data streams and broaden the genetic analysis market footprint.

Geography Analysis

North America captured 43.29% of the genetic analysis market share in 2025. High reimbursement levels, dense hospital and laboratory networks, and early use of comprehensive genomic profiling sustain regional demand. The Centers for Medicare & Medicaid Services set a USD 2,989.55 payment for Illumina's TruSight Oncology Comprehensive test effective January 2026, accelerating the adoption of broad multi-gene panels in oncology practices. Roche's USD 50 billion commitment to new U.S. manufacturing and AI-driven R&D facilities through 2030 underscores confidence in the market's long-term trajectory. While North America will remain the largest revenue contributor through 2031, growth is expected to moderate as oncology and rare-disease testing nears saturation, shifting vendor emphasis toward pharmacogenomics, prenatal screening, and population-health applications.

Asia-Pacific is projected to log the fastest 12.97% CAGR between 2026 and 2031, fueled by large-scale public genomics programs. China's National GeneBank now houses data from more than 10 million genomes, supporting both research and clinical sequencing. India's GenomeIndia initiative has completed 10,000 genomes and plans to broaden coverage of South Asian ancestry groups that are under-represented in global databases.

Europe benefits from coordinated country programs and the European Health Data Space, which standardizes cross-border genomic data sharing across member states. The NHS Genomic Medicine Service delivered more than 810,000 tests in 2024, while Genomics England is sequencing 100,000 newborns and 150,000 adults, weaving whole-genome testing into routine care. Beyond these regions, Gulf states, South Africa, and Brazil are scaling genomics centers, though reimbursement gaps in parts of Latin America and Eastern Europe still limit near-term uptake.

- 10x Genomics

- Agilent Technologies

- Azenta

- BGI / MGI Tech

- Bio-Rad Laboratories

- Danaher

- Eurofins

- Roche

- Guardant Health

- Helix

- Illumina

- LabCorp

- Myriad Genetics

- Natera

- New England Biolabs (NEB)

- Novogene

- Oxford Nanopore Technologies

- Pacific Biosciences

- QIAGEN

- Quest Diagnostics

- Revvity

- Takara Bio

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining Sequencing Costs Compress Cost-Per-Genome

- 4.2.2 Expanding Clinical Reimbursement and CDX Approvals

- 4.2.3 National Genomics Programs Integrating WGS Into Care

- 4.2.4 EU New Genomic Techniques Enabling Agri-Genomics

- 4.2.5 AI-Enabled Variant Interpretation Accelerates Insights

- 4.2.6 Rising Liquid Biopsy Adoption for MRD And Early Detection

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-Border Transfer Constraints (GDPR Etc.)

- 4.3.2 China HGR Rules Constrain Cross-Border Genomics

- 4.3.3 Reimbursement Variability for Comprehensive CGP/WGS

- 4.3.4 Data Localization and Sovereign Cloud Requirements

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Instruments & Systems

- 5.1.2 Consumables & Reagents

- 5.1.3 Software & Bioinformatics Services

- 5.2 By Technology

- 5.2.1 PCR/qPCR

- 5.2.2 Next-Generation Sequencing (short-read)

- 5.2.3 Long-read Sequencing (SMRT, Nanopore)

- 5.2.4 Sanger Sequencing

- 5.2.5 Microarrays

- 5.2.6 Cytogenetics (Karyotyping, FISH)

- 5.2.7 Genotyping & Gene Expression (non-NGS)

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.2 Pharmacogenomics

- 5.3.3 Agriculture & Animal Genomics

- 5.3.4 Forensics & Human Identification

- 5.3.5 Consumer/Ancestry & Wellness

- 5.3.6 Research Applications (functional, transcriptomics, single-cell)

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic & Reference Laboratories

- 5.4.3 Academic & Research Institutes

- 5.4.4 Pharmaceutical & Biotechnology Companies

- 5.4.5 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 10x Genomics

- 6.3.2 Agilent Technologies

- 6.3.3 Azenta Life Sciences

- 6.3.4 BGI / MGI Tech

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Danaher Corporation

- 6.3.7 Eurofins Scientific

- 6.3.8 F. Hoffmann-La Roche

- 6.3.9 Guardant Health

- 6.3.10 Helix

- 6.3.11 Illumina

- 6.3.12 Labcorp

- 6.3.13 Myriad Genetics

- 6.3.14 Natera

- 6.3.15 New England Biolabs (NEB)

- 6.3.16 Novogene

- 6.3.17 Oxford Nanopore Technologies

- 6.3.18 Pacific Biosciences

- 6.3.19 QIAGEN

- 6.3.20 Quest Diagnostics

- 6.3.21 Revvity

- 6.3.22 Takara Bio

- 6.3.23 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment