PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063561

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063561

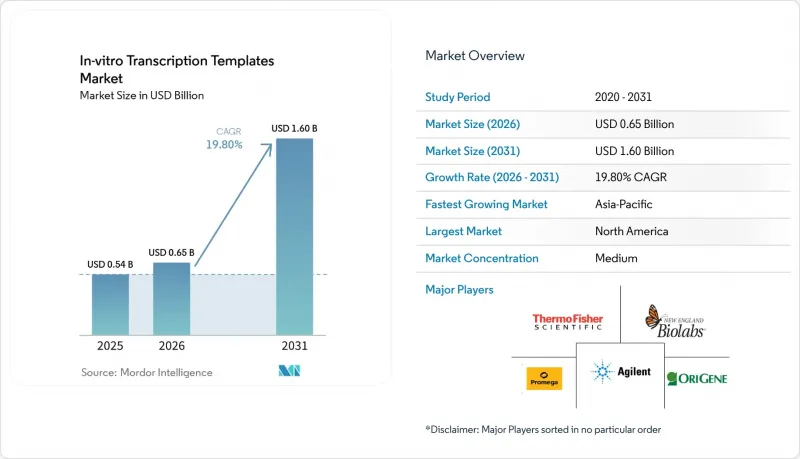

In-vitro Transcription Templates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the in-vitro transcription templates market size is expected to grow from USD 0.54 billion in 2025 to USD 0.65 billion in 2026 and is forecast to reach USD 1.60 billion by 2031 at 19.80% CAGR over 2026-2031.

This report is Segmented by Template Type (Linearised Plasmid DNA, Synthetic Gene Fragments, PCR Amplicons, Oligonucleotides, Others), Application (mRNA Therapeutics & Vaccines, and More), End User (Biopharma, Cros & CMOs, Academic Institutes, Clinical Labs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global In-vitro Transcription Templates Market Trends and Insights

mRNA Vaccine Manufacturing Expands Rapidly

As pandemic-era demand stabilizes, the In-vitro Transcription Templates market continues to grow, driven by seasonal influenza initiatives and oncology pipelines. In 2024, Moderna expanded its Norwood, Massachusetts, facility by 200,000 square feet to enhance its multi-product mRNA production capacity. In June 2024, the FDA introduced a new benchmark requiring sponsors to maintain residual host-cell DNA levels below 10 ng per dose. Template suppliers are adopting next-generation sequencing for lot release, which, while increasing per-unit costs, improves downstream transcription yields by up to 25%. In 2025, efforts to accelerate synthetic DNA template development for rapid-response vaccine platforms further reinforced the demand for high-purity templates.

CRISPR Guide-RNA Synthesis Services See Rising Adoption

As clinical programs transition from ex vivo edits to in vivo delivery, the demand for guide-RNA volumes per patient is increasing, along with higher standards for template quality. By 2025, significant production of cGMP guide-RNA batches supported multiple investigational new-drug applications. Advanced cloud design engines now integrate off-target prediction with IVT template optimization, identifying secondary structures in the T7 promoter that can reduce transcription efficiency by 40%. While the FDA modernized its gene-therapy framework in 2024, the European Medicines Agency has yet to align its purity specifications fully, requiring global sponsors to comply with dual regulatory standards.

Batch-to-Batch Variability in T7 Polymerase Yields

Wild-type T7 polymerase lots experience activity variations of 20% to 40%, resulting in the generation of double-stranded RNA contaminants that reduce translation efficiency. A 2024 study demonstrated that a G47A+884G mutant enzyme decreased dsRNA formation by 85%. However, scaling up production remains a challenge, as fermentation titers are 30% lower compared to the wild type. To mitigate the risk of low-activity lots, sponsors often procure excess enzyme, increasing the cost of goods by 10% to 15%. Additionally, implementing real-time activity assays extends delivery timelines by 2 to 3 weeks, exposing the In-vitro Transcription Templates market to potential scheduling delays.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Investments for Cell & Gene Therapy CDMOs

- Synthetic Biology Foundries Revolutionize IVT Workflows

- Limited Availability of GMP-Compliant Nucleotide Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, linearised plasmid DNA templates accounted for 47.8% of the In-vitro Transcription Templates market, reflecting their longstanding regulatory acceptance and compatibility with established mRNA workflows. However, the market for synthetic gene fragments is projected to grow significantly, with a strong 20.45% CAGR. A notable development in 2025 was the commercialization of ENFINIA IVT-Ready DNA, which offers delivery in under seven days, significantly faster than the traditional 4-6 week plasmid cloning timeline. Sequence-verified fragments streamline processes by bypassing fermentation, eliminating endotoxin remediation, and reducing the risk of host-cell DNA contamination.

Geography Analysis

In 2025, North America held a 39.61% market share, supported by FDA guidance that sets global purity standards and the strong presence of established industry players. However, the Asia-Pacific region is expected to grow significantly, with a projected 21.34% CAGR in the In-vitro Transcription Templates market through 2031. Major investments in the region include a large-scale biocampus featuring advanced cell-gene therapy and mRNA suites. Plans to automate a significant portion of global capacity by 2026 further enhance the region's competitive edge. In Europe, growth is moderated by hazardous-waste fees under regulatory directives, prompting the adoption of closed-loop bioreactors despite their high costs.

Emerging regions remain below a 10% market share. India is advancing in the value chain with the announcement of a significant biologics CDMO facility in 2026, signaling its ambition to compete in this space. Dual-sourcing strategies are becoming increasingly common as companies balance regulatory certainty in North America and Europe with cost efficiencies in the Asia-Pacific region.

- Agilent Technologies

- Aldevron LLC (Danaher)

- Bioneer

- Bio-Rad Laboratories

- Bio-Synthesis

- Cytiva

- Eurofins

- GeneDesign Inc.

- Genscript

- Integrated DNA Technologies (IDT)

- Jena Bioscience

- Lucigen Corporation (LGC Biosearch)

- Maravai LifeSciences (TriLink BioTechnologies)

- Merck KGaA (MilliporeSigma)

- New England Biolabs

- OriGene Technologies

- Promega

- QIAGEN

- Roche

- Synbio Technologies

- Takara Bio

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Scale-Up of Mrna Vaccine Manufacturing

- 4.2.2 Growing Adoption of CRISPR Guide-RNA Synthesis Services

- 4.2.3 Rising Investments in Cell & Gene Therapy Cdmos

- 4.2.4 Advent of Synthetic Biology Foundries Standardising IVT Workflows

- 4.2.5 Biopharma Demand for GMP-Grade Linearised Plasmid Templates

- 4.2.6 Cloud-Based Automation of Template Design & Error-Checking

- 4.3 Market Restraints

- 4.3.1 Batch-To-Batch Variability in T7 Polymerase Yields

- 4.3.2 Limited Availability Of GMP-Compliant Nucleotide Raw Materials

- 4.3.3 IP Cross-Licensing Disputes on Promoter Sequences

- 4.3.4 Environmental Regulations on Plasmid-Prep Waste Streams

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Template Type

- 5.1.1 Linearised Plasmid DNA Templates

- 5.1.2 Synthetic Gene Fragments

- 5.1.3 PCR Amplicon Templates

- 5.1.4 Oligonucleotide Templates

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 mRNA Therapeutics & Vaccines

- 5.2.2 Cell & Gene Therapy (CRISPR gRNA, siRNA)

- 5.2.3 Diagnostic Probes

- 5.2.4 RNA Structural Studies

- 5.2.5 Synthetic Biology & Protein Engineering

- 5.3 By End User

- 5.3.1 Biopharmaceutical & Biotechnology Companies

- 5.3.2 Contract Research & Manufacturing Organisations (CROs & CMOs)

- 5.3.3 Academic & Research Institutes

- 5.3.4 Clinical & Diagnostic Laboratories

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies Inc.

- 6.3.2 Aldevron LLC (Danaher)

- 6.3.3 Bioneer Corporation

- 6.3.4 Bio-Rad Laboratories Inc.

- 6.3.5 Bio-Synthesis Inc.

- 6.3.6 Cytiva (Danaher)

- 6.3.7 Eurofins Genomics

- 6.3.8 GeneDesign Inc.

- 6.3.9 GenScript Biotech Corporation

- 6.3.10 Integrated DNA Technologies (IDT)

- 6.3.11 Jena Bioscience GmbH

- 6.3.12 Lucigen Corporation (LGC Biosearch)

- 6.3.13 Maravai LifeSciences (TriLink BioTechnologies)

- 6.3.14 Merck KGaA (MilliporeSigma)

- 6.3.15 New England Biolabs Inc.

- 6.3.16 OriGene Technologies

- 6.3.17 Promega Corporation

- 6.3.18 QIAGEN N.V.

- 6.3.19 F. Hoffmann-La Roche Ltd

- 6.3.20 Synbio Technologies

- 6.3.21 Takara Bio Inc.

- 6.3.22 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment