PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063565

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063565

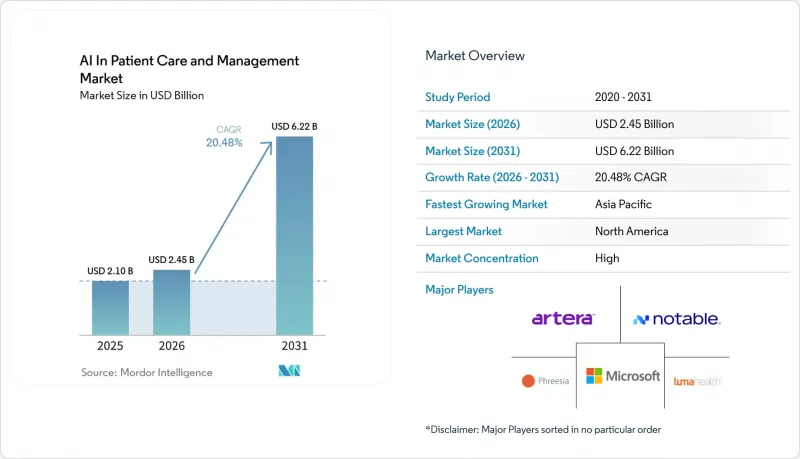

AI In Patient Care And Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aI in Patient Care and Management market size is expected to grow from USD 2.10 billion in 2025 to USD 2.45 billion in 2026 and is forecast to reach USD 6.22 billion by 2031 at 20.48% CAGR over 2026-2031.

This report is Segmented by Offering (Software, Services), Deployment Mode (Cloud, On-Premise, Hybrid), Technology (Natural Language Processing (NLP), and Others), Application (Enhanced Communication and Omnichannel Messaging, and Others), End User (Healthcare Providers, and Others), and Geography (North America, Europe, Asia-Pacific, and Others). Forecasts Provided in Value (USD).

Global AI In Patient Care And Management Market Trends and Insights

CMS Interoperability and Prior Authorization APIs Accelerate Digital Patient Access and Status Automation

The CMS Interoperability and Prior Authorization Final Rule requires impacted payers to stand up FHIR-based Patient Access, Provider Access, Payer-to-Payer, and Prior Authorization APIs, with operational provisions live on January 1, 2026 and full API compliance by January 1, 2027. The rule introduces firm turnaround times for prior authorization, including a seven-day standard decision window and reporting obligations that increase transparency and accountability. These provisions transform prior authorization from a manual and opaque process into a dataset that AI agents can query, pre-populate, and monitor, which reduces back-and-forth communications and shrinks call volumes. Patient-facing assistants gain new value when prior authorization status becomes accessible through the Patient Access API, since members can self-serve updates rather than wait for callbacks. Industry surveys in 2025 showed a slow start on implementation for many payers and providers, which points to a ramp that intensifies through 2027 as APIs stabilize across networks. As these APIs scale, the AI in Patient Care and Management market benefits from lower friction in accessing structured data that supports timely automation of eligibility checks, documentation assembly, and status notifications.

Rising Consumer Adoption of Virtual Care and Preference for 24/7 Self-Service Digital Front Doors

Consumer expectations for always-on engagement are spilling into healthcare, and virtual touchpoints are becoming the default entry for scheduling, messaging, and triage. Hospitals expanded secure messaging and electronic access capabilities through 2024, which laid the groundwork for scalable digital front doors that integrate with AI chatbots and intake tools. Providers deploying after-hours digital scheduling and multi-channel reminders report stronger appointment capture and fewer no-shows as automated outreach meets patients on their preferred channels.Southeast Asian hospitals have also rolled out WhatsApp-based virtual assistants for booking and patient navigation, showing how conversational interfaces can match regional communication habits. On the supply side, virtual urgent care has continued to evolve with platform upgrades that emphasize 24/7 availability and faster resolution, which reinforces consumer habits that favor immediate access. These factors widen the addressable surface for the AI in Patient Care and Management market as providers and payers align their engagement models with real-time digital expectations.

EHR Integration Complexity and Vendor Gating Increase Time-To-Value

The gap between standards availability and operational deployment remains a bottleneck, which slows the pace at which AI applications can go live inside production EHR workflows. Industry surveys in 2025 indicated that a large share of payers and providers had yet to start required API implementations, which underscores the distance between policy goals and technical reality. Even where FHIR R4 support is present, access occurs through governed APIs with scopes, rate limits, and consent metadata that AI vendors must design around, which adds engineering complexity and lengthens testing cycles. Health IT buyers also apply strict marketplace approvals and workflow validation, which can require months of joint testing to ensure safe embedding in clinician tools. Organizations planning comprehensive interoperability rollouts estimate multi-month timelines and significant direct costs, and they reserve budget for ongoing maintenance and vendor management. These factors favor partners with proven integration tooling and governance, which shapes procurement toward vendors that can demonstrate safe EHR write-back and audit trails. The result is a slower and more resource-intensive path to value for new AI entrants, which can delay wider benefits for the AI in Patient Care and Management market.

Other drivers and restraints analyzed in the detailed report include:

- Acute Healthcare Labor Shortages Push Automation of Front Desk and Contact-Center Workflows

- TEFCA-Enabled National Exchange Improves Record Location and Identity Matching for Assistants

- A2P SMS 10DLC Registration and Carrier Filtering Reduce Outreach Deliverability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 57.42% in 2025 and is projected to lead growth at a 22.34% CAGR through 2031, reflecting a shift to unified platforms that bundle intake, triage, engagement, and documentation under a single governance model for the AI in Patient Care and Management market. Health systems are consolidating vendors to streamline security reviews and simplify contracting, which reduces integration risk and lowers the indirect costs tied to managing multiple point tools across similar workflows. Platform providers now package ambient documentation, EHR search, and patient messaging in one stack, which reduces handoffs and speeds time-to-value for clinical teams that need end-to-end automation. Salesforce announced new Agentforce Health agents that integrate medical histories and device data to automate tasks across referral triage and engagement, which illustrates how software vendors are shipping multi-agent capabilities as part of broader suites. Microsoft expanded healthcare tooling that streamlines triage and prior authorization operations, which strengthens the software core that customers can activate without standing up extensive custom builds. Oracle launched an AI Center of Excellence for healthcare to accelerate embedded use cases across its customer base, which aligns with the consolidation trend as EHR-aligned platforms bring AI natively into clinical workflows. These moves reflect the center of gravity in the AI in Patient Care and Management market as buyers prefer fewer, deeper software relationships that connect clinical and operational teams to one data and orchestration layer.

The AI in Patient Care and Management industry still uses services for complex integration, data governance, and model-risk management, yet code-light configuration now covers many common tasks. EHR marketplaces and secure connectors shorten deployment cycles for standard features, which reduces reliance on large implementation projects for front-office and documentation flows. Platform roadmaps emphasize compliance guardrails and explainability for clinical adoption, which supports growth in hospital and payer settings that require auditable changes. Software-led automation also scales across service lines once initial templates are proven, which compounds return on investment across multi-specialty provider groups. As a result, software increases its strategic importance as buyers seek multi-year partners with interoperable suites that reduce workflow fragmentation in the AI in Patient Care and Management market.

Cloud held 45.34% in 2025 and hybrid is projected to grow at a 21.65% CAGR through 2031 as organizations combine on-premise control with elastic cloud inference. This pattern aligns with PHI stewardship goals while preserving access to state-of-the-art models delivered as managed services in cloud environments. Customers use cloud services for language and search while they pre-process prompts on-premise to minimize PHI exposure, which balances privacy with the need for scale. Microsoft's healthcare-specific tooling illustrates how managed services provide secure model access and workflow components without building everything in-house. Oracle's focus on embedded AI patterns shows how EHR vendors are enabling inference wrapped in clinical context, which reduces the lift for hospital IT teams. These approaches support migration paths that move sensitive workloads behind the firewall and burst compute-heavy tasks to the cloud. In this model, the AI in Patient Care and Management market reinforces security posture while retaining the option to use new capabilities as they are released by cloud providers.

Hybrid topologies also help with EHR integration, since local services can handle identity, consent, and write-back using hospital policies, while cloud models process de-identified context. The resulting pattern allows IT to set guardrails, manage traffic spikes, and audit events without constraining teams to on-premise-only deployments. Many buyers adopt hybrid incrementally, starting with ambient scribing and messaging assistants where model calls are stateless and auditable. As organizations prove success in one department, they extend the same infrastructure to additional use cases such as intake and referral management. Over time, hybrid becomes the default for larger health systems that must meet security and performance targets while keeping access to the latest capabilities in the AI in Patient Care and Management market.

Geography Analysis

North America accounted for 48.26% in 2025, while Asia-Pacific is projected to grow at a 23.37% CAGR over 2026-2031 for the AI in Patient Care and Management market. The region benefits from regulatory clarity and infrastructure that supports secure data sharing, including CMS mandates and TEFCA-based exchange at national scale. Adoption gains come from embedded assistants and ambient documentation inside incumbent EHR workflows that reduce cognitive load and documentation time for clinicians. Platform vendors deliver healthcare-specific AI capabilities that hospital IT teams can activate under existing agreements, which reduces procurement friction for new use cases. The AI in Patient Care and Management market share leadership in North America reflects a mix of regulatory pull and vendor ecosystem depth that speeds deployment cycles relative to other regions.

Asia-Pacific is the fastest-growing region as governments and providers scale digital health initiatives and AI-enabled engagement. National priorities around technology and healthcare modernization are helping organizations test and expand AI in triage, intake, and navigation. Southeast Asian health systems have deployed messaging-based assistants aligned with local channel preferences, which supports rapid uptake without extensive portal migrations. In parallel, platform vendors are extending healthcare solutions into the region through cloud marketplaces and partner networks, which shortens lead times for pilots and rollouts. China's push to deepen AI healthcare commercialization in 2026 signals strong policy interest in scaling digital capabilities within care delivery. These trends support multi-year adoption momentum and set a foundation for continued growth in the AI in Patient Care and Management market.

Europe is expanding AI deployments within data protection and clinical safety frameworks that influence architecture and validation. Health systems emphasize explainability, risk controls, and integration with existing clinical governance, which favors models embedded in incumbent platforms. Multinational vendors continue to localize capabilities to meet EU data handling standards and language requirements. Over time, standardization and cross-border exchange efforts will help providers and payers align assistant workflows with national systems. Regions in the Middle East, Africa, and South America are adding pilots and targeted rollouts as infrastructure and policy frameworks mature. These deployments often concentrate on patient engagement and virtual triage to address access constraints, and they extend reach where specialist staffing is limited. As capabilities prove in one service line, neighboring use cases follow, which reinforces steady growth for the AI in Patient Care and Management market.

- Ada Health

- Amwell (Conversa)

- Artera (formerly WELL Health)

- Buoy Health

- Cedar

- Evernorth (Cigna)

- Fabric (incl. GYANT)

- Genesys Cloud

- Hyro.ai

- Infermedica

- Kyruus Health

- Lifelink Systems

- Luma Health

- Mediktor

- Microsoft

- Notable Health

- Oracle

- Orbita

- Phreesia

- Salesforce Health Cloud

- Syllable

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CMS Interoperability and Prior Authorization APIs Accelerate Digital Patient Access and Status Automation

- 4.2.2 Rising Consumer Adoption of Virtual Care and Preference for 24/7 Self-Service Digital Front Doors

- 4.2.3 Acute Healthcare Labor Shortages Push Automation of Front Desk and Contact-Center Workflows

- 4.2.4 Growth in Patient Portal Usage and FHIR APIs Enables Personalized AI Assistants

- 4.2.5 On-Device and Privacy-Preserving AI Enables PHI-Safe Assistants in Apps and Kiosks

- 4.2.6 TEFCA-Enabled National Exchange Improves Record Location and Identity Matching for Assistants

- 4.3 Market Restraints

- 4.3.1 High-Risk AI Compliance and Privacy Obligations (EU AI Act, HIPAA) Raise Implementation Costs

- 4.3.2 Safety, Hallucinations, and Validation Burdens Slow Deployment in Patient-Facing Use Cases

- 4.3.3 EHR Integration Complexity and Vendor Gating Increase Time-To-Value

- 4.3.4 A2P SMS 10DLC Registration and Carrier Filtering Reduce Outreach Deliverability

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Technology

- 5.3.1 Natural Language Processing (NLP)

- 5.3.2 Chatbots / Conversational Agents

- 5.3.3 Computer Vision

- 5.3.4 Predictive Analytics Engines

- 5.4 By Application

- 5.4.1 Enhanced Communication and Omnichannel Messaging

- 5.4.2 Virtual Health Assistants and Chatbots

- 5.4.3 Patient Intake, Forms, and Pre-Registration

- 5.4.4 Triage and Symptom Checking

- 5.4.5 Care-Plan Adherence and Remote Coaching

- 5.4.6 Medication Support and Refill Assistants

- 5.4.7 Others

- 5.5 By End User

- 5.5.1 Healthcare Providers

- 5.5.2 Healthcare Payers

- 5.5.3 Retail-Health and Digital-Front-Door Platforms

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Ada Health

- 6.3.2 Amwell (Conversa)

- 6.3.3 Artera (formerly WELL Health)

- 6.3.4 Buoy Health

- 6.3.5 Cedar

- 6.3.6 Evernorth (Cigna)

- 6.3.7 Fabric (incl. GYANT)

- 6.3.8 Genesys Cloud

- 6.3.9 Hyro.ai

- 6.3.10 Infermedica

- 6.3.11 Kyruus Health

- 6.3.12 Lifelink Systems

- 6.3.13 Luma Health

- 6.3.14 Mediktor

- 6.3.15 Microsoft

- 6.3.16 Notable Health

- 6.3.17 Oracle

- 6.3.18 Orbita

- 6.3.19 Phreesia

- 6.3.20 Salesforce Health Cloud

- 6.3.21 Syllable

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment