PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064499

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2064499

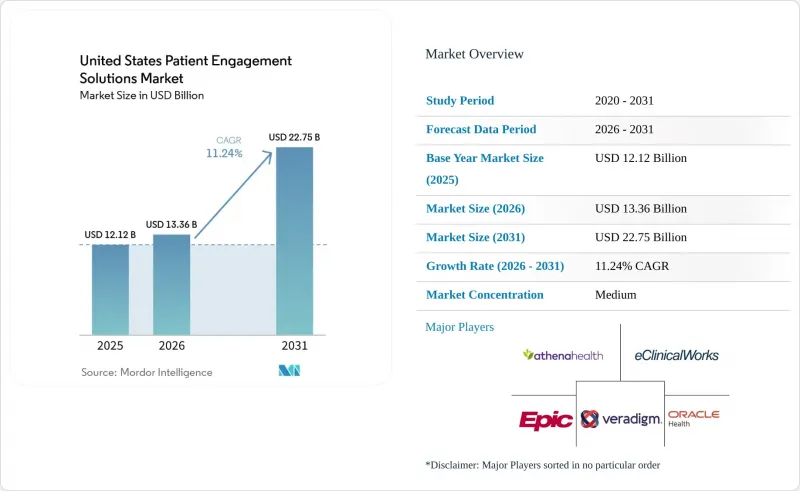

United States Patient Engagement Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states patient engagement solutions market size is projected to be USD 12.12 billion in 2025, USD 13.36 billion in 2026, and reach USD 22.75 billion by 2031, growing at a CAGR of 11.24% from 2026 to 2031.

This report is Segmented by Component (Software, Services, Hardware), Solution Type (AI-Driven, Portals, Telehealth, RPM, Population Health), Delivery Model (Web/Cloud, On-Premise), Functionality, Application, Therapeutic Area (Chronic, Women's, Behavioral & Mental, Others), and End User (Providers, Payers, Pharmacies, Others). The Market Forecasts are Provided in Terms of Value (USD).

United States Patient Engagement Solutions Market Trends and Insights

Shift to Value-Based and Patient-Centric Care

The United States patient engagement solutions market is benefiting from value-based payment structures that reward providers and payers for measurable clinical improvement rather than visit volume alone. The Medicare Alternative Payment Model incentive payment rate fell to 1.88% in 2026 from 5% in earlier program years, which reduced the financial cushion that once made inefficient care coordination easier to absorb. That change is making digital outreach, care plan follow-up, adherence tracking, and patient-reported engagement records more important for contract performance and reporting. CMS's ACCESS model also supports outcome-aligned payments for technology-enabled care when providers achieve measurable targets such as blood pressure reduction or pain management. The United States patient engagement solutions market is also drawing stronger payer investment, as digital engagement now supports member navigation, care gap closure, and retention. UnitedHealthcare launched Avery in March 2026 as a generative AI companion inside its member app, showing that large payers now treat engagement capability as part of core benefit delivery.

High Chronic Disease and Aging Burden

The United States patient engagement solutions market has a durable demand base because chronic and mental health conditions continue to shape how care is financed, delivered, and monitored. CDC states that 90% of the nation's USD 4.9 trillion in annual healthcare spending is attributable to people with chronic and mental health conditions, which keeps pressure on health systems to improve between-visit management. Patients managing multiple long-duration conditions typically require more reminders, more education, more follow-up, and more documentation than episodic care populations. That pattern increases the strategic value of platforms that can keep outreach continuous across medication use, symptom monitoring, and care plan updates. The United States patient engagement solutions market, therefore, benefits not just from disease prevalence, but from the recurring interaction frequency that chronic care creates inside provider and payer workflows.

Interoperability Gaps Across EHR, Payer, and Point-Solution Stacks

The United States patient engagement solutions market still faces a structural limit because patient data often sits across disconnected provider, payer, and specialized workflow systems. A 2025 systematic review in Frontiers in Health Services found persistent barriers, including semantic misalignment across HL7 FHIR and SNOMED CT implementations, limited cross-system exchange, and weak integration of patient-generated health data. That means standards adoption alone does not guarantee a usable longitudinal record inside patient engagement platforms. HHS leadership wrote in a 2025 JAMA article that unlocking the potential of EHR data for patient experience improvement still requires a more unified approach to exchange and implementation. When information appears incomplete or inconsistent across portals, reminders, and payer touchpoints, patients are less likely to trust the digital channel. The United States patient engagement solutions market, therefore, remains constrained by operational integration quality, not just by the number of interfaces a vendor can claim to support.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Digital Front-Door and AI Engagement Adoption

- CMS Interoperability and Prior Authorization API Rollout

- Data Privacy, Cybersecurity, and HIPAA Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 58.66% of the United States patient engagement solutions market in 2025, which kept it well ahead of services and hardware in the spending mix. That lead reflects the scale of platform demand for communication, scheduling, intake, reminders, education, and care coordination inside one digital layer. Integrated suites remain the preferred choice for large health systems because they reduce vendor sprawl and fit more easily inside established clinical workflows. Standalone applications still hold an important role in narrower use cases such as intake optimization, patient financing, and behavioral outreach, where buyers often want deeper configuration. The United States patient engagement solutions market continues to reward software vendors that can combine workflow breadth with faster implementation and easier clinician adoption.

Services are projected to record the fastest component growth at a 12.39% CAGR through 2031, which shows that deployment complexity is rising with platform sophistication. Health systems increasingly need implementation support, integration work, staff training, ongoing optimization, and compliance guidance as AI agents and FHIR-based connectivity become more common. Phreesia stated in its FY2026 stakeholder letter that it enabled more than 180 million patient visits in 2025 and expanded its scope through the AccessOne acquisition, which added patient financing capability to its platform offering. Hardware remains a supporting layer rather than the core spending center, but kiosks, bedside devices, tablets, and identity tools still matter in ambulatory and inpatient settings. Oracle Health's CLEAR integration shows how identity verification is being folded into digital intake and paper-free check-in workflows, which keeps certain hardware-linked functions relevant even as software takes the largest share.

AI-driven engagement held 30.51% of the solution type segment in 2025, making it the largest category inside the United States patient engagement solutions market. Its lead comes from intelligent outreach, conversational scheduling, triage support, and care gap closure tools that are now moving into routine enterprise use. Platforms with larger installed bases also build richer behavioral datasets over time, which improves personalization and makes the product more useful with each new interaction. That advantage matters because patient response patterns, channel preferences, and timing behavior can shape outreach quality in ways that are difficult for newer entrants to replicate quickly. The United States patient engagement solutions market is, therefore, seeing solution competition move from isolated features toward data-backed workflow performance.

Remote patient monitoring is forecast to expand at an 11.95% CAGR through 2031, which makes it the fastest-growing solution type over the forecast period. Its growth is tied to chronic disease prevalence, wider use of between-visit monitoring, and reimbursement support for remote physiologic monitoring activities in higher-risk populations. Patient portals still account for a meaningful share of solution demand, but ONC data shows that adoption and capability use remain uneven among lower-resourced hospitals. Telehealth solutions also remain embedded in the engagement stack because virtual care now supports access, follow-up, and convenience expectations across many care settings. Population health tools, medication reminders, intake platforms, and financial engagement systems continue to sell alongside one another, which is encouraging multi-solution purchasing inside broader platform ecosystems.

Web-based and cloud-based delivery held 67.35% share in 2025 and is also the fastest-growing model at a 13.33% CAGR through 2031. That combination shows that the dominant delivery model in the United States patient engagement solutions market is still gaining ground rather than moving into a slow-growth phase. Health systems favor cloud deployment because it supports faster upgrades, more flexible scaling, and easier rollout of AI-enabled features across multiple sites. The Change Healthcare attack pushed many organizations to review infrastructure resilience, vendor dependencies, and recovery preparedness with greater urgency after 2024. Frequent release cycles also suit cloud environments better, since modern engagement platforms need regular workflow tuning, security updates, and model changes.

On-premise delivery still retains a role in federal settings, highly regulated specialty environments, and organizations with stricter network isolation requirements. Some providers continue to prefer local control over deployment and data flows when internal governance is more conservative or when legacy infrastructure remains deeply embedded. Procurement standards such as HITRUST and FedRAMP have also raised the bar for cloud vendors serving sensitive or publicly funded programs, which can slow smaller entrants. Oracle Health's QHIN and CMS Aligned Network activity shows that interoperability expectations and delivery architecture are increasingly being planned together rather than separately. The United States patient engagement solutions market is therefore moving toward cloud-first deployment as the default, even though on-premise options still matter in selected enterprise environments.

List of Companies Covered in this Report:

- athenahealth

- eClinicalWorks

- Epic Systems

- Experian Health

- Get Well

- Luma Health

- Mckesson

- Meditech

- NextGen Healthcare

- Oracle

- Phreesia, Inc.

- Press Ganey

- Salesforce

- Solutionreach, Inc.

- TeleVox

- TruBridge, Inc.

- Veradigm

- WellSky

- Xealth

- Yosi Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift To Value-Based and Patient-Centric Care

- 4.2.2 High Chronic Disease and Aging Burden

- 4.2.3 Rapid Digital Front-Door and AI Engagement Adoption

- 4.2.4 Consumer Demand for Self-Service Access and Communication

- 4.2.5 CMS Interoperability and Prior Authorization API Rollout

- 4.2.6 CMS Healthtech Ecosystem and Medicare App Library Discovery Layer

- 4.3 Market Restraints

- 4.3.1 Interoperability Gaps Across EHR, Payer, And Point-Solution Stacks

- 4.3.2 Data Privacy, Cybersecurity, and HIPAA Compliance Burden

- 4.3.3 Portal And App Fragmentation Reducing Longitudinal Engagement

- 4.3.4 AI Governance and ROI Scrutiny Slowing Enterprise Rollouts

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Integrated patient engagement platforms

- 5.1.1.2 Standalone patient engagement applications

- 5.1.2 Services

- 5.1.2.1 Implementation and integration services

- 5.1.2.2 Training and education services

- 5.1.2.3 Support and maintenance services

- 5.1.2.4 Consulting and optimization services

- 5.1.3 Hardware

- 5.1.3.1 Bedside engagement devices

- 5.1.3.2 Self-service kiosk and check-in devices

- 5.1.3.3 Patient tablets and remote devices

- 5.1.1 Software

- 5.2 By Solution Type

- 5.2.1 AI-driven engagement

- 5.2.2 Patient portals

- 5.2.3 Telehealth solutions

- 5.2.4 Remote patient monitoring solutions

- 5.2.5 Population health and outreach solutions

- 5.2.6 Appointment and medication reminder solutions

- 5.2.7 Patient intake and registration solutions

- 5.2.8 Financial engagement solutions

- 5.3 By Delivery Model

- 5.3.1 Web-based and cloud-based

- 5.3.2 On-premise

- 5.4 By Functionality

- 5.4.1 Communication and messaging

- 5.4.2 Scheduling and access

- 5.4.3 Clinical enablement

- 5.4.4 Financial and administrative workflow

- 5.4.5 Analytics and personalization

- 5.5 By Application

- 5.5.1 Health management

- 5.5.2 Home and remote care management

- 5.5.3 Care coordination and communication

- 5.5.4 Social and behavioral management

- 5.5.5 Financial health management

- 5.6 By Therapeutic Area

- 5.6.1 Chronic diseases

- 5.6.1.1 Diabetes

- 5.6.1.2 Cardiovascular diseases

- 5.6.1.3 Respiratory diseases

- 5.6.1.4 Oncology

- 5.6.1.5 Obesity and metabolic disorders

- 5.6.1.6 Other chronic diseases

- 5.6.2 Women's health

- 5.6.3 Behavioral and mental health

- 5.6.4 Other therapeutic areas

- 5.6.1 Chronic diseases

- 5.7 By End User

- 5.7.1 Providers

- 5.7.2 Payers

- 5.7.3 Pharmacies

- 5.7.4 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 athenahealth

- 6.3.2 eClinicalWorks

- 6.3.3 Epic Systems Corporation

- 6.3.4 Experian Health

- 6.3.5 Get Well

- 6.3.6 Luma Health

- 6.3.7 McKesson Corporation

- 6.3.8 MEDITECH

- 6.3.9 NextGen Healthcare, Inc.

- 6.3.10 Oracle

- 6.3.11 Phreesia, Inc.

- 6.3.12 Press Ganey

- 6.3.13 Salesforce

- 6.3.14 Solutionreach, Inc.

- 6.3.15 TeleVox

- 6.3.16 TruBridge, Inc.

- 6.3.17 Veradigm LLC

- 6.3.18 WellSky

- 6.3.19 Xealth

- 6.3.20 Yosi Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment