PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063570

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063570

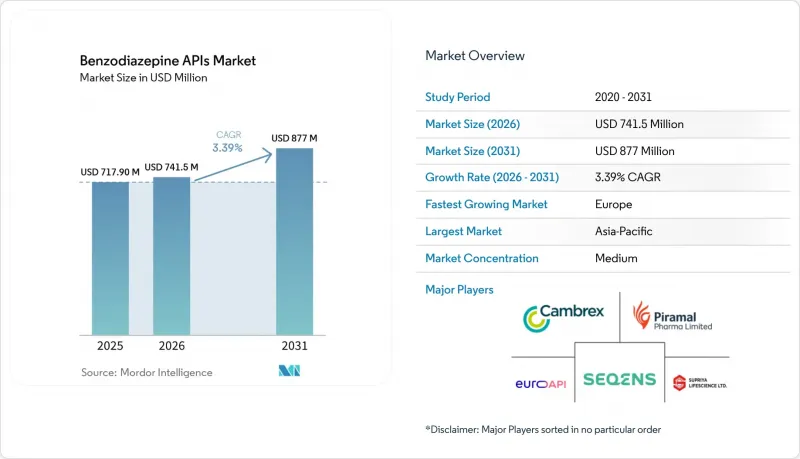

Benzodiazepine APIs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the benzodiazepine aPIs market size is expected to increase from USD 717.90 million in 2025 to USD 741.5 million in 2026 and reach USD 877 million by 2031, growing at a CAGR of 3.39% over 2026-2031.

This report is Segmented by Molecule (Alprazolam, Diazepam, Lorazepam, Midazolam, Clonazepam, Clobazam, and More), Therapeutic Indication (Anxiety, and More), End User (Generic Manufacturers, Innovators, Hospitals, Cdmos, Veterinary), Route of Administration (Oral, Parenteral, Nasal, Others), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Benzodiazepine APIs Market Trends and Insights

Anxiety and Seizure Burden Sustaining Core Molecules

Anxiety disorders generated major revenue in 2025 demand and remain pivotal as the WHO's 2025 policy note urged every member state to ring-fence continuous alprazolam and diazepam supplies on essential-medicine lists. INCB import statistics show 8,766 kg of alprazolam and 33,092 kg of diazepam distributed to 141 countries in 2024, underscoring entrenched clinical reliance. Pediatric seizure rescue is widening the base further; buccal midazolam and rectal diazepam were added to formularies from Zambia to Seychelles last year. ASAM's 2025 tapering guideline simultaneously preserved the role of short-acting benzodiazepines for acute crises while discouraging months-long regimens. The dual narrative of access and caution is therefore channeling more active pharmaceutical ingredients (APIs) into hospital emergency kits, public stockpiles, and veterinary neurology while tempering large-volume chronic tablet prescriptions.

ICU and Procedural Sedation Needs Supporting Injectable APIs

Midazolam's projected significant growth stems from its indispensability where seconds matter, bronchoscopy, cardioversion, dental surgery, and alcohol-withdrawal delirium. SCCM's 2025 critical-care guideline shifted ventilated patients toward propofol or dexmedetomidine, yet kept IV midazolam in first position for refractory agitation. FDA clearance of ready-to-use intranasal midazolam devices for seizure clusters has spilled over into procedural suites, especially pediatrics, where needle-free access improves throughput and patient comfort. Piramal's USD 90 million sterile fill-finish upgrade in Michigan and Kentucky directly targets this hospital pipeline, affirming that parenteral benzodiazepines will not exit formularies despite broader sedative substitution.

Tighter Safety Warnings and Prescribing Controls Curbing Chronic Use

The 2024 FDA boxed warning on benzodiazepine-opioid co-prescription and ASAM's 2025 tapering algorithm are compressing refill volumes for alprazolam tablets, previously the workhorse of primary-care anxiety therapy. Europe followed with prior-authorization hurdles in Spain and France, pushing patients toward SSRIs or SNRIs for generalized anxiety. PDMP systems in 47 U.S. states now flag prescriptions longer than 30 days, disincentivizing family physicians from large scripts. Net impact is a measurable decline in chronic outpatient usage, partially compensated by growth in high-acuity settings.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Generic Manufacturing and API Outsourcing

- Veterinary Neurology/Sedation Use Cases Maintaining Niche Volumes

- International Trade and Permit Frictions for Psychotropics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alprazolam generated the largest 32.18% benzodiazepine active pharmaceutical ingredients (APIs) market share in 2025, yet its growth is flattening under prescribing caps. Continuous-flow chemistry from Purdue has slashed diazepam cost-of-goods by 25%, but commercial adoption remains at pilot scale. Midazolam, aided by intranasal launches, is forecast for a 3.87% pace, the fastest in the set. Diazepam and lorazepam together made up a notable portion of volume, but grapple with intermittent shortages that push hospitals toward midazolam substitutes. Specialty epilepsy molecules such as clobazam are edging upward in orphan-drug niches, whereas older insomnia actives like flurazepam languish amid non-benzodiazepine hypnotic competition.

Commercial economics differ sharply: high-volume tablets carry razor-thin margins, whereas rescue sprays or sterile syringes command premiums for micronized or sterile-filtered intermediates. That bifurcation is visible in investment patterns, Cambrex added controlled-substance flow reactors in Iowa for specialty lots while Indian exporters chase tablet-grade demand. Continuous-flow patents filed during 2024-2026 for lorazepam and clonazepam underscore a race to greener, lower-solvent routes that can satisfy EU sustainability audits once the Critical Medicines Act's environmental reporting clauses activate in 2027.

At 43.12% of 2025 usage, anxiety remains the principal indication, buoyed by WHO-endorsed essential-medicine programs even as chronic scripts contract. Epilepsy and cluster seizure rescue represent the next-largest slice, swelling since the FDA widened Valtoco's label to children aged 2-5 in April 2025. ICU sedation volumes are plateauing because of guideline shifts, yet midazolam holds irreplaceable status for alcohol-withdrawal delirium, keeping a floor under injectable purchases. Procedural sedation, colonoscopy, dental, and minor orthopedic procedures have emerged as the fastest-advancing clinical bucket at 4% plus, thanks to intranasal adoption that circumvents IV lines in day-surgery centers. Muscle spasm, insomnia, and veterinary neurology round out demand at single-digit percentages but carry distinct formulation needs, rectal gels, buccal solutions, flavor-masked liquids, that bolster API premiums.

Geography Analysis

Asia-Pacific remained the engine at 47.15% of worldwide revenue in 2025, rooted in India's manufacturing heft and China's precursor stranglehold. Still, Europe's 3.68% CAGR is set to outpace every region as reshoring aid and six-month buffer stocks stimulate localized output. The Benzodiazepine APIs market share for Europe is expected to grow significantly under the Critical Medicines Act's direct procurement clauses.

North America held a notable share in 2025 revenue, sustained by hospital procedural sedation and federally funded emergency reserves. Persistent diazepam and lorazepam shortages in 2024-2026 nudged hospitals to midazolam, triggering Siegfried's multi-site U.S. acquisition spree in May 2026. Canada and Mexico trail in volume but face heightened border checks under DEA diversion crackdowns.

The Middle East & Africa cluster shows patchy yet vital growth tied to tertiary-care upgrades in Gulf states and expanded essential-medicine lists in Southern Africa. South America's dependence on Indian imports exposes it to permit oscillations; Argentina endured three months of stock-outs in 2025 after incomplete INCB filings. WHO's 2025 balance guideline is nudging ministries to execute firmer demand forecasts, smoothing but not eliminating periodic shortages.

- ALP Pharmaceutical Ltd.

- Apotex

- Cambrex

- Centaur Pharmaceuticals Private Limited

- Cohance Lifesciences Limited

- EUROAPI S.A.S.

- Fermion Oy

- FIS - Fabbrica Italiana Sintetici

- Global Calcium Private Limited

- Honour Lab Limited

- JSC Farmak

- Lake Chemicals Pvt. Ltd.

- Malladi Drugs & Pharmaceuticals Ltd.

- Medichem S.A.

- Minakem SAS

- Piramal Pharma Limited

- Qilu Anxin Pharmaceutical Co., Ltd.

- RL Fine Chem Pvt. Ltd.

- SEQENS Group

- Solara Active Pharma Sciences

- Sun Pharmaceuticals Industries

- Supriya Lifescience Ltd.

- Wavelength Pharmaceuticals Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Anxiety And Seizure Burden Sustaining Core Molecules

- 4.2.2 ICU and Procedural Sedation Needs Supporting Injectable APIs

- 4.2.3 Expansion of Generic Manufacturing and API Outsourcing

- 4.2.4 Veterinary Neurology/Sedation Use Cases Maintaining Niche Volumes

- 4.2.5 Essential-Medicine Stockpiling and Reshoring Programs Stabilizing Demand

- 4.2.6 Intranasal and Rescue-Therapy Reformulations Lifting Select APIs

- 4.3 Market Restraints

- 4.3.1 Tighter Safety Warnings and Prescribing Controls Curbing Chronic Use

- 4.3.2 International Trade/Permit Frictions for Psychotropics

- 4.3.3 Diversion/Abuse Risk Prompting Regional Restrictions

- 4.3.4 Supply-Chain Fragility and Precursor Constraints

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Molecule

- 5.1.1 Alprazolam

- 5.1.2 Diazepam

- 5.1.3 Lorazepam

- 5.1.4 Midazolam

- 5.1.5 Others

- 5.2 By Therapeutic Indication Served

- 5.2.1 Anxiety disorders

- 5.2.2 Epilepsy and seizure rescue (incl. cluster seizures)

- 5.2.3 ICU sedation and agitation management

- 5.2.4 Procedural sedation/anesthesia

- 5.2.5 Insomnia

- 5.2.6 Muscle spasm and spasticity

- 5.2.7 Preoperative anxiolysis

- 5.2.8 Other Therapeutic Indications

- 5.3 By End User (API Buyers)

- 5.3.1 Generic finished-dose manufacturers

- 5.3.2 Innovator/branded manufacturers

- 5.3.3 Hospital outsourcing and compounding centers

- 5.3.4 CDMOs with captive FDF lines

- 5.3.5 Veterinary pharmaceuticals manufacturers

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Parenteral

- 5.4.3 Nasal

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 ALP Pharmaceutical Ltd.

- 6.3.2 Apotex Inc.

- 6.3.3 Cambrex Corporation

- 6.3.4 Centaur Pharmaceuticals Private Limited

- 6.3.5 Cohance Lifesciences Limited

- 6.3.6 EUROAPI S.A.S.

- 6.3.7 Fermion Oy

- 6.3.8 FIS - Fabbrica Italiana Sintetici S.p.A.

- 6.3.9 Global Calcium Private Limited

- 6.3.10 Honour Lab Limited

- 6.3.11 JSC Farmak

- 6.3.12 Lake Chemicals Pvt. Ltd.

- 6.3.13 Malladi Drugs & Pharmaceuticals Ltd.

- 6.3.14 Medichem S.A.

- 6.3.15 Minakem SAS

- 6.3.16 Piramal Pharma Limited

- 6.3.17 Qilu Anxin Pharmaceutical Co., Ltd.

- 6.3.18 RL Fine Chem Pvt. Ltd.

- 6.3.19 SEQENS Group

- 6.3.20 Solara Active Pharma Sciences Limited

- 6.3.21 Sun Pharmaceutical Industries Ltd.

- 6.3.22 Supriya Lifescience Ltd.

- 6.3.23 Wavelength Pharmaceuticals Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment